Download

1 / 16

160 likes | 385 Views

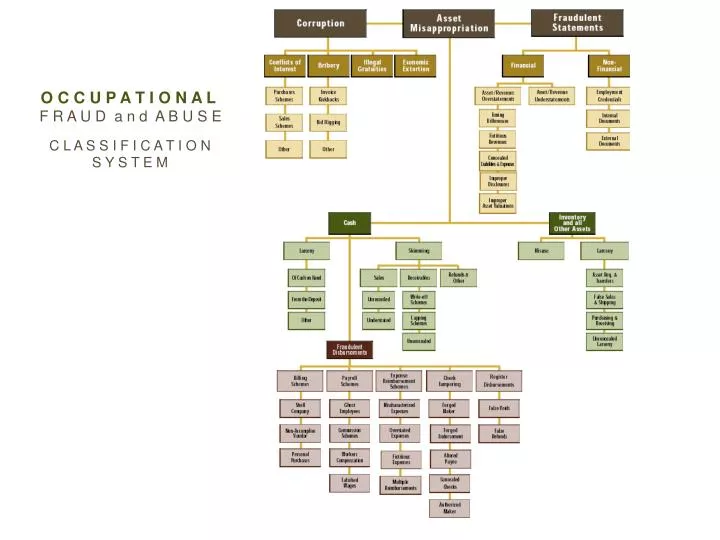

O C C U P A T I O N A L F R A U D a n d A B U S E. C L A S S I F I C A T I O N S Y S T E M. Finally, most fraudulent disbursements fall into one of the above five categories. 5 Types of Check Tampering. Forged Maker Authorized Maker Altered Payee Forged Endorsement Concealed Check.

E N D

O C C U P A T I O N A L F R A U D a n d A B U S E C L A S S I F I C A T I O N S Y S T E M

Finally, most fraudulent disbursements fall into one of the above five categories.

5 Types of Check Tampering • Forged Maker • Authorized Maker • Altered Payee • Forged Endorsement • Concealed Check

Keys to Forged Maker Scheme: • obtain the check • determine who to make it payable to • forge the signature • convert the check • conceal your crime (record the check in the books, or?)

Keys to Authorized Maker Schemes: • Probably already has access to check stock • No need to forge signature • Still needs to convert the check • Still a problem with concealment

Concealment Methods: • Alter the bank statement • Re-alter checks after bank statement • Enter false info. into CDJ • Code checks to false debits • Re-issue checks to vendors expecting payment

Audit Program Steps for CH5: • See pages 195-196 – these red flags should be added to our audit programs (if not already there) • Controls on 196-199 are controls that the client should have. We should inquire of these during our internal control work.

In other words, to determine if a significant risk of fraud exists, we should: • identify the type of fraud that could occur and, • evaluate the risk factors that relate to that fraud type, grouped by: • pressure or incentive • opportunity • rationalization

To carry this a step further, SAS #99 identifies 4 facets to the risk of MM due to fraud: • type • significance ($ magnitude) • likelihood (that it will be material) • pervasiveness