Download

1 / 19

190 likes | 209 Views

Learn the fundamental concepts of accounting, including the accounting equation, double-entry system, assets, liabilities, and owner's equity. Master the recording of financial information, revenues, and expenses, and understand debit and credit rules with real-life examples.

E N D

CHAPTER 2A: ACCOUNTING PROCESS, EQUATION AND DOUBLE ENTRY BASIC FINANCIAL ACCOUNTING MGT 2304 MOHD ZARIR YUSOFF

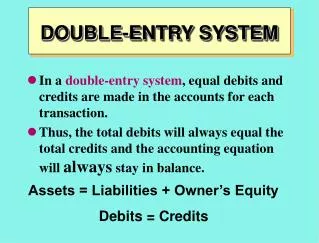

ACCOUNTING EQUATION ASSETS = LIABILITIES + OWNER’S EQUITY • This equation will remain unchanged and will be the accountant guideline in performing the accounting cycle (journal until financial statements' preparation) • Assets • The economic resources owned by a business entity which are capable of providing services or benefits in future. • Example: Cash, inventory, land, machinery, bank account, furniture, equipment, building and account receivables. • Liabilities • The amount due to a third party. • Example: Bank overdraft, accounts payable/creditors, mortgage, short-term loan and long-term loan. • Equity • The owner’s residual claims of the business assets. In other word it refer to 2 important things a) the movement of capital investment of the investors (capital – drawing) and b) profit or loss that the company experienced through out the years (revenues –expenses) Example: Capital, Drawing, Revenues items and Expenses items.

OWNER’S EQUITY = (CAPITAL – DRAWING) + or - (REVENUES – EXPENSES) • Revenues • The gross inflow of economic benefits during the period arising in the course of the ordinary activities of an enterprise when those inflows result in increases in equity, other than increases related to contributions from equity participants. For example: increase in assets as a result of the sales of goods and services, fees, interest, dividends, royalties, grants and rent. • Expenses • The decrease in economic benefits during the period in the form of outflows or depletions of assets or the increase in liabilities that result in decreases in equity, other than those related to distributions to equity participants. Expenses include both expenses and losses. Examples of expenses are utilities, wages, selling and administrative expenses.

DOUBLE-ENTRY SYSTEM • Each transaction will have at least dual side effect, which are debit and credit • Recording transaction will involve 2 accounts or 2 side of the same account with 1 debit and 1 • Debit mean received value while credit mean given value

ACCOUNTING EQUATION ASSETS • FIXED ASSETS • Furniture • Vehicles • Buildings / premises • Land • Machinery • CURRENT ASSETS • Inventories • Investments • Bank • Cash • Debtors / Account Receivable • INCREASE = DEBIT • DECREASE = CREDIT

ACCOUNTING EQUATION LIABILITIES • Loan from Bank • Creditors / Accounts Payable • Unpaid Business Expenses • Eg. Accrued Utility Expenses • (Water and Electricity) • INCREASE = CREDIT • DECREASE = DEBIT

ACCOUNTING EQUATION OWNER EQUITY = (CAPITAL- DRAWINGS) +(REVENUES-EXPENSES) • CAPITAL • DRAWINGS • INCREASE = CREDIT • INCREASE = DEBIT

ACCOUNTING EQUATION OWNER EQUITY = (CAPITAL- DRAWINGS) +(REVENUES-EXPENSES) • REVENUES • Sales Revenues • Rental / Land Revenue • Services Revenues • Interest Revenue • EXPENSES • Cost of Good Sold • Purchase • Rental Expenses • Water Expenses • Depreciation • Operating Expenses • Admin Expenses • Salaries • INCREASE = CREDIT • INCREASE = DEBIT

DOUBLE-ENTRY SYSTEM • Each transaction will have at least dual side effect, which are debit and credit • Recording transaction will involve 2 accounts or 2 side of the same account with 1 debit and 1 • Debit mean received value while credit mean given value

