Download

1 / 38

400 likes | 445 Views

Learn the complete accounting cycle process with Mugan-Akman 2005 methodology. Understand adjusting entries, prepare financial statements, and close accounts effectively.

E N D

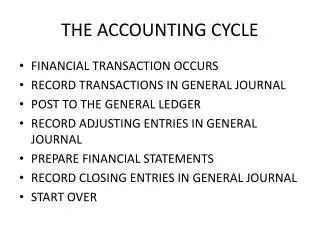

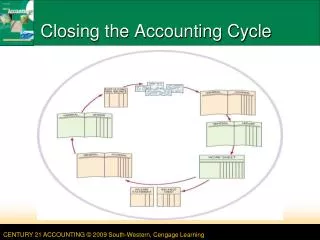

Adjust the accounts and prepare trial balance Analyze and record the transactions Post the transactions and prepare trial balance Prepare the financial statements Close the accounts and prepare trial balance Accounting Cycle Mugan-Akman 2005

Matching Principle All revenues must be recorded in the accounting period in which the goods are sold or services are rendered and all expenses must be recorded in the accounting period in which they are incurred to produce such revenues Mugan-Akman 2005

Adjusting Entries • Some journal entries are made at the end of the accounting period just to separate the effect of an event into its proper periods. • Each adjusting entry affects: 1) a revenue or expense account 2) an asset or liability account (except cash) • Examples include: 1. Recognition of accrued revenues and receivables, 2. Interest calculations, 3. Recognition of accrued expenses and payables, 4. Allocation of prepaid operating costs, and 5. Recognition of depreciation. Mugan-Akman 2005

When do we need adjusting entries? Mugan-Akman 2005

TRIAL BALANCE Mugan-Akman 2005

Adjusting Entries Mugan-Akman 2005

Adjustment (1)Prepaid Rent Mugan-Akman 2005

Adjustment (2)Prepaid Insurance Mugan-Akman 2005

Adjustment (3)Office Supplies Mugan-Akman 2005

Adjustment (4)Depreciation of Property Plant & Equipment Mugan-Akman 2005

Express Travel Agency Partial Balance Sheet 31January 2004 In TL Plant and Equipment Office Equipment and Furniture 15.000 Less: Accumulated Depreciation (250) Plant and Equipment, net 14.750 Mugan-Akman 2005

Adjusting Entries Mugan-Akman 2005

Adjustment (5)Unearned Revenues Mugan-Akman 2005

Adjusting Entries Mugan-Akman 2005

January 2004 Mugan-Akman 2005

Adjustment (6)Accrued Salary Expense Mugan-Akman 2005

Adjustment (7)Accrued Interest Expense Mugan-Akman 2005

Adjusting Entries Mugan-Akman 2005

Adjustment (8)Accrued Revenues Mugan-Akman 2005

Effects of Adjusting Entries Mugan-Akman 2005

Adjust the accounts and prepare trial balance Analyze and record the transactions Post the transactions and prepare trial balance Prepare the financial statements Close the accounts and prepare trial balance Accounting Cycle Mugan-Akman 2005

Steps to Close Accounts • Close temporary accounts with credit balances to income summary • Close temporary accounts with debit balances to income summary • Close income summary • Close dividends or owners’ withdrawals Mugan-Akman 2005

Closing Credit Balances Mugan-Akman 2005

Closing Debit Balances Mugan-Akman 2005

Closing Income Summary Mugan-Akman 2005

Closing Withdrawals Mugan-Akman 2005

Adjust the accounts and prepare trial balance Analyze and record the transactions Post the transactions and prepare trial balance Prepare the financial statements Close the accounts and prepare trial balance Accounting Cycle Mugan-Akman 2005

Closing Credit Balances Mugan-Akman 2005

Closing Debit Balances Mugan-Akman 2005

Closing Income Summary Mugan-Akman 2005