Download

1 / 4

70 likes | 354 Views

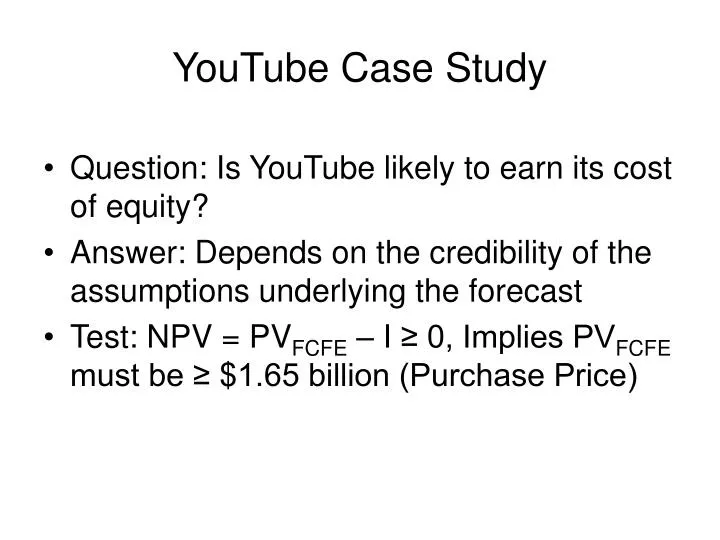

YouTube Case Study. Question: Is YouTube likely to earn its cost of equity? Answer: Depends on the credibility of the assumptions underlying the forecast Test: NPV = PV FCFE – I ≥ 0, Implies PV FCFE must be ≥ $1.65 billion (Purchase Price). YouTube Case Study: Estimating Base Year Cash Flow.

E N D

YouTube Case Study • Question: Is YouTube likely to earn its cost of equity? • Answer: Depends on the credibility of the assumptions underlying the forecast • Test: NPV = PVFCFE – I ≥ 0, Implies PVFCFE must be ≥ $1.65 billion (Purchase Price)

YouTube Case Study: Estimating Base Year Cash Flow • (Revenue/Month)YouTube = (Revenue/Unique Visitor/Month)About.com x YouTube Unique Visitors/Month = $.15 x 34 million = $5.1 million • (Net Income/Month)YouTube = (Revenue/Month)YouTube x Google net profit margin = $5.1 million x .25 = $1.28 million 3. Assuming depreciation equal capital spending and Δworking capital zero, then base year free cash flow to equity (FCFE) is FCFEFullYear = (Net Income/Month)YouTube x 12 = $1.28 million x 12 = $15.4 million

Underlying Assumptions • To realize a PVFCFE≥ $1.65 billion if discounted at 10%, we have to assume • Base year FCFE would have to grow at least 225 percent annually for the next 15 years • FCFE would grow at 5 percent annually during the terminal period Results: • PVTV = $1,005 million • Total PV = $1,610 million • PV15yrs = $ 605 million

Sensitivity Analysis • Assuming a higher revenue per unique visitor figure would result in a lower projected rate of growth of free cash flow to equity • However, assuming YouTube’s cost of equity is the same as Google’s may be optimistic. A higher discount rate to reflect YouTube’s probable higher level of risk would offset assumed higher revenue per unique visitor figure.