Download

1 / 24

240 likes | 297 Views

Learn about the fundamentals of double entry accounting, cash versus accrual accounting, concepts of debit and credit, classification of accounts, and the importance of financial statements in maintaining accurate records. Develop a solid foundation in accounting principles.

E N D

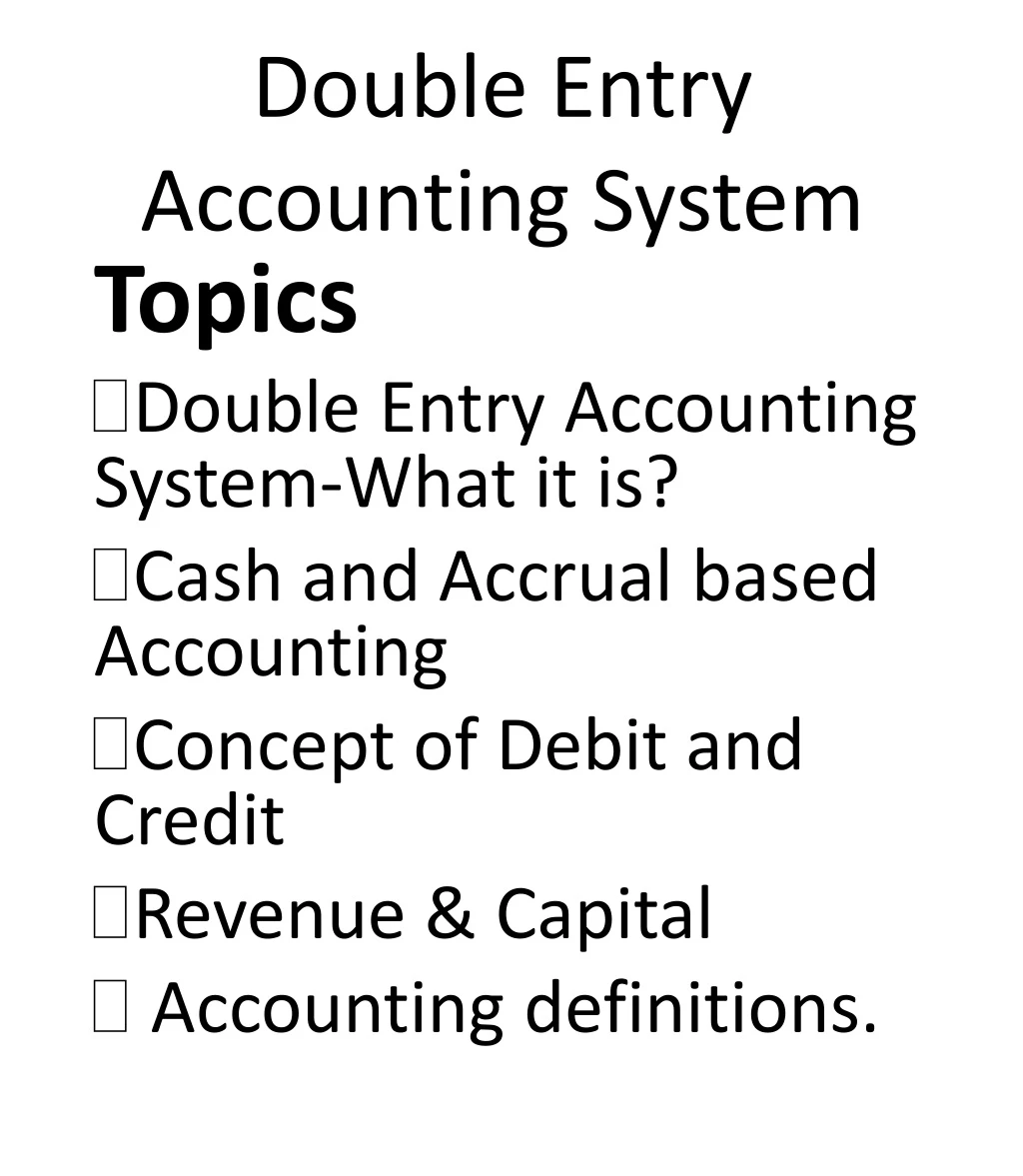

Double Entry Accounting System Topics Double Entry Accounting System-What it is? Cash and Accrual based Accounting Concept of Debit and Credit Revenue & Capital Accounting definitions.

What is Accounting? Accounting is an art of recording ,classifying and summarizing the financial information in a significant manner.

