Download

1 / 19

200 likes | 355 Views

Completion of the Accounting Cycle for a Merchandise Company. Chapter 13. Preparing financial reports for a merchandise company. Learning Objective 1. Learning Unit 13-1. Banks are interested in the revenue producing areas of a merchandising company. Expenses are linked to

E N D

Completion of theAccounting Cycle for aMerchandise Company Chapter 13

Preparing financial reports for a merchandise company. Learning Objective 1

Learning Unit 13-1 Banks are interested in the revenue producing areas of a merchandising company. Expenses are linked to products for a full view of success.

Learning Unit 13-1Income Statement Net Sales Cost of Goods Sold – Gross Profit Operating Expenses = – Net Income from Operations Other Income = + Other Expenses Net Income – =

Learning Unit 13-1 Example Art’s Wholesale Clothing Company Statement of Owner’s Equity For Year ended December 31, 200x Art’s, Capital, January 1, 200x $ 7,905 Net Income for the Year $13,745 Less Withdrawals for the Year 8,600 Increase in Capital 5,145 Art’s, Capital, December 31, 200x $13,050

Learning Unit 13-1 Example Art’s Wholesale Clothing Company Classified Balance Sheet December 31, 200X AssetsLiabilities Current Assets: Current Liabilities: Cash $10,920 Accounts Payable $17,900 Accounts Receivable 14,500 Salary Payable 3,070 Inventory 2,300 Tax Payable 1,500 Total Current Assets $27,720 Total Liabilities $22,470 Plant Assets Owner’s Equity Equipment $15,500 Capital $13,050 Less Accum. Dep. 7,700 7,800 Total Liabilities and Total Assets $35,520 Owner’s Equity $35,520

Recording adjusting and closing entries. Learning Objective 2

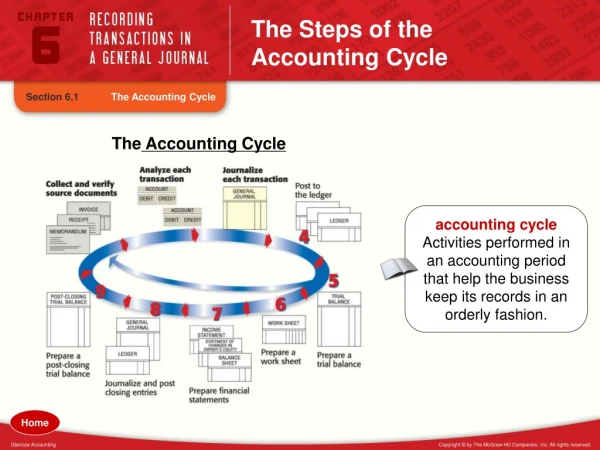

Learning Unit 13-2 • Adjusting entries shown on the worksheet are journalized. • Adjusting entries are then posted to the proper accounts.

Learning Unit 13-2 • All Discount plus Returns and Allowances accounts are temporary accounts that have to be closed. • The account Freight-In is also a temporary account that needs to be closed.

Learning Unit 13-2 Close all balances on the income statement credit column of the work-sheet except Income Summary. Close all balances on the income statement debit column of the work-sheet except Income Summary.

Learning Unit 13-2 Transfer the balance of the Income Summary account to the Capital account. Transfer the balance of the Withdrawal account to the Capital account.

Preparing a post- closing trial balance. Learning Objective 3

Learning Unit 13-3 Example Art’s Wholesale Clothing Company Post-Closing Trial Balance December 31, 200X Cash $10,920 Accounts Receivable 14,500 Inventory 2,300 Equipment 15,500 Total $43,220

Learning Unit 13-3 Example Art’s Wholesale Clothing Company Post-Closing Trial Balance December 31, 200X Accumulated Depreciation $ 7,700 Accounts Payable 17,900 Salary Payable 3,070 Tax Payable 1,500 Owner’s Capital 13,050 Total $43,220

Completing reversing entries. Learning Objective 4

Reversing Entries Example Date Account and Explanation. Debit Credit Dec. 31 Salaries Expense 600 Salaries Payable 600 Adjusting entry

Reversing Entries Example Date Account and Explanation. Debit Credit Jan. 1 Salaries Payable 600 Salaries Expense 600 Reversing entry

Reversing Entries Example Date Account and Explanation. Debit Credit Jan. 1 Salaries Expense 2,000 Cash 2,000 Paid salaries