Download

1 / 20

200 likes | 781 Views

2 Step Process: eligibility application. Eligibility: project must meet federal guidelines for rehab and qualifying expensesApplication: actual deduction awards must be applied for and are granted by a local CRD Authority, but declared

E N D

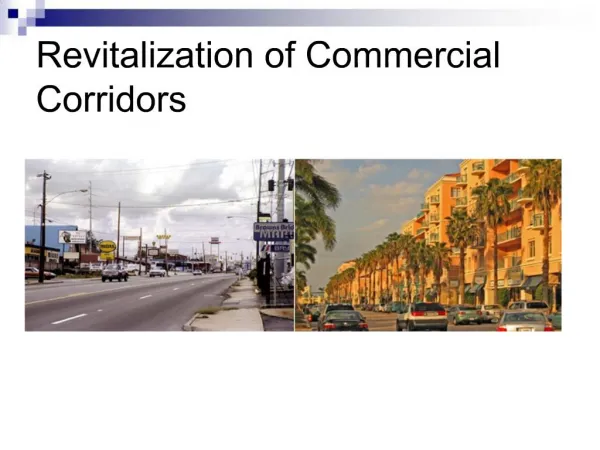

1. Commercial Revitalization Deduction Incentive to Purchase or Substantially Rehabilitate Nonresidential Real Property in the Renewal Community

2. 2 Step Process: eligibility + application Eligibility: project must meet federal guidelines for rehab and qualifying expenses

Application: actual deduction awards must be applied for and are granted by a local CRD Authority, but declared & affect federal taxes

3. RC Advantages: Up Close

4. Local Application- 4 Priorities for Awards Primary Focus: New Jobs

Emphasis on allocation of deductions will focus on building projects which will help support new job creation

Strong Wages

Jobs to be located at the site support higher than average wages by comparison

Abandoned, Refurb Buildings

Project Readiness

Bonus Points for other extraordinary economic development considerations

5. RC & Chattanooga

6. How to Apply? Consult with your tax professional to make sure your project satisfies federal eligibility tests (info following)

�CRD� Application forms available from:

On line: www.renewal-community.com

Pick up from:

Mayor�s Office, City Hall, Lindsay Street

Chamber of Commerce

River City Company

African American Chamber

Call City�s RC Hotline and have Mailed to You: 757 - 4903

7. When Can You Apply? Application forms for 2002 are being accepted NOW! $12M to Award in 2 Months.

Projects that meet fed eligibility and are good candidates for satisfying local criteria can apply during the following stages of development:

Prior to Construction- but able to be completed in 24 months

Mid Construction- but able to be completed in 24 months

Post Construction- but no later than the year the building is placed into service

8. Commercial Revitalization Deduction- federal eligibility Rehabilitation of the abandoned or under utilized buildings in a renewal community

New construction

Not applicable for:

Residential rental projects

Building acquisitions without substantial rehabilitation

Land speculation

For-profit businesses with insufficient income to take advantage of accelerated depreciation deductions or non-profits

9. Mixed Use Buildings Residential rental property is a building for which at least 80% of gross rental income is rental income from dwelling units

If less than 80% of gross rental income is from dwelling units, then the building would qualify for the Commercial Revitalization Deduction

10. What Is the Deduction? An option to treat the capital expenses for the qualified revitalization of a qualified building by either:

Deducting half (50%) of the qualified expenses for the tax year the building is placed in service, or

Amortizing all the qualified expenses over a 120 month period beginning with the month the building is placed in service (or 10% per year for 10 years)

Normally, deductions would be taken over 39.5 years.

11. What Is a Qualified Revitalization Building? A building and its structural components you place in service in the renewal community before 2010

If the building is new, the original use must begin with you

If the building is not new, you must substantially rehabilitate the building then place it in service

12. What is Substantial Rehabilitation? The total qualified rehabilitation expenditures during any 24-month period* beginning after 2001 must exceed the greater of

100% of the adjusted basis of the building and its structural components at the beginning of the 24 month period, or

$5,000

* 60 months if completed in phases set forth in an architectural plan

13. What Is a Qualified Revitalization Expense? Depreciable costs of a new building

Depreciable costs associated with an existing building that has been substantially rehabilitated

1245 property is

1.Tangible or intangible personal property

2.Other tangible property (except buildings and components) used for manufacturing, production, or extraction or of furnishing transportation, communications electricity, gas, water, or sewage disposal services.

a) A research facility in any of the above activities.

b) A facility in any of the activities above for the bulk storage of fungible commodities.

