Download

1 / 2

20 likes | 33 Views

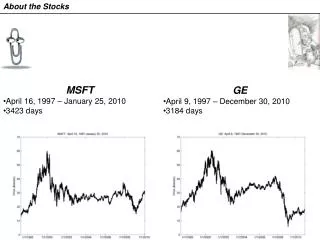

Pieter Stalenhoefu2019s analysis allows him to reach the conclusion that value stocks have been underperforming in the United States since 2007 mainly because the condition has not been so good for the past 13 years and even then, considering value investing to be obsolete can never be acceptable. Pieter emphasizes this with great conviction as he has observed value outperforming growth over longer periods and also derives references from various historical trends that speak volumes about the same.

E N D

Pieter Stalenhoef Talks About His Analysis About Performance of Value Stocks Pieter Stalenhoef explains that even though value stocks trade below market value and often have very strong fundamentals, they are undervalued for several reasons. He has spent quite some time observing these stocks and he loves to talk about how these present an exciting opportunity for the investors to buy great stocks at low prices way before the market correction takes the price to its actual price. Pieter Stalenhoef has worked in several roles and responsibilities over the years and one of these positions even required him to spend a lot of time analyzing global small and mid-cap equities while focusing specially on consumer and healthcare stocks. In addition to that, his responsibilities included keeping a track of global stock trends and performance of growth stocks over value stocks over the last 10 years. As far as the difference between growth stocks and value stocks is concerned, he explains growth stocks as stocks that investors believe will surely outperform the market

with time. He goes on to explain that growth stocks are usually managed by companies that have a high potential for growth or expansion. These may include tech companies. Pieter Stalenhoef’s analysis allows him to reach the conclusion that value stocks have been underperforming in the United States since 2007 mainly because the condition has not been so good for the past 13 years and even then, considering value investing to be obsolete can never be acceptable. Pieter emphasizes this with great conviction as he has observed value outperforming growth over longer periods and also derives references from various historical trends that speak volumes about the same. He also cites a study published in the Financial Planning Magazine which sheds enough light on the fact that the returns on value stocks outperformed those on growth stocks over a period of 25 years (1990- 2014). It doesn’t come to Pieter as a surprise that the value stocks have been seen doing good even during the periods of stunted growth.