Download

1 / 29

320 likes | 776 Views

The Accounting Cycle. After studying this chapter you should be able to: Understand basic accounting terminology. Explain double-entry rules. Identify steps in the accounting cycle. Prepare adjusting entries. Prepare closing entries. Prepare reversing entries. 2. 2. 2. Roadmap.

E N D

The Accounting Cycle After studying this chapter you should be able to: • Understand basic accounting terminology. • Explain double-entry rules. • Identify steps in the accounting cycle. • Prepare adjusting entries. • Prepare closing entries. • Prepare reversing entries. 2 2 2

Roadmap • Basic terminology • Introduction to accounting cycles • Adjusting entries • Prepayments • Prepaid expenses • Unearned revenues • Accruals • Accrued revenues • Accrued expenses • Closing entries • Reversing entries

Basic Terminology • The following is a brief summary of selected terms. • Event: A happening of consequence. May be external or internal. Generally triggers a change in assets, liabilities or equity. • Transaction: An external event involving a transfer or exchange between two or more entities. • Account: A systematic recording of transactions or events that affect assets, liabilities, equity, revenue and expense areas. An account represents an area of similar economic interest. 3 3 3

Basic Terminology • Real Accounts: Balance sheet accounts--Asset, liability and equity accounts (except dividends). Exist from one period to the next (not closed). • Nominal Accounts: Income statement accounts--Revenue and expense as well as the dividends account. They do not exist from one period to the next (they are closed). Exist in name only! 4 4

Basic Terminology • Trial Balance: A list of all open accounts in the GL and their balances. Done to prove the equality of debits and credits. • Unadjusted--taken after routine entries are posted. • Adjusted--taken after adjusting entries are posted. • Post-closing--taken after closing entries are posted. • Adjusting Entries: Done to bring the books up to date in anticipation of the preparation of the financial statements. • Financial Statements: The primary reporting vehicles for accounting information. They are the result of the collection, tabulation and summation of accounting data. The following four statements comprise a complete set of financial statements (“taken as a whole”): 6 6

Basic Terminology • Balance sheet--Financial condition (position) of an enterprise at the end of the period. • Income statement--Shows the results of operations for the period. • Statement of cash flows--Reports cash activity for the period by operating, investing and financing flows. • Statement of retained earnings--Reconciles the beginning and ending balances in the owner equity account. • Closing entries: Done to zero the nominal accounts, formally calculate income or loss and update retained earnings. 7 7

Basic Terminology • Debits and credits: • Debit means entering an amount on the left-hand side of an account. It does not mean increase or decrease. • Credit means entering an amount on the right-hand side of an account. It does not mean increase or decrease. Account Name Debit Credit 8 8

Basic transaction entries Purchase Cash Purchase Dr. Assets (Trucks, Inventory, etc) xxx Cr. Cash xxx Purchase on account Dr. Assets (Trucks, Inventory, etc) xxx Cr. Accounts Payable xxx

Basic transaction entries Sell Cash Sell Dr. Cash xxx Cr. Assets xxx Sell on account Dr. Accounts Receivable xxx Cr. Assets xxx

Basic transaction entries Pay Your Dues Dr. Accounts Payable xxx Cr. Cash xxx Collect Your Dues Dr. Cash xxx Cr. Accounts Receivable xxx Pay Dividends Dr. Retained Earnings xxx Cr. Cash xxx

Basic Terminology • Double Entry System of Accounting. A logical method for recording transactions. It recognizes that there are at least two events or changes for each transaction. Debit (or sum of the debits) will always equal the credit (or the sum of the credits). • Balance Sheet Equation: Assets = Liabilities + Owner Equity Assets will always equal the sources of those assets. That is, assets belong to either the creditors or the owners. 9 9

Summary of Basic Terminology • Events, transactions and accounts • Real accounts and nominal accounts • Financial statements • Debits and credits • Basic equation

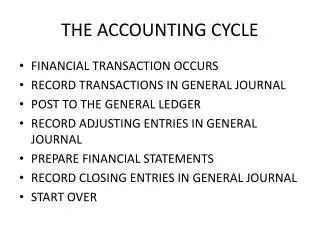

Accounting Cycle • Accounting Cycle: • Identify, analyze and record relevant business transactions. • Both internal and external events. • Journalizing • Record of transactions in the journal in formal journal entry form. Transactions are recorded all in one place in chronological order. 10 10

Accounting Cycle • Formal journal entry form: (If more than one debit and/or more than one credit it is called a compound entry.) • Date Account name XX • Account name XX • Account name XX • Explanation • Posting: Routine function of carrying the entries from the journal to the ledger. • Trial balance: Listing of accounts and their balances in general ledger order (A,L, OE, R, E). Done to prove the equality of the debits and credits. 11 11