3. That part of real property (not part of 2) with an adjusted basis that was reduced by certain amortization deductions

Such as: certified pollution control facilities

child care facilities

removal of architectural barriers to persons with disabilities and the elderly

reforestation expenses

Or: a section 179 deduction

Single purpose agricultural or horticultural structure.

Storage facilities (except buildings and their structural components) used in distributing petroleum or any primary product of petroleum

Section 1245 property does not include buildings and structural components. DO NOT treat structures that are essentially items of machinery or equipment as buildings and structural components.

Structures such as oil and gas storage tanks, grain storage bins, silos, fractionating towers, blast furnaces, basic oxygen furnaces, coke ovens, brick kilns, and coal tipples are not treated as buildings.

Bulk storage facility means the storage of a commodity in a large mass before it is used. Ex. A facility used to store oranges that have been sorted and boxed is not used for bulk storage.

To be fungible, a commodity must be such that one part may be used in place of another.

Stored materials that vary in composition, size and weight are not fungible. One part cannot be used in place of another part and the materials cannot be estimated and replaced by simple reference to weight, measure, and number. Example: the storage of different grades and forms of aluminum scrap is not storage of fungible commodities.1245 property is

1.Tangible or intangible personal property

2.Other tangible property (except buildings and components) used for manufacturing, production, or extraction or of furnishing transportation, communications electricity, gas, water, or sewage disposal services.

a) A research facility in any of the above activities.

b) A facility in any of the activities above for the bulk storage of fungible commodities.

3. That part of real property (not part of 2) with an adjusted basis that was reduced by certain amortization deductions

Such as: certified pollution control facilities

child care facilities

removal of architectural barriers to persons with disabilities and the elderly

reforestation expenses

Or: a section 179 deduction

Single purpose agricultural or horticultural structure.

Storage facilities (except buildings and their structural components) used in distributing petroleum or any primary product of petroleum

Section 1245 property does not include buildings and structural components. DO NOT treat structures that are essentially items of machinery or equipment as buildings and structural components.

Structures such as oil and gas storage tanks, grain storage bins, silos, fractionating towers, blast furnaces, basic oxygen furnaces, coke ovens, brick kilns, and coal tipples are not treated as buildings.

Bulk storage facility means the storage of a commodity in a large mass before it is used. Ex. A facility used to store oranges that have been sorted and boxed is not used for bulk storage.

To be fungible, a commodity must be such that one part may be used in place of another.

Stored materials that vary in composition, size and weight are not fungible. One part cannot be used in place of another part and the materials cannot be estimated and replaced by simple reference to weight, measure, and number. Example: the storage of different grades and forms of aluminum scrap is not storage of fungible commodities.

14. What Is Not Qualified Revitalization Expense? The cost of acquiring a building that you substantially rehabilitate, to the extent that it is more than 30% of the total qualified revitalization expenses for the building (not counting the cost of the building itself)

Any expenditure which is used in computing any allowable credit

15. Dollar Limitation Qualified revitalization expense is limited to the smaller of:

$10 million, or

The amount allocated to the building by the Chattanooga CRD Authority

16. Example 1 Purchased a new building for $2,000,000 with land value of $200,000

Take a deduction of $900,000 (50% of $1,800,000) in the year placed in service, or

Take $15,000 ($1,800,000 � 120) per month amortization for 120 months beginning with the month placed in service

17. Example 2 Purchased an old building for $2,000,000 with $200,000 land value and spent $900,000 on revitalization

This building does not qualify because the revitalization expense is less than the adjusted basis of the cost of the building

18. Example 3 Purchased an old building for $2,000,000 with land value of $200,000 and spent $3,000,000 on revitalization

Deduct $1,950,000 [50% of $3,000,000 + 900,000 (30% of $3,000,000)] in the year placed in service, or

Deduct $32,500 ($3,900,000 � 120) per month amortization for 120 months beginning with the month placed in service

19. What Is the Effect of Commercial Revitalization Deduction? The adjusted basis of the building is reduced by the amount of the commercial revitalization deduction

The balance of the basis is depreciated using the current depreciation rules

20. How Do I Claim the Deduction? If the 50% deduction is claimed � claim under �other deductions� on the appropriate income tax return

If amortized over 120 months, the deduction is claimed on Form 4562

21. Need More Information? IRS Publication 954

IRC �1400I

1-800-829-1040

www.irs.gov