Download

1 / 17

170 likes | 262 Views

Long-Run Growth and International Saving Flows. Claude BISMUT University Montpellier-I. Globalization from goods to capital markets.

E N D

Long-Run Growth and International Saving Flows Claude BISMUT University Montpellier-I

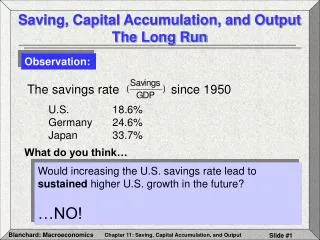

Globalization from goods to capital markets • Together with trade liberalization, the integration of capital markets has been one of the major long-run trends of the world economy over the last sixty years. • It was believed to foster growth, in particular in developing countries, thus speeding up convergence. • What can we reasonably expect from capital market integration? • Has it worked as expected? • How could the outcome of this process be improved? Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

I. What can we expect from international financial integration? • Welfare increasing? Because households have a larger choice. • Speeding convergence? Because foreign saving can supplement insufficient domestic resource for investing in less developed countries. • More growth? Because market forces enhance private efficiency and government discipline. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

1. Consumption smoothing Integrated capital markets allow to smooth consumption against asymmetric shocks. • A country can borrow in bad times and lend in good times. • Aging countries can transfer savings to young countries. • Consumption smoothing is welfare increasing • Current account deficits are not a concern, if sustainable. • On average, does not lead to faster growth. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

2. Financial integration and convergence • Open domestic capital markets, savings will move from low to high return places. • This does not change the long run rate of growth but speeds up convergence. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Essence of the neoclassical argument • Two countries, DC and LDC, have the same neoclassical production function, ... Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Essence of the neoclassical argument …, but, initially, DC is much more capital intensive than LDC. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Essence of the neoclassical argument Two domestic capital markets: neoclassical theory predicts convergence in the long run. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Essence of the neoclassical argument Merge the two capital markets in a unique global one: then, savings move rapidly from DC to LDC. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

3 Factors enhancing growth Foreign investment bears the seeds of efficiency gains. • FDI favors transfers of technology and importation of management practices. • Portfolio investment accelerates the development of the equity market. • Governments are subject to markets’ judgement, which enhances discipline. • Opening the current account is also expected to increase the efficiency of domestic banks. • However capital flows must be directed toward productive investments. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Less developed countries : net capital inflows Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

II. Has financial integration delivered its expected benefits? • Financial opening does not necessarily bring about more convergence or more growth. • Current account imbalances are not a concern if countries remain solvent. • Catching-up works on average, but not for all LDC. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

1 Is the internationalization of savings actually at work? Disconnection between saving and investment • Close correlation found between saving and investment in the 80s and early 90s raised doubts on capital mobility. • One reason is that governments have implemented macro policies to contain current account deficits. • More recent evidence indicates that investment and saving have actually been disconnected, and that internationalization of savings is at work. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

2 Who’s afraid of current account imbalances? Current account imbalances have to be accepted do not automatically lead to convergence. • Opening the current account and refusing deficit is somewhat contradictory. • But deficit have to be sustainable. • Governments are under markets judgement, and fear financial crises and sharp exchange rate corrections. • Sound macroeconomic policy is crucial. • But faster convergence will not necessarily follow. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

3 Has the convergence process been effective? At work on average, but not for all. • Some economies -- notably in transition -- have benefited from globalization. • Less developed countries still have too limited access to capital markets. • However, there is some evidence of negative correlation between growth and income per head. • But too many countries remain trapped in a vicious circle. Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Convergence is at work Global Convergence Scenarios, OECD Workshop, Jan. 16,2006

Concluding remarks :Strategy for growth and convergence Global Convergence Scenarios, OECD Workshop, Jan. 16,2006