Download

1 / 45

450 likes | 770 Views

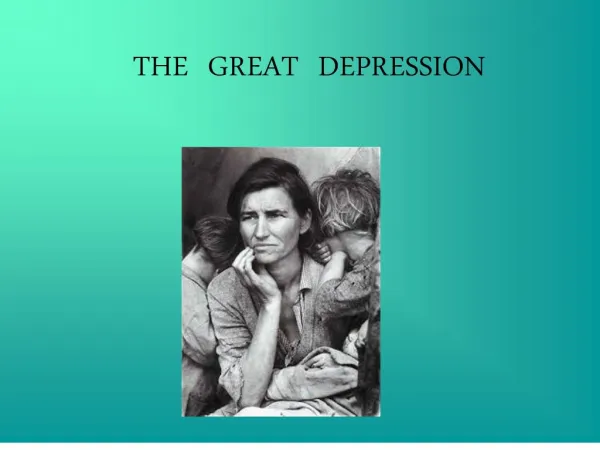

The Great Depression. The Great Depression. The worst economic contraction was the Great Depression of the 1930s. Real GDP fell nearly 30% from the peak in August 1929 to the trough in March 1933. The unemployment rate rose from 3% to nearly 25%.

E N D

The Great Depression • The worst economic contraction was the Great Depression of the 1930s. • Real GDP fell nearly 30% from the peak in August 1929 to the trough in March 1933. • The unemployment rate rose from 3% to nearly 25%. • Thousands of banks failed, the stock market collapsed, many farmers went bankrupt, and international trade was halted. • There were really two business cycles in the Great Depression. • A contraction from August 1929 to March 1933, followed by an expansion that peaked in May 1937. • A contraction from May 1937 to June 1938. • By May 1937, output had nearly returned to its 1929 peak, but the unemployment rate was high (14%). • In 1939 the unemployment rate was over 17%.

American Business Cycle • Recessions were common from 1865 to 1917, with 338 months of contraction and 382 months of expansion. • Compare it with 56 months of expansion and only 122 months of contraction from 1945 to 2001. • The longest contraction on record was 65 months, from October 1873 to March 1879. • The longest expansion was 120 months between March 1991 and March 2001. http://www.nber.org/cycles/

Source: http://econ161.berkeley.edu/TCEH/Slouch_Crash14.html

The United States Business Cycle, 1890-1940 Source: http://econ161.berkeley.edu/TCEH/Slouch_Crash14.html

The United States Business Cycle, 1950-1990 Source: http://econ161.berkeley.edu/TCEH/Slouch_Crash14.html

http://oregonstate.edu/Dept/pol_sci/fac/sahr/pc1915ff.htm 10

What Happened During the Great Depression? Huge increase in unemployment rate, of course, means a huge decrease in Y. Among the components of GDP, investment dropped precipitously. Government spending did not compensate for the expenditure drops, at all.

What Happened During the Great Depression? Real money balances were relatively constant. Nominal interest rates dropped but deflation meant real interest rates were high.

Roaring Twenties • Extensive innovations in technology and business practices. • Rapid growth in American economic dominance. • Euphoria. • Stock market rise (by 9/29 it was 40% above its fundamental value).

Crash of October 1929 • The urban legend is: stock market crashed in October 1929 and that triggered the Great Depression. • The Stock Market Crash was not the cause but the effect of economic downturn and monetary policy of the Fed.

Economy before 10/29 • The US economy was already slowing down by the fall of 1929 largely as a result of monetary tightness. • Industrial production started to decline in July • Construction permits fell sharply in August and September. • Automobile sales dropped sharply in October • Interest rates in US and abroad were rising http://www.federalreserve.gov/boarddocs/speeches/2002/20021015/default.htm#pagetop

Stock Market Non-Crash of ‘29 • Stock prices did not collapse in 1929 but only began to plummet when the depth of the general economic decline became apparent. • Stock prices in April 1930 were still about the same level as in January 1929; and someone who bought stock in early 1928 and sold in October 1930 would have almost broken even. • Only as the bad economic news kept rolling in, in the fall of 1930, did stock prices finally fall below 1928 levels. http://www.federalreserve.gov/boarddocs/speeches/2002/20021015/default.htm#pagetop

Monetary Tightening • In 1928, while the inflation rate was actually slightly negative and the economy was only barely emerging from a mild recession, the Fed began to raise interest rates. • The New York Fed's discount rate, at 3.5 percent in January 1928, reached 6 percent by August 1929, its highest value since 1921. • Rates on term stock-exchange loans peaked in that month at almost 9 percent, and the rate on call loans exceeded 10 percent in early August. For short periods the rates on these loans sometimes spiked above 20 percent. http://www.federalreserve.gov/boarddocs/speeches/2002/20021015/default.htm#pagetop

