Download

1 / 14

140 likes | 297 Views

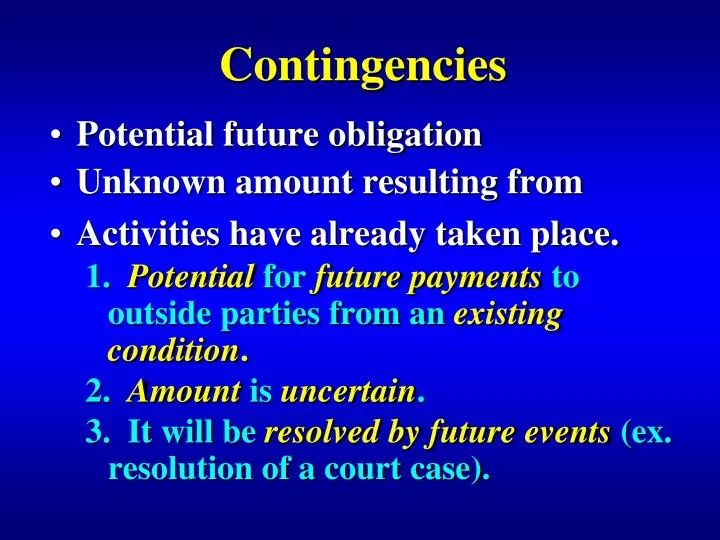

Contingencies Potential future obligation Unknown amount resulting from Activities have already taken place. 1. Potential for future payments to outside parties from an existing condition . 2. Amount is uncertain .

E N D

Contingencies • Potential future obligation • Unknown amount resulting from • Activities have already taken place. • 1. Potential for future payments to outside parties from an existing condition. • 2. Amount is uncertain. • 3. It will be resolved by future events (ex. resolution of a court case).

Loss Contingency Treatment • Likelihood of Event Treatment • Remote (Slight chance) No disclosure • Reasonably possible • (more than remote, less Disclose • than probable) • Reasonably est. • Probable- adjust • Cannot estimate • -disclose

Sources of Information • 1. Audit workpapers • 2. Inquiries of management • 3. Minutes • 4. Review of legal expense • 5. Attorney confirmations • primary purpose of attorney confirmation is corroboratemanagement information

24-22(a) (from text, not in notes) • The audit step most likely to reveal contingent liabilities is: • 1. Review of vouchers paid in the • month following year-end. • 2. Accounts payable confirmations. • 3. Inquiry directed to legal counsel. • 4. Mortgage-note confirmation.

Subsequent Events and Subsequent Discovery of Fact • Subsequent events -events occurring between the balance sheet date and report date with a material impact on F/S • Subsequent discovery - events discovered after report issued necessitating recall of financial statements • event prior to report date • knowable by auditor

Report • B/S Date Date • Subsequent Subsequent • Event Period Discovery Period • (active search) (passive search)

Report Report mailed • B/S Date Date(discovery • requires recall) • Subsequent Subsequent • Event Period Discovery Period • (active search) (passive search)

Subsequent Events • Direct Effect adjust • Condition existed at B/S date • Meets SFAS # 5 criteria • Indirect Effect disclose • After B/S date, or • Original condition before B/S date • but doesn’t meet SFAS # 5 criteria

24-24 (a) • Subsequent events are defined as events that occur subsequent to: • 1. Balance sheet date • 2. Date of the auditor’s report • 3. Balance sheet date but before the • auditor’s report • 4. Date of the auditor’s report and • concern contingencies not reflected • in the financial statements.

Dual Dated Reports • Applies when testing of an individual subsequent event is performed after field work date • Limits responsibility after report date to subsequent event

Example of Dual Date • Dewey, Cheatem & Howe • February 2, 2009 • except for Note 11, dated February 10, 2009

Subsequent Discovery of Facts • F/S are misleading due to errors or omitted disclosures • Condition existed and was knowableat report date • Not responsible for incorrect estimates, or subsequent changes in facts

Overall Evaluation of Results • Recall that materiality of errors is in relation to F/S as a whole • Individual errors must be summed; compared with materiality (see Figure 24-6 on p. 775) • Includes actual (known) and projected (likely) errors • If exceeds materiality • Adjust for sufficient amount • Increase testing to lower estimated error

Audit Letters (see p. 165 in notes) • Engagement letter • Attorney letter • Client representation letter • Illegal Acts (not responsible for on exam) • Significant Deficiencies • Audit Committee • Management Letter • Will see multiple choice or brief problem/matching on letters