Download

1 / 10

100 likes | 399 Views

Valuation of Merger Target. Corporate Financial Decisions Timothy A. Thompson. Basics. Valuation of merger target is from the perspective of acquiring company´s shareholders Net present value of acquisition is the „value of the target to acquirer“ minus the „effective cost“.

E N D

Valuation of Merger Target Corporate Financial Decisions Timothy A. Thompson

Basics • Valuation of merger target is from the perspective of acquiring company´s shareholders • Net present value of acquisition is the „value of the target to acquirer“ minus the „effective cost“

Value of target to acquirer • Value of the target to the acquirer is made up of: • Stand alone value of the target plus • Value of improvements at target made by acquirer management plus • Value of pure synergies between target and acquirer

Valuations must make a capital structure assumption • The valuations (stand alone, improvements, and synergies) must make a capital structure assumption • WACC model or APV model • Be careful! • The capital structure assumption should not be reflective of the financing used to buy the target per se, but should reflect the degree to which owning the target incrementally affects your debt capacity

What?! • For example, suppose you bought the target with debt • If you are using WACC to value target, the weights should reflect the debt capacity of the target, not 100% debt • If you are using APV, the tax shields should only reflect the contribution of the target firm towards affording those tax shields

What is the „effective cost“? • Acquirer pays cash ($100M) • Cash price is the effective cost of the acquisition • Acquirer must raise the cash ($100M) • Assume borrow the money from government with a subsidized rate • Loan is $100M, but PV of loan payments is $95M • „Purchase price“ is $100M, but acquirer makes $5M NPV on loan. „Effective cost“ of acquisition is $95M • Assume sell shares of combined firm ($100M) • „Purchase price“ is $100M, but suppose shares are actually worth $60M. NPV on share sale is $40M. „Effective cost“ of acquisition is „$60M“.

Deal NPV and NPV to original shareholders • Deal NPV is the NPV of the deal to all capital contributors • Original target shareholders • And new purchasers of stock or debt • If new securities are not zero NPV • This is a redistribution among capital providers • Decision should be made from perspective of original target shareholders • Actual NPV = Deal NPV – NPV of financing issues

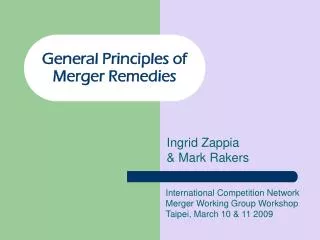

Valuation of Merger Target Deal NPV Value of synergies „Purchase price“ Value of improvements Value of Target to Acquirer Stand alone value of target V

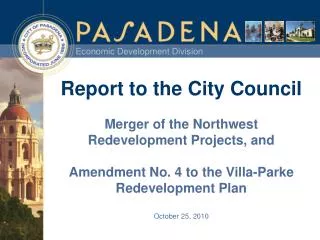

NPV to target shareholders NPV of financing issues NPV to target shareholders Value of synergies Value of Target to Acquirer´s Share- holders „Purchase price“ Value of improvements Stand alone value of target V

Where was „effective cost“? • The „purchase price“ minus the NPV of financing is the „effective cost“ • Real world situations • Debt plus warrants or equity of private firm (like John Case) • Debt may be cheap to „make it up on equity“ • Subsidized loans • Using overvalued stock to make acquisitions