Why Did the Fed Tighten? • To prick the stock market bubble. • As early as the mid-1920s, various policymakers and commentators expressed concern about the rapidly rising stock market and sought so-called corrective action by the Federal Reserve. http://www.federalreserve.gov/boarddocs/speeches/2002/20021015/default.htm#pagetop

Money Supply • Deflation, like inflation, tends to be closely linked to changes in the national money supply, defined as the sum of currency and bank deposits outstanding, and such was the case in the Depression. Like real output and prices, the U.S. money supply fell about one-third between 1929 and 1933, rising in subsequent years as output and prices rose.

Source: http://econ161.berkeley.edu/TCEH/Slouch_Crash14.html

Milton Friedman and Anna J. Schwartz • A Monetary History of the United States, 1867-1960 (1963). • Four errors by the Fed. • Tightening from 1928 on. • Sticking to gold standard and raising interest rates when USD was “attacked.” (1931) • Stopped easing monetary policy in 1932 because nominal interest rates were low. • Ignored the problems in the banking sector.

Monetary Tightening in 1928 • Commodity prices were declining sharply, little hint of inflation. • Fed was concerned that bank lending to brokers and investors was fueling a speculative wave in the stock market. When the Fed's attempts to persuade banks not to lend for speculative purposes proved ineffective, Fed officials decided to dissuade lending directly by raising the policy interest rate. http://www.federalreserve.gov/boarddocs/speeches/2004/200403022/default.htm

Gold Standard • Fixed exchange rates are subject to speculative attack if investors doubt the ability of a country to maintain the value of its currency at the legally specified parity. • In September 1931 scared speculators exchanged British pounds for gold in return. • Faced with the heavy demands of speculators for gold and a widespread loss of confidence in the pound, the Bank of England quickly depleted its gold reserves. Unable to continue supporting the pound at its official value, Great Britain was forced to leave the gold standard, allowing the pound to float freely, its value determined by market forces.

Gold Standard • With the collapse of the pound central banks as well as private investors converted a substantial quantity of dollar assets to gold in September and October of 1931, reducing the Federal Reserve's gold reserves. • The speculative attack on the dollar also helped to create a panic in the U.S. banking system. • Fearing imminent devaluation of the dollar, many foreign and domestic depositors withdrew their funds from U.S. banks in order to convert them into gold or other assets. • The worsening economic situation also made depositors increasingly distrustful of banks as a place to keep their savings and bank panics proliferated.

Fed’s Dilemma • To keep the gold standard means to protect the dollar by raising interest rates and making dollar attractive to hold. • To support the banking system means to provide funds to the banks under attack and be lender-of-last-resort by flooding the system with money and keeping interest rates low.

Fed’s Dilemma • Fed decided to ignore the plight of the banking system and focused only on stopping the loss of gold reserves to protect the dollar. • The attack on the dollar subsided and the U.S. commitment to the gold standard was successfully defended. • Fed chose to tighten monetary policy despite the fact that macroeconomic conditions--including an accelerating decline in output, prices, and the money supply--seemed to demand policy ease.

Easing or Not Easing • Congress began pressure the Federal Reserve to ease monetary policy. The Fed increased money supply between April and June of 1932. • Interest rates fell and the decline in prices and economic activity halted. Some Fed officials viewed the Depression as the necessary purging of financial excesses built up during the 1920s. Other officials, noting the very low level of nominal interest rates, concluded that monetary policy was in fact already quite easy and that no more should be done. • The ongoing deflation meant that the real cost of borrowing was very high because any loans would have to be repaid in dollars of much greater value. Thus monetary policy was not in fact easy at all, despite the very low level of nominal interest rates. • When the Congress adjourned in July 1932, the Fed reversed the policy. By the latter part of the year, the economy had relapsed dramatically.

Banking Sector • As depositor fears about the health of banks grew, runs on banks became increasingly common. Deposit insurance was virtually nonexistent, so that the failure of a bank might cause depositors to lose all or most of their savings. • A series of banking panics spread across the country, often affecting all the banks in a major city or even an entire region of the country.

Banking Sector • Between December 1930 and March 1933, when President Roosevelt declared a "banking holiday" that shut down the entire U.S. banking system, about half of U.S. banks either closed or merged with other banks. • Surviving banks, rather than expanding their deposits and loans to replace those of the banks lost to panics, retrenched sharply.

