Download

1 / 60

610 likes | 885 Views

THE ACCOUNTING CYCLE. A DAC 501: FINANCIAL ACCOUNTING PRESENTATION. BY HERICK ONDIGO SCHOOL OF BUSINESS, UoN. The Accounting Cycle. For a new business, it begin by setting up ledger accounts. For an established business, begin with account balances carried over from the previous period.

E N D

THE ACCOUNTING CYCLE A DAC 501: FINANCIAL ACCOUNTING PRESENTATION. BY HERICK ONDIGO SCHOOL OF BUSINESS, UoN

The Accounting Cycle • For a new business, it begin by setting up ledger accounts. • For an established business, begin with account balances carried over from the previous period.

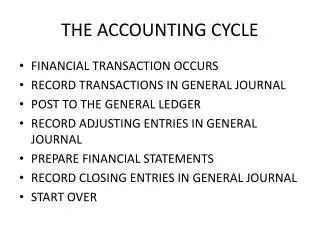

The Steps In The Accounting Cycle • Analyze source documents & record business transactions in a journal • Post journal entries to the ledger accounts • Prepare unadjusted trial balance (TB) • Journalize and post end of period adjustments (EOPA) • Prepare adjusted Trial Balance • Prepare /Create financial statements & reports from data in adjusted TB • Journalize and post the closing entries • Prepare the post-closing trial balance • Prepare and post reversing entries

Prepare unadjusted trial balance. Post entries to the accounts in the ledger. Journalize transactions in the journal. Prepare adjusted trial balance. Journalize and post closing entries Post-closing trial balance Detailed Steps in the Accounting Cycle Analyze Business Transactions. Journalize and post adjusting entries Prepare financial statements.

Analysis and Recording Business Transactions • Business transaction is an economic event that causes a change in the financial position • Financial Position: • What the entity controls • How the entity controls them (claims)

Fundamental Accounting Equation ASSETS = EQUITIES ASSETS = LIABILITIES + OWNERS' EQUITY

Recall the Basic Accounting Equation: Assets = Liabilities + Shareholders’ Equity Implications: Total Asset=Claims against the assets Therefore : If assets increase : either Liabilities and/or Shareholders’ should also increase and vice versa For example: borrow cash, cash (asset) will increase and Liabilities will increase when it is paid back: cash (asset) will decrease and liabilities will decrease How do we use the “Accounting” equation?

How do we record/Account? • An ACCOUNT (ledger Account) : is an accounting device used to record changes in a of a specific asset, liability or owners’ equity item • Has 3 elements: title, debit side and credit side (also called the “T-Account”) • Changes in the accounts are entered manually into a book called a ledger or computerized ledger • Basic forms of book ledgers: the two-column account format, and the running format account • Chart of accounts

Definition of Ledger Account • Ledger Account • Complete listing of business transactions for an individual account • Where you look if you want to find the balance of any given account • General Ledger • A loose-leaf book or computer file containing all the Ledger Accounts • Each account from the chart of accounts has its own ledger account in the general ledger • Complete listing of all account tittles and account names/codes used by an entity is called the chart of accounts - It is like a table of content in a book

Forms of Ledgers Two-Column Account T-Account form that depicts the two-column account:

How do accounts behave? Assets = Liabilities + Shareholders’ Equity + + + So Assets increase on the left hand or debit side then they decrease on the credit side Assets + - debit credit

Behavior of Accounts cont… Liabilities and Owners’ Equity accounts increase on the credit side, decrease on the debit side Liabilities or Owners’ Equity Accounts - + debit credit

Transaction Analysis and The Duality Concept • Double entry system states that every transactions affects at least two accounts. • Therefore • If an asset account increases (decreases), because of duality concept there must be a corresponding: 1.increase(decrease) in a specific liability account 2.or a decrease(increase) in a another asset account 3.or an increase(decrease) in owners' equity account.

What Is a General Journal? • The book in which a person enters the original record of a business transaction • Commonly referred to as a book of original entry • Chronological listing of all the business transactions for the company • Each listing records the debits and credits associated with that business transaction • A book or a location on a hard drive where all business transactions are listed • Like a diary Accounting Is Fun!

What’s in a Journal Entry? • Date • At least one debit entry • Debit account, use exact account title, do not indent titles • At least one credit entry • Credit account, use exact account title, indent titles • An explanation of the transaction: • Check number • Invoice number • Accounts receivable customer name • Many other elements OR details as appropriate… • Remember: the accountant must leave a good audit trail so that users of accounting information can understand what occurred with each transaction DR=CR

Illustration of the accounting process 1. On Jan 1 2010 Ms.Farida invested $100,000 at the inception of the business, Express Travel Agency

2. On 1 January employed a full time secretary and a sales representative.

3. On 1 January rented an office building and paid 3 months rent of $600.

4. On 2 January office furniture and equipment is purchased for $ 15,000 , for which $ 5,000 is paid in cash and the rest would be paid later in January and February 2010.

