Download

1 / 0

0 likes | 113 Views

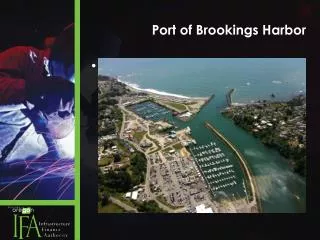

Port and Harbor funding assistance through shared fish taxes . October 11, 2011 Prepared by the Office of Rep. Seaton. Well maintained Port and Harbor facilities are critical to the economic health of communities. The ownership transfer of Harbors from the State to Municipalities has.

E N D