Download

1 / 6

70 likes | 262 Views

It does not have a specific weightage but its techniques are used in other chapter like Non- profit organization, partnership,amalgamation,etc

E N D

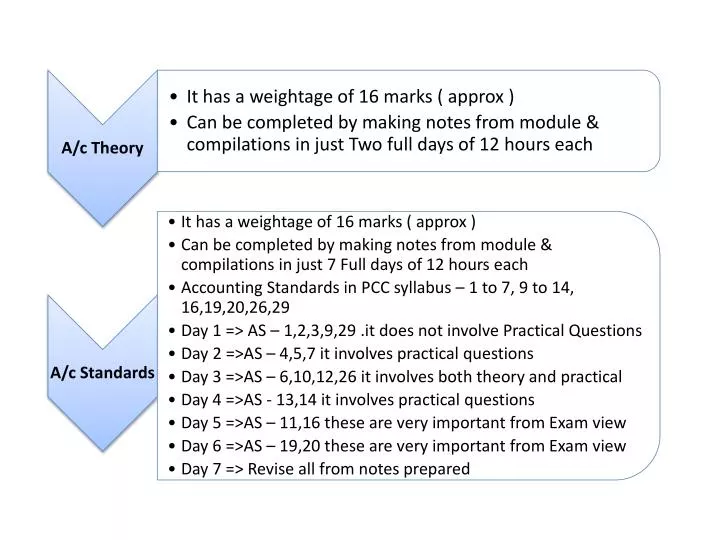

It does not have a specific weightage but its techniques are used in other chapter like Non- profit organization, partnership,amalgamation,etc • Can be completed in just one day by solving all questions asked in past examinations from compilations and module, just cover all the types of questions asked , no need to solve multiple questions of same type. • It’s a pure practical chapter so, no theory included. • Mark some good questions for revision purpose. • Single Entry • It has weightage of minimum 8 marks if combined with single entry system & has a potential to be asked for 20 marks also. • It can also be completed in just one day by solving all questions asked in previous examinations from compilations and modules, cover all possible type or pattern of asking question • Solve one or two question of each type of question • Mark some good questions for revision purpose. • It contains Theory also which is good in module. • Not for profit organisation

It does not have any specific weightage • It can be asked in journal entries form • So while making notes, make the note of journal entries in each case • It is given in module the journal entries • No need for practice, journal entries remains same, just figures keep changing. • Buy back, right issue,esops, forfeitue, etc • It has weightage of minimum 8 marks. • Determine the types of questions asked in past examinations and practice two to three problems of each type. • Banking – type of questions – Provisioning of NPAs, Journal entries for Rebate on Bill Discounting, etc • Insurance - type of questions – Revenue & profit & loss A/c • Electricity – type of questions – Loss on Replacement, Amount to be capitalised on replacement, Determination of distributable profits & Distributions of Profits. • Balance sheet is not expected to be asked in PCC • Module is more than enough for Chapter Electricity companies • Banking, Insurance & Electricity

It is a chapter which is to be studied with AS – 13 • It has limited questions so, easy to cover • It has transactions such as Bonus issue, right issue, dividend declared & sale of shares • Only important point in this chapter is-=>calculation of no. of bonus shares received, Dividend to be capitalised or treated as revenue, Profit & loss on sale as cost to be taken for this purpose should be weighted average cost. • Application of AS - 13 • Investment • A/c ing • Self balancing, A/c current & ADD • It has weightage of minimum 8 marks when combined with investment A/c . • It’s a pure accounting chapter having double entry and posting

Two type of questions are asked- • Calculation of loss of stock • Calculation of loss of profit • Module has more than sufficient questions on this chapter so do not refer any other book for this chapter. • It contains theory questions also like Average clause,etc • Insurance Claims • Liquidation of Compan • There are two types asked- • Statement of affairs – (Formatised) • Liquidators statement of Account ( T format ) • For Statement of Affairs u have remember the Order of payment on liquidation • For Liquidators statement of account also u need Order of payment on liquidation but there is only one important point that how much to Call from equity shareholders & how to Pay to equity shareholders in event that partly paid up shares also exist.

Two type of questions are asked- • Calculation of loss of stock • Calculation of loss of profit • Module has more than sufficient questions on this chapter so do not refer any other book for this chapter. • It contains theory questions also like Average clause,etc • Insurance Claims • Liquidation of Compan • There are two types asked- • Statement of affairs – (Formatised) • Liquidators statement of Account ( T format ) • For Statement of Affairs u have remember the Order of payment on liquidation • For Liquidators statement of account also u need Order of payment on liquidation but there is only one important point that how much to Call from equity shareholders & how to Pay to equity shareholders in event that partly paid up shares also exist.