Download

1 / 30

300 likes | 434 Views

Discover Financial Services. Zhifeng (Jack) Chen Gloria Ho Jonathan Li Swechha Salgia Jeremy Smith Zheng(Andrea) Zhang. RCMP presentation 12.06.2007. Agenda. Company Overview - Jack Business Model - Jonathan Industry Overview - Jeremey SWOT - Andrea Stock Performance – Swechha

E N D

Discover Financial Services Zhifeng (Jack) Chen Gloria Ho Jonathan Li Swechha Salgia Jeremy Smith Zheng(Andrea) Zhang RCMP presentation 12.06.2007

Agenda • Company Overview - Jack • Business Model - Jonathan • Industry Overview - Jeremey • SWOT - Andrea • Stock Performance – Swechha • RCMP Position - Swechha • Valuation: Multiplies - Gloria • Recommendation - Gloria

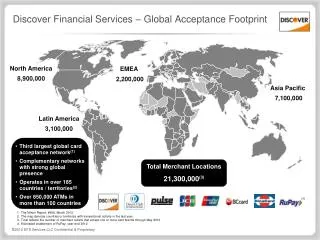

Company Overview • A leading credit card issuer and electronic payment service company in US and UK • Three major business segments: • U.S. card 50m card members, $47.4b receivable • Third party payment PULSE, 2.8b transactions • International card Goldfish Bank, 2m card members, $4.4b receivable • Primary revenue source: • Interest income • Securitization income • Fees from card members, merchants • Operating capital source: • Asset securitization • Consumer deposits

Recent Key News June 2007 officially spun off from Morgan Stanley July 1, 2007 DFS Added To S&P 500 July 2, 2007 DFS Debuts On NYSE Sept. 25 2007 DFS Profit Falls in the 3rd quarter ER due to higher marketing and interest expenses Dec. 3 2007 DFS to take big charge for UK card business in its 4th quarter ER (about $422M, equal to its half-year earning) Dec. 5 2007 Discovery's Consumer Spending Index Down 96.593.4 from Oct. to Nov.

Business Model Visa/MasterCard: $.25 Credit Card Company Credit Card Company Monthly Fee Monthly Fee Consumer Merchant Payment Network Consumer Merchant $100 $98 $1.75 Credit Card Issuer Discover: Credit Card Issuer • Discover owns all aspects of Credit card payment operations, and thus captures all revenue points in this model Transaction Fee

Revenue Breakdown *Mostly Credit Card revenue

Future Strategies • Focus on credit quality • Delinquency and charge-off rates significantly less than competition. • Average credit score 734. • Increase third-party revenues • Pulse network, debit cards. • International Partnerships • Reciprocal acceptance agreements with Asian credit card companies. • Challenge Visa/MasterCard dominance in this space.

Industry History • Diner Club Program, first general-purpose charge card established in 1949 • Bilateral Model • In late 1950s, Bank of America started to issue first credit card nationally, evolved toVisa network later on • Multiple Card Issuer Model • In 1966, MasterCard network was established • Multiple Card Issuer Model • American Express (1958) and Discover Card (1986) • single-issuer model

Credit CardIndustry • Highly competitive among concentrated market • American Express, Visa, Mastercard, Discover • Declining credit quality • Mortgage Crisis (for some) • Failure of loan payments • Increase in Charge-offs • DFS susceptible to loss rates • Heavily influenced from consumer spending • Threatened by tightening of lending practices

Credit Market "FDIC Quarterly Banking Profile ." Third Quarter 20072 December 2007 <http://www2.fdic.gov/qbp/2007sep/qbp.pdf>. • Home mortgage defaults biggest factor • Increase in bad loans expense (3rd quarter) • Loan-loss expense $16.6BN v. $7.5BN in 3rd quarter 06 • Net charge-offs up 200% last year • $10.7BN total (3rd quarter 07’) vs. $3.6BN(06’) • Significant decline in stock values of all the biggest US banks • DFS hurt from sale of asset backed loans to big investors • Further loss expected in near future

Current Market • Is a mature market • Estimated 76% of American families had credit card in 2001 • Average card number for all households: 6.3 • Nearly all retail establishments can process credit card

Strengths • “One-of-a-kind company”: • 4th-largest network, 6th-largest credit card issuer, owns the nation’s 3rd-largest debit network. • Potential as a top-tier issuer and processor in a secularly growing market. • Good credit quality: 3.12% delinquency rate 2Q07 • Focus on lending to the prime credit segment and strengthening its portfolio: no direct exposure to housing or housing credit market • Attractive and stable card member base • Higher income, better educated, higher percentage of home ownership • Highest percentage that cardmembers stay longer than 5 years • Possibility of a future acquisition

Weaknesses • Continued losses in DFS's U.K. business due to UK’s weak economy. • Lack of global diversification: • Recently inaugurated joint programs with China UnionPay and JCB in Japan. • Has no plans to expand in Europe or Latin America, where the usage of card is growing at double digit rate in selecting countries. • The core Discover Network business, experienced transaction growth of just 4.8% in 3Q07 comparing to MasterCard’s 15.3% in 2Q07 • Lower spending per card than peers: the active account rate is only 44%. Marketing the brand to a desirable product is a primary issue. • 0% introductory interest rate: 16 out of 17, or 94% of its lending card by discovery carries a 6 or 12 months APR, the highest percentage among peers, where industry average is 73% • Economy of scale: much smaller than Visa and MasterCard

Opportunities • Continued migration from cash spend to plastic and other electronic forms of payment within the U.S. and continued card penetration internationally • U.S. charge-offs were a solid 3.7% in Aug-Q • Possible take over target • Debit cards usage is growing much faster than the consumer spending and the card usage.

Threats • On housing and credit related issues, • Possible deterioration of US consumer confidence that would have an impact on consumer spending • A rise in unemployment that would pressure credit quality. • The competition of the industry is very intense: competitors offer identical or similar products

DFS Stock Performance • Closed at $ 16.45 on 5th Dec 2007 • 52 Week high low : $ 32.17 - $ 15.72 Source: Wall Street Journal : http://online.wsj.com/quotes/stock_charting.html?symbol

DFS Stock Performance • International losses have contributed to 39% decline since its spin-off especially Europe • International card business suffered $ 67 million pretax loss in the third quarter Source: Wall Street Journal : http://online.wsj.com/quotes/stock_charting.html?symbol

RCMP Position • DFS Position • 201 shares by virtue of spin off on 2nd July 2007 @ 19.52 per share • .87 % of RCMP Value • Total RCMP value as of 12/03/07 • $ 379895 Source: Yahoo Finance: http://finance.yahoo.com/p?k=pf_1

RCMP Profit/Loss • Net Profit as of 12/03/07 • $ 92173 • DFS Loss • $ 617 Source: Yahoo Finance: http://finance.yahoo.com/p?k=pf_1

RCMP LOSS • Total Loss as of 12/03/07 • $ 4499 • DFS Loss • $ 617.07 Source: Yahoo Finance: http://finance.yahoo.com/p?k=pf_1

Valuation • Difficulties in valuing DFS by cash flow and DCF • Profitability depend on • Interest spread on loans • Investment income • incl. profit / loss from sales of securities • Changes in market value • Loan quality • Young as a stand-alone company

Multiple Valuation * Figures represent trailing PE multiple. Forward earnings are applied to this multiple to arrive at valuation.

Recommendation • Short history as a standing along company • It’s hard to forecast whether the management is able to bring the company out of current trouble • Although multiple valuation gives a high target price, we are hesitant to recommend a buy at this juncture in the company’s young history Hold! Thank you!