Accounting Cycle • Adjusting Journal Entries (AJE): Done to bring the books up to date so financial statements can be prepared. • Types of AJEs: • Deferrals • Accruals 12 12

Accounting Cycle • After all the adjusting entries have been recorded and posted an adjusted trial balance is taken. • This will not detect omissions or errors where debits = credits. It only determines, after adjusting, that total debits = credits. • Financial statements may then be prepared from the adjusted balances. 24

Adjusting Entries • Let’s review examples of selected AJEs: • Deferral of an expense (prepaids) • Deferral of a revenue (unearned revenues) • Accrual of an expense • Accrual of a revenue 13 13

Adjusting Entries • Deferral Type of AJE is characterized by a previous transaction which must be adjusted because it is now the end of the period (time period assumption). The transaction is not yet complete at the end of the period. • Example: Deferral of an expense. Information: You are a tenant renting office space for $2,000 per month. On November 1, 19X1, you prepay six months of rent or $12,000 to your landlord. The original entry may have been: 11/1 Rent expense 12,000 Cash 12,000 14

Adjusting Entries • Suppose it is now December 31, 19X1, two months later. The previous entry must be adjusted. The adjusting entry would be: • To adjust: • 12/31 Prepaid Rent 8,000 • Rent Expense 8,000 Note: You had to refer back to the original entry to prepare the correct adjusting entry. 15

Adjusting Entries • This properly reflects, at the end of the period, four months of asset remaining and two months of expense matched to the period. • But what if the original entry had been: • 11/1 Prepaid Rent 12,000 • Cash 12,000 16

Adjusting Entries • Then the appropriate adjusting entry would be: • To adjust: • 12/31 Rent Expense 4,000 • Prepaid Rent 4,000 Note: You had to refer back to the original entry to prepare the correct adjusting entry. 17

Adjusting Entries • Example: Deferral of an revenue. Information: You are a publisher selling magazines. You collect on 9/1/X1, a total of $18,000 for the next six months of publications (earned evenly). The original entry may have been: • 12/31 Cash 18,000 • Earned Revenue 18,000 • It is now 12/31/X1 and the above entry is no longer wholly correct. It must be adjusted to reflect you have services still to perform. 18

Adjusting Entries To adjust: 12/31 Earned Revenues 6,000 Unearned (Deferred) Revenues 6,000 But what if the original entry had been: • To adjust: • 12/31 Cash 18,000 • Unearned (Deferred) Revenues 18,000 19

Adjusting Entries • It is now 12/31/X1 and the above entry is no longer wholly correct. It must be adjusted to reflect you have services still to perform. The adjusting entry at 12/31/X1 would be: • To adjust: • 12/31 Unearned Revenues 12,000 • Earned Revenues 12,000 • The adjusting entry was prepared with the original entry in mind. You arrive at $12,000 of earned revenue and $6,000 of a liability, deferred revenues, at the end of the period. 20

Adjusting Entries Accrual type of adjusting journal entries: • Done to record an as yet unrecorded transaction. To accrue or record for the first time. • No prior transaction to refer back to or update. • Example: Accrual of a revenue: Information: You have performed accounting services for a client on December 30, 19X1. The services are valued at $300 but you have not recorded this yet nor sent a bill. To adjust: 12/31 Accounts Receivable 300 Service Revenue (Earned) 300 Note: There will always be a pairing between a receivable (balance sheet) and a revenue (income statement) account. 21

Adjusting Entries • Example: Accrual of an expense Information: You had some emergency repair work done on 12/31/X1. The plumber states the bill will be approximately $3,400. To adjust: 12/31 Repair Expense 3,400 Accounts Payable 3,400 Note: There will always be a pairing between an expense (income statement) and a payable (balance sheet) account. The final accrual done will be the tax accrual. 22

Adjusting Entries Cost allocation type of adjusting journal entry: • To follow matching and divide up cost to current and future periods benefited. • Depreciation, bad debt expense. Example: You consume the usefulness of your building at the rate of $12,000 per year. To recognize that the cost has now been consumed (now an expense) you depreciate: 12/31 Depreciation Expense (I/S) 12,000 Accumulated Depreciation (B/S) 12,000 23

Closing Entries • Purposes of Closing Entries • Calculate COGS under Periodic Inventory System: • Establish Ending Inventory • Get rid of Begging Inventory and all Purchases related accounts • COGS is a plug-in number • Reduce the balance of all nominal accounts to zero. • Debit all revenue accounts and credit Income Summary • Credit all expense accounts and debit Income Summary • Close Income Summary to Retained Earnings 25

Reversing Entries • OPTIONAL • Purpose: simplify the recording of transactions in the next accounting period • When: at the beginning of the next accounting period • How: reverse the adjusting entry made in the previous accounting period • Example: P91 • Guidelines are on Page 92-93.