Download

1 / 29

300 likes | 436 Views

Red Meat Prospects Conference. ‘Progress Through Partnership’. Market Outlook for Beef & Sheep Sectors: - ROI Perspective. Joe Burke. March 2013. Beef Market Outlook. Irish Cattle Availability EU Beef Production Price Situation Market Demand Live Exports. ROI National Cattle Herd 2012.

E N D

Red Meat Prospects Conference ‘Progress Through Partnership’

Market Outlook forBeef & Sheep Sectors:- ROI Perspective Joe Burke March 2013

Beef Market Outlook • Irish Cattle Availability • EU Beef Production • Price Situation • Market Demand • Live Exports

ROI National Cattle Herd 2012 Source CSO June 1.14m. Dairy cows 1.15m. Suckler cows produced 2.16m. calves in 2012: Source DAFM Dairy-beef crosses 0.38m Dairy-bred animals 0.75m. Suckler-bred cattle 1.03m.

2012 Calf Registrations +3.7% / +77,000 Live Exports -25% / -55,000

Throughput Forecast – Export Meat Plants (000’ head) Most of this increase likely in second half of 2013

ROI weekly finished cattle supplies (head) 2013 Cattle Supplies to-date 9.7% vs. 2012

European Markets Cattle Supplies 2012 UK • Throughput -6.3% • Prime cattle -7.6% • Cull cows -1.6% • Calf births recover • Germany • Throughput -1.5% • France • Throughput -5.7% • Y. Bulls -6.5% • Cull cows -4.8% • Live Exps: -3.1% EU Beef Production in 2012 4.8% lower than 2011 • Italy • Throughput -4% • Cattle imports -10% • Males aged <12mo.s -8% (EU Commission) • Spain • Throughput -1.5% • Live imports -17% • Live exports +54%

EU-27 Beef Production Trend 2011 - 2013 -1.7% -2.1% -1.5% +0.5% N/C. +8% +1% -2% Source: EU working beef forecasting group Further decline of 0.5% forecast for 2013

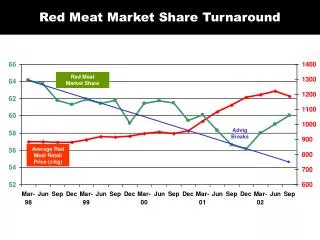

Producer Price Increase: ROI vs. Europe & UK Note: Price Increase in Euro terms

Producer Prices: Ireland vs. Europe & UK Prices in Euro terms (w/e 09/03) Irish Price €4.08/kg, EU-15 Av. €3.95/kg; UK €4.37/kg In Italy, R-grade young bull price: €4.09/kg, Spain: €3.90, France: €3.94, Germany €4.14

Slight further decline in consumption forecast -1.2% -0.6% Source: EU working beef forecasting group

Ireland Beef Consumption • 52 Weeks to 17th February: • Volume: -6.9% • Av. Price: +8.0% to €8.85/kg • Latest 4 weeks to 17th Feb: • Volume -7.3% • Av. Price: +13.4% to €9.36/kg Source: Kantar

UK Beef Consumption • 52 Weeks to 17 February • Volume: - 2.8% • Price: + 7.3% • 4 Weeks to 17 February • Volume: -1.1% • Price: +3.0% Knock-on effect of price increases Less price promotions Underlying decline in consumption Disappointing sales of roasting joints Sales of burgers/grills down 35% in latest 4 week period

Live Cattle Exports 2013 Distribution of Live Exports from Ireland up to w/e. 2nd March

Beef Summary • Recovery in national cattle herd: • Increase in cattle kill on last year’s low levels • Continued decline in EU production: • 4.8% fall in 2012; even tighter supplies this yr • Market opportunities in France, Germany, Italy and Netherlands • Price performance: UK & Irish producer prices have risen most • Beef consumption impacted by higher prices, especially in the more ‘difficult’ economies: ROI, Italy, Spain, Portugal • Some recovery in live exports, especially calves

Wk ending 30 Dec ROI Sheep Meat Production 2011 v’s 2012 TOTAL 2,171,242 + 160k + 32K + 68k TOTAL 2,431,283 Source: DAFM +12% Increase | +260k head | +5,300 tonnes to53,300t

ROI Sheep Population Outlook 2013 ... 2-3% growth 6.4 Number of Sheep (Millions) 5.25 5.15 4.7 3.5 2.67 Source’: CSO June National Livestock Survey

ROI Sheep Throughput Year to-date 2011, ‘12, ‘13 TOTAL 300,652 TOTAL 335,259 + 90k TOTAL 447,201 +33% Increase | +112k head | 19.9kg Av Carcass Wt | +2,229 tonnes

ROI Sheep Prices Period: 2010- 2013 2012 462c

Home Market – Consumption still growing Latest Kantar Retail Data (52 week period ending 17 Feb ‘13) Total Volume 9,760t (+ 4.9)% Total Value €103m (+ 4.3%)

Promoting Lamb with the Quality Mark 2013 Spring & Summer Lamb Promotion PR activity Instore Activity New Season Lamb Radio Advert TV Advertising (8wks) & Local Radio

Export Market Performance Period: January – December 2012 SWEDEN 2,424t (+17%) UK 11,318t (+4%) Netherlands 1,365t (+76%) BELGIUM 2,129t (+35%) Export Market Volumes up 12% Value up 7% GERMANY 2,508t (+29%) FRANCE 18,995t Hong Kong 680t (+6%) (+350%) Source’: Bord Bia estimates based on CSO/GTIS

Irish Sheep Meat Exports* ... Continued shift from carcass to boneless trade *Exports to FR, UK, BE, S, DE

Markets Carry over of hoggets | Production +8% | 55% exports FR | Sterling Production - 8% | poor domestic demand | targeting France Breeding flock -5% | Lacaune lambs Spring ’13 | Import requirement + Production + 3-5% | Shipping costs | Weather | Market Priorities?

Market Outlook forBeef & Sheep Sectors:- ROI Perspective Joe Burke March 2013

Red Meat Prospects Conference ‘Progress Through Partnership’