Download

1 / 22

• 220 likes • 388 Views

Financial Underwriting ABC Co. Case Study. Isabelle Dailly, FALU Regional Underwriting Consultant. Important Information.

E N D

Financial UnderwritingABC Co. Case Study Isabelle Dailly, FALU Regional Underwriting Consultant

Important Information We've provided written material with this oral presentation to make it easier for you to take notes. Do not rely on the written material on its own because it may be incomplete or inaccurate without the additional context and information provided by the oral presentation. Because of this, and also because the presentation is of a technical nature designed for insurance professionals, the written material should not be redistributed. We have provided client-friendly material about many of our products and concepts on our advisor website at www.manulife.com/repsource. This presentation is for educational purposes only. It should not be construed as legal, tax or accounting advice. This presentation doesn't bind Manulife to provide, or to continue to provide, any of the concepts or products described in the presentation. It also doesn't limit Manulife's ability to change any of the procedures that may be described in the presentation. If this presentation contains competitive information, we've made every effort to ensure its accuracy as of the date of the original oral presentation. We can't, however, guarantee the accuracy and, if you have any questions regarding this information, you should contact the competitor directly.

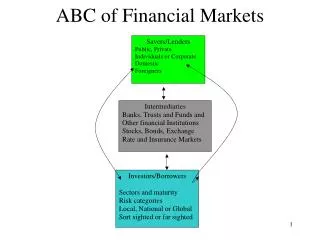

Financial Underwriting Guidelines • Page 1 – personal needs driven • Page 2 - business insurance • Page 3 – insurance for tax planning purposes (insurance as an investment)

Why do we underwrite financially? • Large case mortality studies • Relationship between amount and need for insurance • Avoid bad claims • Follow published guidelines

Case Presentation • Male 61 non-smoker • Medically standard • Cover letter included • T10 $4,000,000 • Corporate owner/beneficiary

Open Envelop #1 • Read the cover letter • Read the inspection report • Read the financial statements • Consider your financial underwriting guidelines • Discuss are you going to approve this application for $4 million

What did you come up with? • Approve? • Decline? • Ask for more information?

My notes • Insurance in force: $2 Million Bus. Insurance with Canada Life, to be replaced • $163,000 Norwich Union - personal • Annual Income $200,000 • Personal net worth > $2 million • New coverage $4 Million T10 • Owner: ABC Inc. • Beneficiary: 85% ABC Inc. (3,400,000), 15% spouse ($600,000) • Purpose of insurance: Loan Protection and Growth of company. In 2005 insured increased his ownership to 85% by repurchasing shares from Venture Capital company • Insured is 85% (application) or 80% (IR ) owner

My notes (2) • Purpose of insurance: Loan Protection and Growth of company. In 2005 insured increased his ownership to 85% by repurchasing shares from Venture Capital company • Insured is 85% (application) or 80% (IR) . Mr. Smart, please confirm whether this means buy-sell coverage, is there a buy-sell agreement in place, the other partners have coverage you state, is this for buy-sell coverage, or is this keyman coverage? Is his percentage 80 or 85%? • Other partners have insurance in force (no details on amounts) Mr. Smart, what amounts are inforce on partners?

My notes (3) • Additional information: building for the business (blind manufacturer, 220 employees) is being purchased by insured on personal basis. • Discussed with Dereka Thibault, TEPG, it is not unusual for a business to separate out real estate holdings from operating company. Having personal ownership of the building and leasing it back to business can make good business sense, particularly if life insurance is not required by financial institution and no deductibility issues. Most real estate would not require mortgage coverage as the property backs the loan.

My notes (4) • Mr. Smart, the inspection report states the company is buying the building, but you told us he is buying the building. If he is buying it personally and leasing back to company, is some of the insurance coverage to cover this mortgage? will the policy be collaterally assigned to the bank to cover the outstanding mortgage in case of death, or is there a shareholders agreement or board resolution that directs the outstanding amount of the mortgage to be paid off. What is the purchase price of building and what is the loan amount (if this is what we are underwriting for)? • Jan 31, 2005 Financial Statements ABC Inc. (started in 1978) • 2005 gross sales $18 million, 2004 gross sales $16 million • 2005 niat $916,689, 2004 niat $908,617 • bank indebtedness at Jan 31, 2005 $1.9 million Mr. Smart, do we have a feel for the current bank indebtedness? one year later

My notes (5) • Rough business valuation using our BVP method about $9 million, accountant estimates business values to be between $4 and $8 million (no formal valuation done) • We would consider coverage for buysell at 80 or 85% of FMV conservatively estimated at $4 million. Mr. Smart, if this is what is required here, we just need to confirm the other 2 partners are insured equally (i.e. for their percentage of ownership) - although really considering the amounts it is quite possible that this client is the only one that really requires the insurance i.e. he could buy-out the other partners' minor interest fairly easily without coverage. • If that is not the case, and it is keyman please advise.

We now have the full FS with notes • Review notes to financial statement • Where are you now? • Decision?

My underwriting notes • income / net worth? • Purpose of insurance? • Other partners? • 80/85? • Collateral assignment? • Business valuation? • The agent’s reply …..

The solution … • Hi David, • I spoke with the insured, Wayne this afternoon (604 123 4567) as requested by the agent, Mr. Smart. • Client advises that his partners have $500,000 and $1,000,000 of coverage in force. • There is a shareholder agreement in place. • The insurance coverage is required for buy-sell coverage. • He increased his percentage ownership to 80% of the company in 2005 and therefore needs the increased coverage. • Yes, he is purchasing a building, but the insurance is not for that,it is to fund the buy-sell agreement. • Based on the most conservative value of $4 million X 80% = $3,200,000 • The coverage requested in $3,600,000 and I would recommend approving the coverage as requested. • Isabelle Dailly, FALU

Always Communicate: • Existing coverage and any planned replacement • Purpose of the proposed coverage • How the amount of coverage was determined and sales concept used • Rationale behind owner and beneficiary designations, if not evident • Include supporting documentation such as financial/net worth statements

Always keep in mind: • The underwriter has not been a part of the sales process, has not met the client and is only aware of the details presented on the application and attachments • The underwriter must establish the purpose of the insurance and justify the amount, based solely on the application and supporting information you have provided

Understand • Financial requirements: financial statements, personal net worth statements, financial questionnaires, copies of investment statements, T1s, Inspection Reports, Third Party Verification

BE ABLE TO EXPLAIN … • Do not tell your client/his accountant ‘I don’t know why the insurance company wants this’ ‘I’ll see if they will waive these requirements’ • Explain rationally the need for financial underwriting and third party verification • Clients can and will understand financial underwriting • Provide privacy guidelines

Alwayskeep in mind: • If the underwriter is concerned about the financial justification on a case or suspects potential fraud or anti-selection, an unscheduled inspection report or other discretionary requirements may be requested, complicating and perhaps jeopardizing the sale • It is always advisable to be “proactive” and provide the financial documentation the underwriter requiresto approve the risk – overkill!!!

Questions? Email: isabelle_dailly@manulife.com