Download

1 / 17

170 likes | 180 Views

Explore how modern structured finance, specifically Credit Default Swaps, could revolutionize philanthropy, making capital flow readily to programs that effectively address social problems. Learn about Impact Backed Securities (IBS), Savings Failure Swaps (SFS) and Savings Backed Securities (SBS).

E N D

How Credit Default Swaps Could Change the World By Mary Kopczynski, J.D./Ph.D.

Finance = Technology • When the internet was created, for-profit companies used it first. It wasn’t until later that non-profits and foundations started developing websites. Now it is critical for non-profits and foundations to have websites. • Credit Default Swaps weren’t invented until 1994 and it became a 60 trillion dollar industry in ten years. If we could get over the stigma and ensure a safer, more transparent system, modern structured finance could be used to revolutionize philanthropy as we know it.

Asset Backed Securities An asset-backed security is a structure where interest bearing assets are pooled together in a kind of company called a special purpose vehicle or SPV. Depending on their risk-tolerance, investors would buy notes in what is called a “waterfall.” Low risk investors who wanted their money back safely would buy the Series A note where they would be paid first before all others. Once Series A notes were all paid out, then the cashflows would go to the Series B noteholders. Once Series B was paid out, then Series C would be paid out and so on and so forth until there was nothing left but the equity tranche. The remaining assets would then be sold off and the equity tranche noteholders would received the remaining proceeds.

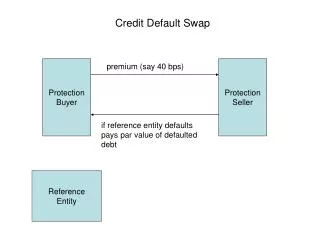

Credit Default Swap Credit Default Swap When Series A note holders were particularly worried, they could enter into a credit default swap. In a credit default swap (CDS), another party will agree to pay the Series A note holder in the event that the SPV fails to deliver its revenue stream. While CDS are similar to insurance, the difference is the way “failure” is specifically defined and also the way the failure event is priced. In other words, similar to insurance, a credit default swap will pay out if the note does not. So what does this have to do with philanthropy????

The Current Philanthropic System Every day, 115 new non-profits register with the IRS. 93% of them operate on less than $1M annually. Charities spend 70% of their time organizing fundraising events or filling out lengthy grant proposals to receive funding. Governments shell out billions for social services. Foundations are for-profit structures that are obligated to give 5% to charities but the remaining 95% go to normal for-profit investments. Only 2% of foundations are using capital in program-related investments where they receive a return from loaning capital to non-profits. • The Result: • Capital flows are fragmented and uncoordinated. • Charities are not able to spend their time doing what they do best, which is to address a social problem. • Social problems still exist.

Phase I: IBS We can do better. Phase II: SBS What if we built a system where capital flowed readily to programs that had demonstrated success in reducing social problems? Measurement would be critical. (How do you know your program is the one that kept a social ill from occurring?) Language would be critical. (This concept would disrupt a lot of industries that will resist change.) A pilot and testing phase would need to be coordinated. Phase III: ABS

Savings Failure Swap Phase I: Impact Backed Securities Similar to an SPV, an impact backed security is a impact purpose partnership (IPP) that has a measurable objective that, if achieved, would reduce the government’s expenses associated with servicing that social problem. The only “investors” in Phase I would be foundations. The capital raised would be provided to non-profits targeting that social problem. Non-profits report their progress regularly until the target is achieved or a set deadline occurs.

Savings Failure Swap Phase I: Impact Backed Securities Example: The agreed upon target is to reduce the homeless population of a city by 2%. The city pre-agrees to pay a given sum if the impact target (reduction in population and therefore a reduction in their future expenses) is achieved. Upon success, Bedrock Supporters get the “impact” they desire. Tier II Supporters get back their investments. Tier III Supports get back their investment plus a return. Upon failure, Bedrock Supporters have knowledge about which non-profit strategies are impactful. Tier II Supporters get whatever part of their principal is possible. Tier III Supporters get back a portion of their principal from another Foundation that agreed to provide a Savings Failure Swap.

Savings Failure Swap Phase II: Savings Backed Securities Similar to an impact backed security, a savings backed security is a impact purpose partnership (IPP), but it only focuses on reducing expenses associated with social problems. Phase II could include traditional commercial investors, impact investors and foundations. The capital raised would be provided to non-profits targeting that social problem. Non-profits report their progress regularly until the target is achieved or a set deadline occurs.

Savings Failure Swap Phase II: Savings Backed Securities Example: The agreed upon target is to reduce the homeless population of a city by 2%. The city pre-agrees to pay a given sum if the impact target (reduction in population) is achieved. Upon success, Bedrock Supporters get the “impact” they desired. Tier 1-3 Investors get back their principal plus a return, depending on the savings achieved. Upon failure, Bedrock Supporters have knowledge about which non-profit strategies are impactful. Those tiered investors who chose to enter a Savings Failure Swap would get their allotted recovery rate.

What would this mean to philanthropy? Instead of capital flowing to the charities that are best at fundraising, capital would flow to the charities that are the best at eliminating the problem.

We’d spend less time connecting causes with funding! • Depending on their interests and capital risk tolerance, foundations could “buy a note” on an issue, say women’s health or ocean clean-up. • If they are pleased with the impacts, they can buy another round. • No more lengthy applications to read or write!

So what is the catch? • Poorly run charities will go out of business.

Measurement is key. • Measurement issues are critical. Problems need to be demonstratively reduced in order to link to financial savings. • This is why the first instruments should be impact-backed securities for foundations only and not saving-backed securities. • We can test the measurement process and only be risking grant money that was meant to be given away anyway. • Once the methodology is sound, savings-backed securities will naturally lead to asset-backed securities Some issues will never be measurable in mathematically concrete ways, so they will never be a recipient of this type of funding.

Regulation? Yes, please. • Derivative technology requires transparency. • Intermediaries need to be properly regulated. • Legal/finance fees must not be egregious.

Thanks for reading and feel free to contact me with questions! Mary Kopczynski, J.D./Ph.D. CEO, Eight of Nine Consulting, LLC 1115 Broadway, 12th Floor New York, NY 10010 917.261.3902 maryk@8of9consulting.com www.8of9consulting.com Be sure to follow the make [*]it happen team on Twitter! @8of9consulting @MaryKopczynski