Download

1 / 70

700 likes | 865 Views

ECO 3311 Ch 11: Monetary Policy. Introduction. In this chapter, we learn: how the central bank effectively sets the real interest rate in the short run, and how this rate shows up as the MP curve in our short-run model.

E N D

ECO 3311 Ch 11: Monetary Policy

Introduction • In this chapter, we learn: • how the central bank effectively sets the real interest rate in the short run, and how this rate shows up as the MP curve in our short-run model. • that the Phillips curve describes how firms set their prices over time, pinning down the inflation rate. • how the IS curve, the MP curve, and the Phillips curve make up our short-run model. • how to analyze the evolution of the macroeconomy—output, inflation, and interest rates—in response to changes in policy or economic shocks.

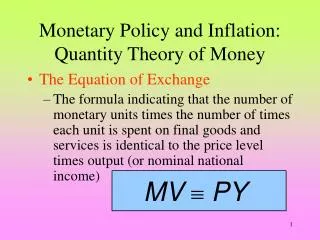

The federal funds rate is the interest rate paid from one bank to another for overnight loans. • The monetary policy (MP) curve describes how the central bank sets the nominal interest rate and exploits the fact that the real and the nominal interest rates move closely together in the short run.

The short-run model is summarized as follows: • Through the MP curve, the nominal interest rate set by the central bank determines the real interest rate in the economy. • Through the IS curve, the real interest rate influences GDP in the short-run. • The Phillips curve describes how booms and recessions affect the evolution of inflation.

The MP Curve: Monetary Policy and the Interest Rates • Large banks and financial institutions borrow from each other from one business day to the next. • To set the nominal interest rate on overnight loans, the central bank states that it is willing to borrow or lend any amount at the specified rate.

Banks cannot charge a higher rate because everyone would use the central bank. • Banks cannot charge a lower rate because banks would borrow at the lower rate and lend it back to the central bank at a higher rate. • This opportunity for pure profit is called the arbitrage opportunity. • Thus, banks must exactly match the rate the central bank is willing to lend at.

From Nominal to Real Interest Rates • The relationship between the nominal interest rate and the real interest rate is given by the Fisher equation. • Changes in the nominal interest rate lead to changes in the real interest rate so long as they are not offset by corresponding changes to inflation.

The sticky inflation assumption implies that the rate of inflation displays inertia, or stickiness, so that it adjusts slowly over time. • In the very short run (6 months or so), we assume the rate of inflation does not respond directly to monetary policy. • It implies central banks have the ability to set the real interest rate in the short run.

The IS-MP Diagram • The MP curve illustrates the central bank’s ability to set the real interest rate. • Central banks set the real interest rate at a particular value and the MP curve is a horizontal line.

The IS-MP diagram is a graph of the IS and the MP curves. • The economy is at potential when the real interest rate equals the MPK and when there are no aggregate demand shocks. • short-run output = 0 • If the central bank raises the interest rate above the MPK, inflation is slow to adjust so the real interest rate rises and investment falls.

Example: The End of a Housing Bubble • Suppose housing prices had been rising, but they fall sharply. • This episode implies that the aggregate demand parameter declines and the IS curve shifts left.

If the central bank lowers the nominal interest rate in response, the real interest rate falls as well because inflation is sticky. • If judged correctly and without lag, the economy would not have a decline in output.

In reality, policymakers are unsure of the severity of shocks and it takes 6 to 18 months for changes in the interest rate to impact the economy.

The Phillips Curve • Recall that the inflation rate is the percentage change in the overall price level for the coming year. • Firms set their prices on the basis of their expectations of the economy-wide inflation rate and the state of demand for their product.

Expected inflation is the inflation rate firms think will prevail in the rest of the economy over the coming year.

Assume that firms expect the inflation rate in the coming year to equal the rate of inflation that prevailed during the last year. • Under adaptive expectations firms adjust their forecasts of inflation slowly. • Expected inflation embodies the sticky inflation assumption.