Banking Crisis • Because bank deposits are a form of money, the closing of many banks greatly exacerbated the decline in the money supply. • People hoarded cash. Hoarding effectively removed money from circulation, adding further to the deflationary pressures. • Shutting down of the U.S. banking system also deprived the economy of an important source of credit and other services normally provided by banks.

Bank Panics • “Many of the banks that failed during the panics appear to have been at least as financially sound as banks that were able to use alternative resolution strategies. This result supports the idea that the disruptions caused by the banking panics may have exacerbated the economic downturn.” Mark Carlson http://www.federalreserve.gov/pubs/feds/2008/200807/200807pap.pdf

Source: http://econ161.berkeley.edu/TCEH/Slouch_Crash14.html

Shrinking of Banks • There were 12,343 commercial banks and 2815 savings institutions in 1990. On March 31, 2009 there were 7037 commercial banks and 1209 savings institutions. • Number of failed institutions were in the single digits in the years 1995-2007. 878 institutions failed between 1990 and 1994. 25 institutions failed in 2008 and 21 in Q1 of 2009. http://www.fdic.gov/bank/statistical/stats/2009mar/FDIC.pdf

Great Depression • Governments tried to balance budgets, further slowing down the economy. • Huge deflation made bank collateral worthless in defaults. • Bank failures triggered bank panics. • Financial system ground to a stop. • Falling prices provided incentives to postpone investment.

Great Depression • Gold standard restricted countries to expand money supply only when they acquired gold as a result of trade surpluses. • Those countries that abandoned the gold standard (Scandinavian countries, Japan) slipped away from the Great Depression. • To acquire gold, countries passed protectionist policies (Smoot-Hawley in US).

Gold Standard and Trade • Smoot-Hawley was passed in June 1930. • Eichengreen and Irwin show that those countries that clung to the gold standard resorted most to protectionism. • http://papers.nber.org/papers/w15142 • http://www.economist.com/businessfinance/displaystory.cfm?story_id=14082148

Trade Shrank to 1/4th Between Jan. 1929 and Mar. 1933 Imports of 75 Countries. Source: E. Ray Canterbury, A Brief History of Economics, (World Scientific, Singapore: 2001), p. 209.

Ideologies/Policies That Exacerbated the Great Depression • Gold Standard • Classical theory • Fiscal Conservatism (Balanced Budgets) • Smoot-Hawley Protectionism • Tight Money (high interest rate) from bank failures • What is it? How does it operate? How did it contribute to the downfall?

Friedman suggested, the economy can grow faster than normal for a period until it reaches the point where it would have been without the crisis, when it reaches its full potential again. If the shortfall in demand persists it can do lasting damage to supply, reducing the level of potential output (scenario 2) or even its rate of growth (scenario 3). If so, the economy will never recoup its losses, even after spending picks up again. In a recession firms shed labour and mothball capital. If workers are left on the shelf too long, their skills will atrophy and their ties to the world of work will weaken. When spending revives, the recovery will leave them behind. Output per worker may get back to normal, but the rate of employment will not. http://www.economist.com/specialreports/displayStory.cfm?story_id=14530093 World Economic Outlook: cost of 88 banking crises over the past four decades. On average, seven years after a bust an economy’s level of output was almost 10% below where it would have been without the crisis.

Regulatory Legacy of Depression • The experience of the Depression helped forge a consensus that the government bears the important responsibility of trying to stabilize the economy and the financial system, as well as of assisting people affected by economic downturns. • Dozens of our most important government agencies and programs, ranging from social security (to assist the elderly and disabled) to federal deposit insurance (to eliminate banking panics) to the Securities and Exchange Commission (to regulate financial activities) were created in the 1930s, each a legacy of the Depression. http://www.federalreserve.gov/boarddocs/speeches/2004/200403022/default.htm

Historical Development of the Banking Industry Outcome: Multiple Regulatory Agencies 1. Federal Reserve 2. FDIC 3. Office of the Comptroller of the Currency 4. State Banking Authorities ici

http://delong.typepad.com/sdj/2009/03/delong-lessons-from-the-new-deal-for-today.htmlhttp://delong.typepad.com/sdj/2009/03/delong-lessons-from-the-new-deal-for-today.html • The government should not sit on its hands. • Prudent policy has to rely on all the tools • Monetary policy • Quantitative easing • Fiscal policy • Banking policy • Don’t let debates over reform block policies for recovery