Download

1 / 9

90 likes | 1.82k Views

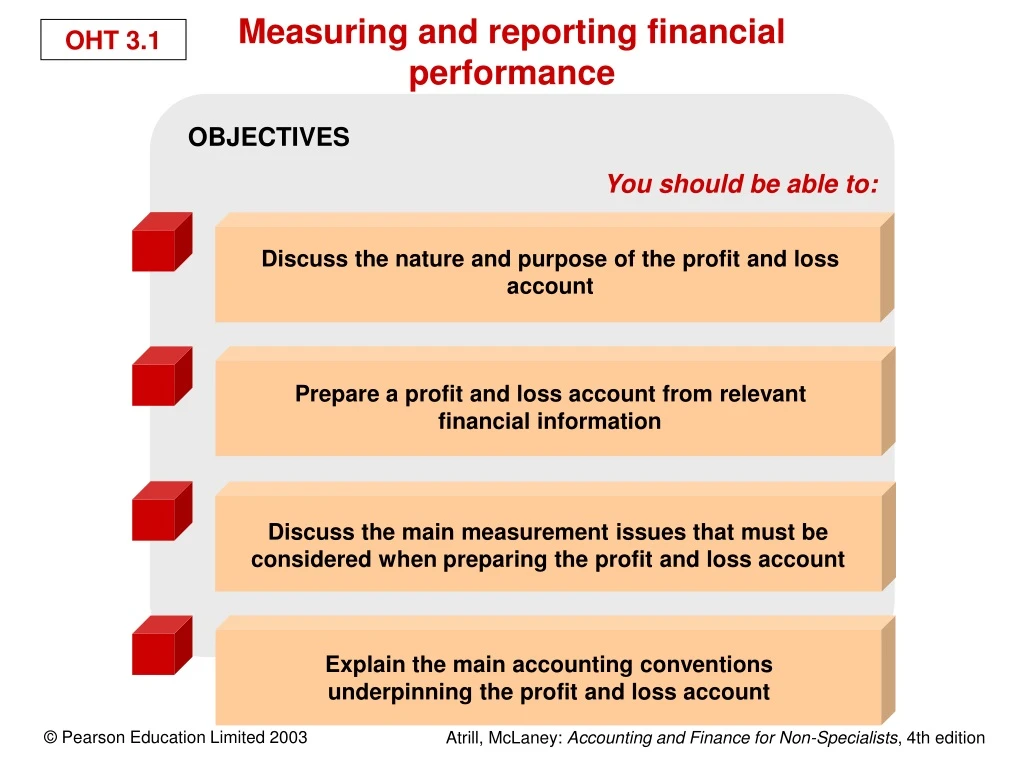

OBJECTIVES. You should be able to:. Discuss the nature and purpose of the profit and loss account. Prepare a profit and loss account from relevant financial information. Discuss the main measurement issues that must be considered when preparing the profit and loss account.

E N D

OBJECTIVES You should be able to: Discuss the nature and purpose of the profit and loss account Prepare a profit and loss account from relevant financial information Discuss the main measurement issues that must be considered when preparing the profit and loss account Explain the main accounting conventions underpinning the profit and loss account Measuring and reporting financial performance

The realisation convention states that revenue should be recognised only when it has been realised. Normally, realisation is considered to have occurred when: The activities necessary to generate the revenue are substantially complete The amount of revenue generated can be objectively determined There is reasonable certainty that the amounts owing from the activities will be received Profit measurement and the recognition of revenue

Profit and loss account Sales commission expense £6,000 Balance sheet at year end Cash flow statement Cash £5,000 Accrual £1,000 Accounting for sales commission

Balance sheet at year end Cash flow statement Cash £20,000 Accounting for rent payable Profit and loss account Rent payable expense £16,000 Prepaid expense £4,000

To calculate a depreciation charge for a period, four factors have to be considered: The cost of the asset The useful life of the asset The residual value of the asset The depreciation method Profit measurement and the calculation of depreciation

40 30 Written-down value (£000) 20 10 2 3 4 1 0 Asset life (years) Graph of written-down value against time using the straight-line method

40 Written-down value (£000) 30 20 10 2 3 4 1 0 Asset life (years) Graph of written-down value against time using the reducing-balance method

Cost less Residual value equals Depreciable amount Year 4and so on Year 1 Year 2 Year 3 Depreciation Depreciation Depreciation Depreciation Asset life (number of years) Calculating an annual depreciation charge

Common assumptions used are: First in, first out (FIFO) Last in, first out (LIFO) Weighted average cost (AVCO) Profit measurement and stock costing methods