The Phillips curve describes how inflation evolves over time as a function of short-run output. • If output is below potential prices rise more slowly than usual. • If output is above potential prices rise more rapidly than usual.

Let denote the change in the rate of inflation: • Therefore, the Phillips Curve can be expressed as: • The parameter measures how sensitive inflation is to demand conditions. • If it is low, it takes a larger recession to reduce the rate of inflation by a percentage point.

Price Shocks and the Phillips Curve • We can add shocks to the Phillips curve to account for temporary increases in the price of inflation:

The actual rate of inflation now depends on three things: • The expected rate of inflation, which equals the inflation rate from last year by adaptive expectations: • An adjustment factor for the state of the economy: • A shock to inflation:

An oil price shock, which when the price of oil rises, will result in a temporary upward shift in the Phillips curve.

Cost-Push and Demand-Pull Inflation • Price shocks to an input in production are cost-push inflation because higher input prices (akin to negative supply shocks) tend to push the inflation rate up. • The effect of short-run output on inflation in the Phillips curve is demand-pull inflation because increases in aggregate demand pull up the inflation rate.

Using the Short-Run Model • Disinflation is sustained reduction of inflation to a stable lower rate. • The Great Inflation of the 1970s was when misinterpreting the productivity slowdown contributed to rising inflation.

The Volcker Disinflation • Reducing the level of inflation requires a sharp reduction in the rate of money growth – a tight monetary policy.

Because of the stickiness of inflation, the classical dichotomy is unlikely to hold exactly in the short run and just a reduction in the rate of money growth may not slow inflation immediately. • Thus, the real interest rate must increase to induce a recession. • The recession causes a reduction in inflation because as demand falls firms raise their prices less aggressively to sell more.

Lowering the inflation rate comes with a cost of a slumping economy, which implies high unemployment and lost output. • Once inflation has declined sufficiently, the real interest rate can be raised back to the MPK allowing output to rise back to potential.

Panel (a): The Volcker policy starts at date 0 and continues until time t*. • Panel (b): Output stays below potential. • Panel (c): Through the Phillips curve, this leads the rate of inflation to decline gradually over time.

The Great Inflation of the 1970s • Inflation rose in the 1970s for three reasons: • OPEC coordinated oil price increases.

The U.S. monetary policy was too loose because the conventional wisdom was that reducing inflation could only be accomplished with permanent increases in employment. • Actually, disinflation requires only a temporary recession.

The Federal Reserve did not have perfect information on the economy and thought the productivity slowdown was a recession, when it was actually a change in potential output. • The Fed lowered interest rates in response to what they perceived was a demand shock, which increased output above potential and generated more inflation.

The Short-Run Model in a Nutshell • The MP curve implies that increases in the nominal interest rate increase the real interest rate:

The IS curve implies that increases in the real interest rate decrease short-run output:

The Phillips curve implies that decreases in short-run output decrease the change in inflation:

Case Study: The 2001 Recession • The recession of 2001 had a “jobless recovery” because even after the return of strong GDP, employment continued to fall. • This is an exception to Okun’s law, which assumes employment and GDP move together.

Microfoundations: Understanding Sticky Inflation • The short run model says that changes in the nominal interest rate affect the real interest rate because inflation does not adjust immediately. • Recall the classical dichotomy says that changes in nominal variables have only nominal effects on the economy and the real side is determined solely by real forces. • If monetary policy affects real variables, the classical dichotomy fails in the short run.

The Classical Dichotomy in the Short-Run • For the classical dichotomy to hold at all points in time, all prices in the economy, including wages and rental prices must adjust in the same proportion immediately.

Reasons why the classical dichotomy fails in the short run are that: • Imperfect information and the costly computation of prices imply that there are costs of setting prices – thus firms do not update prices immediately. • Contracts also set prices and wages in nominal rather than real terms – and these contracts prevent wages from adjusting immediately.