EXAMPLES • START UP A NEW BUSINESS • OWN MONEY • BORROW FROM BANK • RAZAK INVESTED CASH OF RM700,000 INTO HIS TUG BOAT BUSINESS, MEGAH MARITIM SDN BHD ON 1 JAN 2011. • THE COMPANY ALSO RECEIVED BANK LOAN FROM BANK PEMBANGUNAN AMOUNTING 1,300,000 WITH REPAYMENT PERIOD FOR 20 YEARS ON 24 FEB 2011

PURCHASE OF MACHINERY • BY CASH OR • BY CREDIT • MEGAH MARITIM SDN BHD HAVE PURCHASE 4 UNIT OF TUG BOAT AMOUNTING RM 125,000 EACH ON 3 MAC 2011. THE COMPANY USED RM 250,000 FROM THE BANK ACCOUNT FOR THE TRANSACTION WHILE THE RST ON CREDIT WITH THE SUPPLIER. • ON 5 MAC 2011, THE COMPANY PROPOSED TO THE TOP MANGAMENT FOR THE ACQUISITION OF 2 UNIT OF TUG BOAT WITH THE TOTAL COST OF RM 200,000

REVENUE RECEIVED EITHER • VIA SELL OF PRODUCTS OR • VIA SELL OF SERVICES • THE COMPANY RECEIVED RM 50,000 ON CREDIT FROM MSC LOGISTIC ON 20 MAC 2011 FOR THE TUG BOAT SERVICE PROVIDED BY THE COMPANY • THE COMPANY RECEIVED RM 75,000 ON CASH FROM MAERSK MALAYSIA FOR THE PILOTAGE AND TUG BOAT SERVICES PROVIDED ON 30 MAC 2011 • PORT OF TANJUNG PELEPAS SDN BHD HAVE PROMISED THE COMPANY IN THEIR MOA THAT THEY WILL PROVIDED 200 UNIT OF VESSEL FOR THE COMPANY TO SERVE IN 2011 AMOUNTING RM 15 MILLION

WITHDRAWAL OF MONEY FOR PERSONNEL USE • ON 18 MEI 2011, RAZAK HAVE WITHDRAW RM 50,000 FOR THE COMPANY ACCOUNT FOR HIS PERSONNEL USE

LIST OF BUSINESS’S TRANSACTIONS AND HOW IT AFFECTING THE DOUBLE ENTRY SYSTEM • STARTED BUSINESS WITH • CAPITAL INVESTMENT • ↑ A(CASH), ↑ E(CAPITAL)` • LOAN FROM BANK • ↑A(CASH), ↑ L(LOAN) • BOTH CAPITAL AND LOAN FROM BANK • ↑A(CASH), ↑ E(CAPITAL), ↑ L(LOAN)

PURCHASE ASSETS (BUILDING) ON • CASH • ↑A(BUILDING), ↓A(CASH) • CREDIT • ↑A(BUILDING), ↑L(CREDITOR) • PAYMENT TO CREDITOR • ↓A(CASH), ↓L(CREDITOR) • PURCHASE OF “GOOD TO BE SOLD” BY • CASH • ↓A(CASH), ↓E(PURCHASE EXPENSES) • CREDIT • ↓E(PURCHASE EXPENSES), ↑ L(CREDITOR)

PAYMENT OF EXPENSES(SALARY EXPENSES) • ↓A(CASH), ↓E(SALARY EXPENSES) • SELL OF GOODS/SERVICES (REVENUE) • ON CASH • ↑A(CASH), ↑E(SALES REVENUE/SERVICES REVENUE) • ON CREDIT • ↑A(DEBTORS), ↑E(SALES REVENUE/SERVICES REVENUE) • PAYMENT OF LOAN • ↓A(CASH), ↓L(LOAN) • PAYMENT FROM DEBTOR • ↑A(CASH), ↓A(DEBTOR) • WITHDRAWAL OF MONEY FOR PURCHASE OF GOODS FOR “PERSONAL PURPOSE” • ↓A(CASH), ↓E(DRAWING)