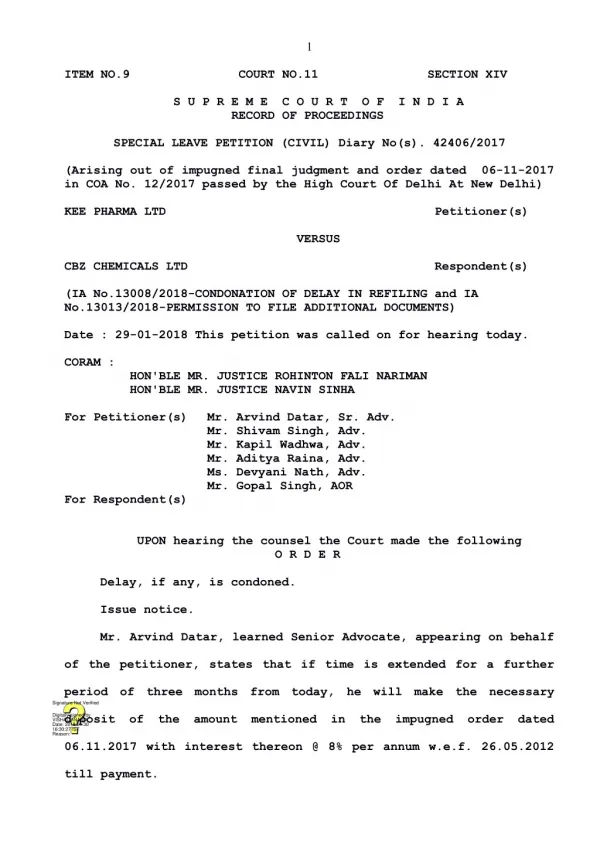

Download

1 / 14

140 likes | 393 Views

CBZ Bank Limited Presentation. Presentation by D. Z. Mandivenga SMEs & Microfinance Executive at The AFRACA Southern Africa Sub Regional Workshop. INTRODUCTION. Who is CBZ Bank Limited Structures – Divisions Number of Branches Vision and mission - Our commitment

E N D

CBZ Bank Limited Presentation Presentation by D. Z. Mandivenga SMEs & Microfinance Executive at The AFRACA Southern Africa Sub Regional Workshop

INTRODUCTION • Who is CBZ Bank Limited • Structures – Divisions • Number of Branches • Vision and mission - Our commitment - Our principles - Our driving force

OUR COMMITMENT To be a progressive strong bank geared to serve personal and corporate customers globally from our home base. To satisfy the diverse needs of our customers by offering a wide range of innovative financial services solutions.

OUR PRINCIPLES • Governance Conscious-Dedicated to being ethical, compliant and transparent in all our activities. • Customer Focus-Dedicated to satisfying customers' needs by being responsive, professional, efficient and reliable. • Innovative Approach-Dedicated to being creative in the development and provision of financial solutions. • Staff Focus-Dedicated to staff empowerment and motivation to foster a culture of productivity and commitment. • Social Responsibility-Dedicated to being a responsible and good corporate citizen.

OUR DRIVING FORCE To be the preferred bank where excellence is a virtue. This will be achieved through innovative service delivery, competency and flexibility whilst adhering to principles of integrity, transparency and fairness.

Why small holder farming sector still remains grossly under- funded, the Commercial Banks’ perspective • Lack of tangible collateral • Fragmented nature of sector • Yields of crops are normally below economic thresholds • Funding the small holder not cost effective • Lack of profitable markets • Cost of money

How did CBZ Bank address the needs of the sector? • Opened a new unit for Community Banking to cater for micro and small clients. • Employed specialised staff to dedicate their time to this special group • Accepted household assets ,group guarantees and personal guarantees as substitutes to the usual preferred tangible 1st class security. • Sourced technical support from CARE and grant assistance from DFID • Due to the high transaction costs associated with lending to micro and small client we employed the following: - Charged interest rates that covered admin costs, loan losses and cost of funds - Maintained levels of Delinquency at very low levels through use of effective group lending methodology - Linkages helped us to reach remote rural areas

How did CBZ face these challenges?. continued • We took a holistic approach to serve this sector (All financial services) • Worked with other PVOs operating in Rural areas by going into partnerships • Worked with other big institutions whose core businesses is Agricultural Production ( Out growers Scheme) • Grouped small communal farmers for purposes of marketing large quantities of produce.

Successful Partnerships in Our rural expansion thrust • Initiative for the Development and Equity in African Agriculture (IDEAA)-provision of in calf heifers to small holder farmers • Farmers Association of Chiefs/Headman Investment Groups (FACHIG)-provision of agricultural inputs to communal farmers • Southern Alliance for Indigenous Resources (SAFIRE)-sustainable use of natural resources

What does CBZ have in store? • Agricultural Thrust mainly expansion in rural areas / Resettlement areas • Value chain concept • Partnership /Linkages to be increased • Networking

Recommendations for Improving Service Delivery To Rural Clients • Other banks must take a leaf from our experiences, for we cannot reach all the deserving clients. • Government must seriously consider the issue of incentivising those offering their services in the rural areas so that more players can come in. • The concept of value chaining financing must be promoted. • Use of mobile banks must be encouraged in order to reach remote areas.

Conclusion Our country’s economy is Agrobased and for it to reach its desired objectives Financial institutions especially Commercial Banks must play a key role and CBZ has led by example in our country. Special mention must go to our Central Bank which is supporting Agriculture through a number of initiatives such as:

Conclusion….continued • The Mechanisation Programme • Cheaper sources of funds • Technical Assistance I am very optimistic that with such kind of innovations (Thinking outside the box) the country and the region can confidently say we will achieve the set MDGs