Download

1 / 20

200 likes | 460 Views

U. S. Risk-Based Capital Requirements and Their Context. Alfred W. Gross Virginia Commissioner of Insurance National Association of Insurance Commissioners October 11, 2002. What is RBC? *. Basic formula compares reported capital to risk-based capital requirement

E N D

U. S. Risk-BasedCapital Requirements and Their Context Alfred W. Gross Virginia Commissioner of Insurance National Association of Insurance Commissioners October 11, 2002

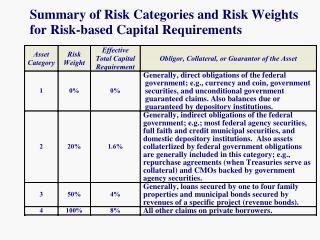

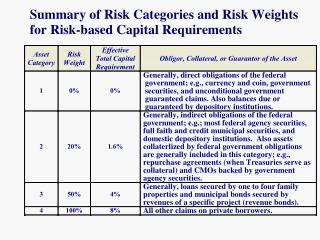

What is RBC? * • Basic formula compares reported capital to risk-based capital requirement • Requirement calculated by applying factors to various asset, credit, reserve and off-balance sheet items * taken from NAIC Financial Analysis Handbook Property/Casualty Edition, 2001 Annual

What is RBC? (continued) • Factor is higher for those items with greater underlying risk • Risk-based capital ratio is defined as a ratio of actual capital (i.e. “total adjusted capital”) divided by required capital (i.e. authorized control level risked based capital”) • Regulatory action taken on basis of this ratio

Standard U. S. Regulatory Filings:Financial Reporting • Annual Statements • Quarterly Statements • Management Discussion and Analysis • Actuarial Opinion • Annual Audited Financial Statements • Risk-Based Capital Report

Standardized Risk-BasedCapital (RBC) Report • Uniform Approach Across Companies and U. S. Jurisdictions • Based on U. S. Statutory Annual Statement Blank (A.S.) • Values are taken from A.S. and have no meaning outside of A.S. context + U. S. statutory accounting model • Formulas and calibration of results are based aggregate industry statistics taken from A.S. reporting

Standardized RBC Report (continued) • Based on historical financial reporting, not “forward looking” • Dependent on accounting definition of solvency (asset-liabilities) • Works within the “surplus geography” of the A.S., e.g., hidden margins in conservatively valued assets and technical provisions

The RBC System • Background: • 1993 Life • 1994 Property/Casualty • 1998 Health • Designed to provide regulators with some degree of control in monitoring risks taken by insurers • Designed to provide companies with some cost-benefit mindset in their asset allocation decisions

The RBC System (continued) • Tensions in Capital Regulation and Standards • Desire to minimize free surplus so as to focus investment in underwriting business and to use financial leverage (e.g., debt) to provide greater returns (management perspective) VS. Need to hold a minimum amount as free surplus to ensure company performance (regulator perspective)

The RBC System (continued) • Need for a straight-forward, transparent, legally workable and fair approach across all companies in a competitive market VS. Need to be sensitive to individual company characteristics, e.g., types of risks, levels of exposure, and management capabilities

The RBC System (continued) • RBC is a Regulatory Tool • Signaling mechanism between regulators and insurance companies as to poorly capitalized companies • Act as a tripwire providing clear regulatory authority for intervention at defined action levels • RBC is not: • A “silver bullet” to stop insolvencies • A system for ranking or rating companies • A precise diagnostic tool to define problematic companies

RBC Formulas • Life and Health • Property and Casualty • Health

Life RBC - Components • Insurance Affiliate Investment and Non-Derivative off-balance Sheet Risk (C0) • Invested Asset Risk - Common Stock (C1cs) • Invested Asset Risk - Other (C1o) • Insurance Risk or Pricing Risk (C2) • Interest Rate Risk (C3a) • Health Provider Credit Risk (C3b) • Business Risk - Guaranty Fund Assessment Risk (C4a) • Business Risk - Health Administration Expense Risk (C4b) • Covariance Adjustment

No Action Level Company Action Level Regulatory Action Level Authorized Control Level Mandatory Control Level 200% + 150% - 200% 100% - 150% 70% - 100% Under 70% RBC - Action LevelsTotal Adjusted Capital/Authorized Control Level RBC

Historical RBC Results(Life, Property and Health) 1996 1997 1998 1999 2000 No Action 3,799 3,740 3,707 3,870 3,953 Company 59 54 54 84 92 Regulatory 22 14 31 64 67 Authorized 11 8 22 23 28 Mandatory 31 27 43 46 53 Total 3,922 3,843 3,857 4,087 4,193 (Life - 1993; Property - 1994; Health - 1998)

Asset Risk-Affiliate (C0) Asset Risk-All Other (C1) Insurance Risk (C2) Interest Rate Risk (C3a) Health Credit Risk (C3b) Total (C3) Risk Business Risk-Prem/Liab (C4a) Business Risk-Health (C4b) Total (C4) Risk RBC After Covariance Authorized Control Level RBC $ 22.0 billion 23% $ 51.1 billion 53% $ 19.1 billion 20% $ 10.9 billion 11% $ 32.0 million <1% $ 10.9 billion 11% $ 3.7 billion 4% $533.6 million <1% $ 4.3 billion 4% $ 96.1 billion 100% $ 48.0 billion Life RBC - RBC Requirement &Percentage After Covariance

NAIC Accreditation: Base - LineLaws and Regulations • Key standards include: 1. Examination Authority 2. Corrective Action 3. Risked Based Capital 4. Reinsurance 5. Investments 6. Reserves 7. Receiverships 8. Guaranty Funds 9. Accounting Practices

Risk Assessment Working Group • Recognition of new financial services marketplace: rapid product innovation, convergence among the sectors, global competition, role of technology • Need for a “forward-looking” perspective responsive to the specific risk exposures of a company’s operations

General Goals • To create a framework for identifying and assessing risk exposures • Categorize risks • Analyze and evaluate risk exposures, both inherent and control risks • Document results in a manner useful in focusing regulatory oversight • Produce a type of risk profile or matrix for each company

General Goals (continued) • To make more effective current approaches to on-site examinations and on-going financial analysis by targeting resources to material risk exposures • To encourage insurers to establish effective risk management systems

Challenging Assumptions • Regulator’s reliance on internal company processes to identify, evaluate, and manage the risks. Has top management the ability to circumvent internal controls? • Increased reliance on work of outside auditors