5. On 3 January insured the office building and the equipment effective from 1 January to 31 December 2010 and paid $ 120 for the whole period.

6. On 5 January the company signed an agreement with Keya Airline to sell their airline tickets and receive commissions in return.

7. On 10 January Express Travel Agency borrowed $15,000 from the bank at an annual interest rate of 24% for six months. The principal and the interest of the loan will be paid together on 10 July 2010.

7. On 10 January Express Travel Agency borrowed $ 15,000 from the bank at an annual interest rate of 24% for six months. The principal and the interest of the loan will be paid together on 10 July 2010.

8. On 10 January purchased office supplies for $2.500 in cash.

8. On 10 January purchased office supplies for $2,500 in cash.

9. During the first half of January the agency sold tickets to various customers and on 16 January issued a commission invoice to clients amounting to $5,000 that will be collected later in January 2010.

9. During the first half of January the agency sold tickets to various customers and on 16 January issued a commission invoice to clients amounting to $ 5,000 that will be collected later in January 2010.

10. On 20 January the company paid $5,000 for the furniture and equipment that were purchased on 2 January.

10. On 20 January the company paid $5.000 for the furniture and equipment that were purchased on 2 January.

11. On 22 January received $7,500 from a customer for organizing the accounting conference that will be held on February 2, 2010.

11. On 22 January the company received $7.500 from a customer for organizing the accounting conference that will be held on 2 February 2010.

12. The company received the full payment of commission charged to Kenya Airlines of $ 5.000 on 23 January.

12. The company received the full payment of commission charged to Kenya Airline s of $ 5,000 on 23 January.

13. On 24 January paid salaries of $ 9,000 employees in cash.

13. On 24 January paid salaries of $ 9,000 employees in cash.

14. During the second half of January the agency sold tickets to various customers and on 31 January issued a commission invoice to Kenya Airline amounting to $ 7,500 which will be collected in February 2010.

14. During the second half of January the agency sold tickets to various customers and on 31 Jan sent an invoice to Kenya Airline amounting to $7,500 which will be collected in February 2010

15. Ms. Farida ( the proprietor) withdrew $ 3,000 on 31 January for her personal use.

15. Ms. Farida withdrew $ 3.000 on 31 January for personal use.

Summary of Journalizing Steps: • Determine the effects of transactions on three components of the accounting equation, • Determine which specific accounts are affected, and • Assure that total of the increases should be equal to either increases on the other side of the equation or to decreases on the same side, or a combination there of.

Behavior of Accounts- Summary Assets = Liabilities + Owners’ Equity + - - + - + Dr Cr Dr Cr Dr Cr Expense Revenue + - - + Dr Cr Dr Cr Withdrawals/Dividends + - Dr Cr

Adjust the accounts and prepare trial balance Analyze and record the transactions Post the transactions and prepare trial balance Prepare the financial statements Close the accounts and prepare trial balance Accounting Cycle-Revisited

Posting -Defined • The process of transferring figures from the journal to the ledger accounts • It simply involves transferring data from one accounting entry into another • The purpose is to classify and summarize transactions and events affecting specific elements of the financial statements

Four-Step Posting Process • Transfer transaction date to account’s date column • Transfer the debit/credit amount and calculate the new balance • Write journal page number in posting reference column of ledger as a cross-reference • Go back to journal and write account number in posting reference column of journal as a cross-reference • Cross-reference • The ledger account number in the Post. Ref. column of the journal and the journal page number in the Post. Ref. column of the ledger account

Exercise • Post all the above transactions (journal entries) to the following ledger accounts: • Prepaid Rent, Office supplies, Prepaid insurance, Office Furniture & Equipment, Bank loan, Accounts Payable, Unearned Revenue, Capital, Withdrawals, Commission Revenue, & Salary Expense • Cast the ledger accounts • Determine the balances carried down (Bal c/d) and balances brought down (b/d) • Prepare a summary of the ledger balances in a two columnar listing to derive the Trial Balance( TB)

Preparing a Trial Balance • List the ledger account balances in two columns on the trial balance • Left column = Debits • Right column = Credits • Trial balance proves DR = CR

The Balancing of Accounts, The Trial Balance & Financial statements • Introduction: • In the previous exercise , you have learned the principles of double entry and how to post to the ledger accounts. The next step in our progress towards the financial statements is the trial balance. • Before transferring the relevant balances at the year end to the financial statements, it is usual to test the accuracy of the double entry bookkeeping records by preparing a trial balance. This is done by taking all the balances on every account. Due to the nature of double entry, the total of the debit balances will be exactly equal to the total of the credit balances.