Download

1 / 5

0 likes | 10 Views

QuickBooks is a widely used accounting software that provides various financial reports to help businesses manage their finances efficiently. One of the most important reports is the Profit and Loss (P&L) report, which summarizes the revenues, costs, and expenses incurred during a specific period. This report is crucial for understanding your businessu2019s financial performance. However, users may occasionally encounter issues where the Profit and Loss report shows incorrect data. This comprehensive guide will help you identify the common causes of these errors and provide step-by-step solutions

E N D

QuickBooks Profit and Loss Report Wrong Problem QuickBooks is a widely used accounting software that provides various financial reports to help businesses manage their finances efficiently. One of the most important reports is the Profit and Loss (P&L) report, which summarizes the revenues, costs, and expenses incurred during a specific period. This report is crucial for understanding your business’s financial performance. However, users may occasionally encounter issues where the Profit and Loss report shows incorrect data. This comprehensive guide will help you identify the common causes of these errors and provide step-by-step solutions to resolve them. Understanding the Profit and Loss Report

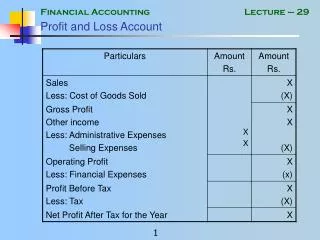

The Profit and Loss report, also known as the Income Statement, provides a snapshot of a company’s financial performance over a specific period. It includes the following key components: 1. Revenue: Total income from sales and other sources. 2. Cost of Goods Sold (COGS): Direct costs attributable to the production of goods sold by a company. 3. Gross Profit: Revenue minus COGS. 4. Operating Expenses: Expenses incurred during regular business operations. 5. Net Profit: Gross profit minus operating expenses and other non-operating expenses. Accurate P&L reports are vital for making informed business decisions, securing loans, and assessing profitability. Common Causes of Incorrect Profit and Loss Reports Several factors can lead to inaccuracies in the Profit and Loss report: 1. Incorrect Data Entry Errors in entering data into QuickBooks can cause discrepancies in the P&L report. This includes incorrect amounts, wrong accounts, or duplicate entries. 2. Misclassified Transactions Transactions might be recorded under incorrect categories or accounts, leading to misrepresentation of financial data. 3. Unreconciled Accounts Unreconciled bank or credit card accounts can result in missing or duplicate transactions, affecting the accuracy of the P&L report. 4. Incorrect Report Settings Using incorrect date ranges, filters, or report settings can lead to incomplete or incorrect data in the report. 5. Issues with Inventory Tracking

Errors in inventory tracking, such as incorrect item quantities or values, can distort the COGS and overall profitability. 6. Software Glitches Occasional software bugs or glitches within QuickBooks can cause data to be displayed incorrectly. Troubleshooting Steps Step 1: Verify Data Entry ● Review Transactions: Go through your transactions to ensure that all entries are correct. Check for any duplicate or incorrect entries. ● Edit Transactions: Correct any mistakes by editing the transactions. Ensure that the amounts, dates, and accounts are accurate. Step 2: Check Account Classification ● Review Chart of Accounts: Ensure that all accounts are correctly categorized as income, expenses, assets, liabilities, or equity. ● Reclassify Transactions: Use QuickBooks’ reclassification tool to move transactions to the correct accounts if necessary. Step 3: Reconcile Accounts ● Bank Reconciliation: Regularly reconcile your bank and credit card accounts to ensure all transactions are accounted for. ● Resolve Discrepancies: Investigate and resolve any discrepancies found during the reconciliation process. Step 4: Adjust Report Settings ● Set Correct Date Range: Ensure the date range for the report is set correctly to capture all relevant transactions. ● Check Filters: Verify that no unnecessary filters are applied that might exclude certain transactions from the report. Step 5: Verify Inventory Tracking ● Review Inventory Items: Ensure all inventory items are correctly tracked, with accurate quantities and values.

● Adjust Inventory: Make necessary adjustments to inventory quantities or values to reflect the actual stock on hand. Step 6: Update and Repair QuickBooks ● Update Software: Ensure you are using the latest version of QuickBooks. Updates often include bug fixes that can resolve reporting issues. ● Run Repair Tool: Use QuickBooks’ built-in repair tools to fix any potential data file issues. Additional Tips and Best Practices 1. Regular Audits: Conduct regular internal audits of your financial data to catch and correct errors early. 2. Consistent Data Entry: Implement consistent data entry practices to minimize errors. Train employees on proper data entry procedures. 3. Utilize Classes and Locations: Use classes and locations in QuickBooks to track income and expenses by department, product line, or location, enhancing the accuracy of reports. 4. Backup Data: Regularly back up your QuickBooks data to prevent data loss and facilitate easy recovery in case of errors. 5. Professional Help: Consider hiring a certified QuickBooks ProAdvisor or accountant to review your books periodically and ensure accuracy. Resolving Specific Issues Duplicate Transactions ● Identify Duplicates: Use QuickBooks’ duplicate transaction detection feature or manually review your transactions to identify duplicates. ● Delete or Merge: Delete duplicate transactions or merge them if they represent the same financial activity. Incorrect Income or Expense Categorization ● Review Income and Expense Accounts: Ensure that all income and expense transactions are recorded in the correct accounts. ● Reclassify as Needed: Use the reclassification tool to move transactions to the appropriate accounts. Missing Transactions

● Check Filters: Ensure that report filters are not excluding relevant transactions. ● Verify Data Import: If transactions are imported from external sources, verify that all data was imported correctly. Mismatched Inventory ● Conduct Physical Inventory Count: Periodically conduct physical counts of your inventory and compare them to QuickBooks records. ● Adjust Inventory Records: Make necessary adjustments in QuickBooks to match the physical inventory count. Software Issues ● Run QuickBooks Diagnostic Tool: Use the QuickBooks Diagnostic Tool to identify and fix software-related issues. ● Contact Support: If software issues persist, contact QuickBooks support for further assistance. Final Thoughts Maintaining accurate Profit and Loss reports in QuickBooks is essential for effective financial management and decision-making. By systematically troubleshooting and addressing the common causes of errors, you can ensure the reliability of your financial reports. Regular maintenance, accurate data entry, and periodic reviews of your financial data will help prevent future issues and keep your business finances in top shape. If you encounter persistent problems or complex issues, seeking professional help from a certified QuickBooks ProAdvisor or accountant is advisable to ensure your financial data is accurate and reliable. Visit us :- https://www.errorsfixs.com/quickbooks-profit-and-loss-report/