Download

1 / 11

110 likes | 155 Views

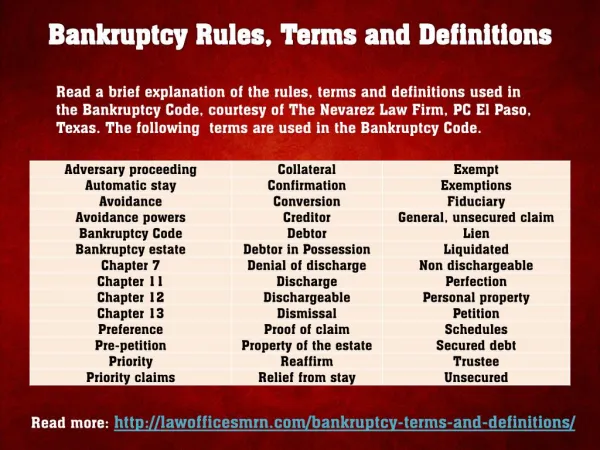

When people start companies, no one sets out with the idea in mind that eventually they’ll go bankrupt. Bankruptcy is often a combination of unforeseen circumstances and a lack of professional advice – one of the main reasons that a company goes bankrupt is because they run out of operating cash to pay their monthly expenses, and stop paying their bills. When you have a reliable and knowledgeable accountant on your team, avoiding bankruptcy becomes a part of your strategic plan from the beginning. Here at Kent Accounting we’ve provided some of the terms that are important for every business owner to know regarding bankruptcy and some starter strategies you can implement to help you avoid it!<br>

E N D

Terms to Understand and Strategies to Help Small Business Avoid Bankruptcy

When people start companies, no one sets out with the idea in mind that eventually they’ll go bankrupt. Bankruptcy is often a combination of unforeseen circumstances and a lack of professional advice – one of the main reasons that a company goes bankrupt is because they run out of operating cash to pay their monthly expenses, and stop paying their bills. When you have a reliable and knowledgeable accountant on your team, avoiding bankruptcy becomes a part of your strategic plan from the beginning. Here at Kent Accounting we’ve provided some of the terms that are important for every business owner to know regarding bankruptcy and some starter strategies you can implement to help you avoid it!

Creditors Formally, bankruptcy is what happens when a business is unable to pay creditors (those parties whom have lent the company money) and those creditors choose to take legal action by suing the company for the money that is owed. Assets When a company goes bankrupt, the first step is to sell off all the assets of the business. This can happen in many ways, but is usually done using a court appointed trustee, who oversees the sales process, and the proceeds are then distributed amongst the creditors by the trustee.

Profit versus Cash The terms “profit” and “cash” are not interchangeable. If a company earns $10,000 in revenue in a month, and has $8,000 in wages and other bills in that month, then they earn a profit of $2,000. However, as we all know, our clients like to pay us after 30 days (or more), but our employees usually want to get paid after one or two weeks. The cash flow for the month will depend on how much money was collected from prior months’ sales in the month and it could turn out that the business may actually lose cash in the month, despite earning a profit.

Kent Greaves, CPA, CA of Kent Accounting, gives us this example to help explain how small businesses can find themselves overwhelmed by their profit versus cash situation: “Take for example getting a big order or project that starts on January 1 and you estimate that order will take a year to complete. Your initial cash outlay (for payroll and materials) would likely be in January with continuing cash outlays each month for additional payroll/materials. If the project completes in December, normal payment in Alberta would be 30 – 90 days, with some larger companies taking as long as 6 months to pay. This puts 18 months from your first cash outlay to receipt of all of the cash related to the project. It is imperative that you map out the cash outlays your project will incur and incorporate progress payments into your negotiations with the prospective client.”

So what goes hand in hand with small businesses taking on larger projects? Running into cash flow problems, which can lead your company directly to bankruptcy. Here are just a few suggestions on how to avoid cash flow problems: Project Size: When you are pitching to larger companies or responding to requests for proposals, ensure that your company is in a position to take on the additional work load. When considering, take into account labour costs, materials, and especially the drain on cash flow. Working closely with your small business accountant on these proposals will ensure you can deliver what you are promising. Unsure about how much more work your small business can handle? Contact Kent Accounting so we can help you accurately understand your capacity.

Cash Flow Forecast: With your accountant, build out a basic Cash Flow Forecast, which is a simple spreadsheet that lays out your estimated incomes and expenses for the year. This will enable you to understand the big picture of your business, and what kind of resources would be required on monthly basis to take on more projects and grow your business. BONUS: Download our Kent Accounting’s basic Cash Flow Forecast excel sheet to get started. Have questions? Don’t hesitate to reach out to our team. Contracts: Set up a contract (a written one!) for every project over a certain dollar amount (e.g. $1,000). There are many contract templates available and your small business accountant can help you tailor those templates to ensure your business is protected from a financial standpoint. Contact Kent Accounting to review your current standard contract template.

Payment Terms: One thing smart small business accountants do is help business owners set up appropriate payment terms. An example of standard terms could be requesting 25% of payment up front, 25% half way through the project, 25% when the project nears completion and 25% upon client acceptance of finished product. Every business is unique and it’s best to consult with a small business accountant to make sure the payment terms you’ve set up are appropriate for your business and industry – contact Kent Accounting today for advice on payment terms.

Credit Policy: Simply put, a credit policy is a defined time-period for payment of goods and services and it is something many small businesses overlook when they are setting up their company. In the early stages of every business, finding a balance between generating new business and ensuring you do work with companies that will pay you promptly is critical. While setting up a Credit Policy isn’t difficult, what can be difficult is enforcing it. There will always be exceptions to your policy, but if you ask and expect your clients to abide by your policy, then you significantly reduce your risk of low cash flow and bankruptcy. To ensure your credit policy is thorough enough to get you paid, contact Kent Accounting.

Connecting with an accountant who specializes in small business is the first step to protecting your business from cash flow problems and bankruptcy. For a review of your current policies, don’t hesitate to connect with Kent Accounting.

Kent Accounting is a full service accounting firm located in Calgary, Alberta. The firm is lead by Kent Greaves, a Chartered Professional 'Accountant in Calgary' with over 18 years of experience working with privately owned companies. Our 'small business accountants in calgary' believe in prompt, accurate service at affordable rates. Running a small business can be the most exciting endeavor and the greatest challenge a person can undertake; we’re here to help you succeed.