Single Entry System • Under this system both the aspects of transaction are not recorded. • Only Personal accounts & cash book are opened. • Under this system balance sheet is not prepared. This system is therefore not considered as an authentic one.

Double Entry Accounting System Based on principle of duel aspect of each transaction. For correct presentation both of them should be recorded. Requires maintenance of records of assets, liabilities, revenues and expenditure. Impact of each transaction can be seen or measured. Total assets are equal to total equities.

Classification of Accounts • Personal Account • Real Account • Nominal Account

Personal Account • Definition & Examples of accounts:- • Personal Account: Personal accounts are accounts relating to persons or organisations with whom the business has transactions. E.gCustomer, Supplier, Money lenders etc.

Real Accounts • Real Accounts: Real accounts refer to accounts in which property and possession are recorded. E.gLand, Building, Plant & Machinery, Vehicle Cash, Bank etc.

Nominal Accounts • Nominal Accounts: Nominal accounts are revenue, expenses, gains, and losses. E.g. Wages, Salary, Discount etc .

Concept of Debit & Credit(Golden Rules) • For Personal Accounts :Debit the receiver and credit the giver. E.g. Furniture has been purchased from Godrej & Boyce Ltd on credit of Rs.2,00,000/- Journal Entry: Furniture A/C Dr. Rs.2,00,000/- To Godrej & Boyce Ltd Cr. Rs.2,00,000/-

Concept of Debit & Credit(Golden Rules) • For Real Accounts: Debit what comes in and credit what goes out. A vehicle has been purchased of Rs. 8,00,000/- by cheque. Journal Entry: Vehicle A/C Dr. Rs.8,00,000/- To Bank Cr. Rs.8,00,000/-

Concept of Debit & Credit(Golden Rules) • For Nominal Accounts: Debit all expenses (and loses) and Credit all incomes(and gain). E.g Telephone bill amounting to Rs.25,000/- paid by cheque. Telephone Expense A/c Dr. Rs.25000/- To Bank A/c Cr. Rs. 25000/-

Double Entry Accounting System classification • Cash Based :- Cash basis of accounting is a method of accounting in which transactions are recorded in the books of account when cash is actually received or paid out. Eg .Property Tax has been received of Rs.10,000/- Cash A/C Dr Rs.10,000/- To Property Tax Cr. Rs.10,000/-

Accrual Based Accrual Based:- Accrual basis of accounting is an accounting system which recognises revenues and expenses as they are earned or incurred , not as cash received or paid respectively. Eg .Raised demand and sent Property Tax bills of Rs.10,000/- on 10th May2014 and the same amount has been received against the demand on 30th May,2014.

Accrual Based 10.05-2014 Property Tax Receivable A/C Dr 10,000/ To Property Tax A/C Cr. 10,000/- 30-05-2014 Cash/Bank A/C Dr 10,000/- To Property Tax Receivable A/C Cr 10,000/-

Accrual Based • A)Received a bill for construction of road from NBCC Ltd for Rs.10,00,000/-(Bill Processed and deductions made Security Money Rs.1,00,000/-,TDS Rs.50,000/- ,TVAT 1,20,000,labour Cess Rs.10,000/-) on 30th May,2014. • B)Paid Rs.7,20,000/- to NBCC Ltd on 3rd June,2014. 30-05-2014 Roads A/C Dr 10,00,000/- To, Security Money 1,00,000/- To, TDS, Income Tax 50,000/- To, TVAT 1,20,000/- To, LabourCess 10,000/- To, NBCC Ltd 7,20,000/- 3-06-2014 NBCC Ltd A/C Dr 7,20,000 /- To, Bank 7,20,000/-

Capital and Revenue Expenditure Capital expenditure is the expenditure where the benefits are not fully consumed in a year but spread over several years. Revenue Expenditure is the expenditure which provides benefits in the current accounting year only. It can not be forwarded to next year or years.

Primary Accounting Documents • Following primary accounting documents have to be maintained: • Receipt Vouchers • Payment Vouchers • Fund Transfer Vouchers/Contra Vouchers. • Journal Vouchers

Primary Books of Accounts Before preparation of Financial Statements we have to prepare following primary books of accounts: • Cash book • Bank book ( incl. Bank Reconciliation Statement) • Journal book • Ledger • Trial Balance

Financial Statement • Receipts & Payments Statement. • Income & Expenditure Account. • Balance Sheet.

Why the Financial Statement is mandatory for ULB. • To know the actual position of the assets, liabilities and reserve of the ULB. • Shows the position of general fund of ULB.