Download

1 / 29

290 likes | 809 Views

. The accounting for purchased goodwill generates greater interest whenever merger and acquisition activity is robust... . And the recent FASB decision to disallow pooling of interests means that goodwill will potentially be an issue in all merger transactions.. . How would you define goodwill? Consider the definition you would use to operationalize goodwill, and compare it to the conceptual definition of goodwill....

E N D

1. Is Goodwill an Asset? Do we care about goodwill, and whether it is an asset?

When is goodwill likely to be an issue that generates interest?

3. And the recent FASB decision to disallow pooling of interests means that goodwill will potentially be an issue in all merger transactions.

4. How would you define goodwill? Consider the definition you would use to operationalize goodwill, and compare it to the conceptual definition of goodwill...

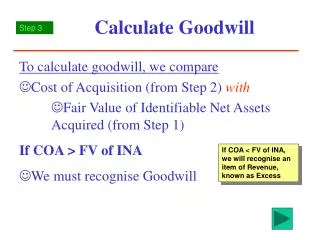

5. The working definition of goodwill has the difference between the purchase price and the fair market value of the identifiable net assets in a purchase transaction. In the past, we accounted for this as an intangible asset and amortized it over a period not to exceed 40 years. Is this adequate anymore? What is the conceptual definition?

6. Conceptually, goodwill is the ability of a business to earn a higher than average rate of return on the identifiable net assets of the company. The higher return implies additional, unidentified, assets that are the drivers for that return.

7. The conceptual definition and working definition are not identical, and they imply some differences in how components of the purchase price might be identified and accounted for. It is useful to evaluate the potential reasons for a difference between the purchase price and the fair market value of the assets.

8. If we can break the lump sum down into component parts, we can evaluate potential accounting treatments that would be implied by the conceptual framework.

9. Nature of Goodwill I�m using the term �goodwill� here in a broad sense, not necessarily consistent with how we account for goodwill...

Top-down perspective: Goodwill is a component or subset of something larger

Bottom-up perspective: Goodwill is the sum of the components that comprise it.

10. Top-Down Goodwill may be viewed as a component of the acquirer�s investment and is based on the acquirer�s expectation about future earnings from the investment.

The issue is framed in terms of whether the investment itself qualifies as an asset. If it does, then the components are viewed as subsets of the larger asset and accounted for as assets themselves.

11. Goodwill is the �leftover� portion of the investment, which is consistent with the definition in APB 16, �the excess of the cost of the acquired company over the sum of the amount assigned to identifiable assets acquired less liabilities assumed.�

12. And this is traditionally how we have thought about goodwill and accounted for it.

13. But as the FASB considers the potential definitions and accounting treatment of �goodwill�, they found that breaking it into different components may also be useful.

14. Bottom-up If the price paid by the acquirer exceeds the fair value of the net identifiable assets of the acquiree, presumably some other resources were acquired that have value to the acquirer. In identifying the resources that may be components of goodwill, it is useful to interpret goodwill broadly to capture the largest potential set of component parts.

15. This may not be consistent with how we finally define goodwill or how we account for goodwill.

16. In its broadest conceptualization, goodwill may be interpreted as the excess of purchase price over book value.

This might be particularly useful if the fair market value of the identifiable assets is hard to determine.

17. What components can you identify that might explain why the purchase price of a company is higher than the book value of the net assets? (Hint...the authors of a recent article on goodwill identified 6 potential components.)

18. The following represent possible component parts of goodwill

Excess of the fair values over the book values of recognized net assets

(Is this part of part of goodwill under APB 16? Should it be? Or should we account for it as something else?)

19. Fair values of other net assets not recognized by acquiree - primarily identifiable intangibles that may not have been recognized, possibly because they did not meet recognition criteria (IPR&D)

(Is this part of goodwill under APB 16? Should it be? Or should we account for it as something else?)

20. Fair value of the going concern element of the acquiree�s existing business; the ability of the acquiree as a stand alone business to earn a higher rate of return on an organized collection of net assets than would have been expected if those assets had been acquired separately (Synergies)

21. Fair value of synergies from combining the acquirer�s and acquiree�s businesses and net assets. This is unique to each business combination.

22. Overvaluation of the consideration paid by the acquirer - possible errors in valuing the purchase consideration (i.e., in an all-stock transaction, the current market price of the shares issued may be higher than if those shares were sold for cash and the cash was then used to effect the combination). (Is this conceptually goodwill? Is the price of shares �fixed�?

23. Overpayment or underpayment by the acquirer, which may occur when the price is driven up in the course of bidding for the acquiree, or when the net assets were obtained through a distress or fire sale (Tyco�s problem when they sold their CIT Insurance group....maybe�)

24. Components 1 and 2 both relate to the acquiree and how the acquiree values its assets.

25. These are not conceptually part of goodwill. Component 1 is not an asset in and of itself, but instead reflects gains that were not recognized by the acquiree on its net assets and is therefore part of those assets, not goodwill.

26. Component 2 is also not part of goodwill, at least not conceptually, but instead primarily reflects intangibles that might be separately identified and recognized as individual assets rather than being included in �goodwill�

27. Components 5 and 6 relate to the acquirer but are not conceptually part of goodwill. Component 5 is not an asset or even part of an asset, but rather a measurement error.

Component 6 represents a gain or loss resulting from measurement error and is not conceptually goodwill.

28. Only Components 3 and 4 are conceptually part of goodwill, and may be thought of as �core� goodwill.

Component 3 might be thought of as �preexisting goodwill� that was either internally generated by the acquiree or acquired by it in previous business combination. This might be called �going concern� goodwill.

29. Component 4 did not exist before the combination, but rather results from the combination itself, and may be referred to as combination goodwill.

30. What are the conceptual differences between going concern goodwill and combination goodwill?

31. Example Big Bank, and institution experienced in acquiring other banks and successfully consolidating their operations with their own, acquires Local Bank, an institution with many of its branch banks located across the street from Big Bank branches.

32. Big Bank acquired Local Bank primarily because of the synergies from consolidation that ultimately are expected to be reflected in significant cost savings from Big Bank�s plan to close redundant branch banks (some will be Big Bank branches; some will be Local Bank branches)

33. If Local Bank�s identifiable net assets have a fair value of $10 million and Local Bank has a market value of $14 on a stand-alone basis, it�s going concern goodwill might be $4 million. If Big Bank acquires it for $20 million, it might be assumed that combination goodwill has a value of $6 million.

34. Based on this analysis of the six components of purchase price, the question of what goodwill is--and is not--can be answered, at least conceptually...

Goodwill is really components 3 and 4

But measurement issues make it difficult to separate out components 1, 2, 5, and 6

35. Conceptually, how should we account for components 1, 2, 5, and 6?

36. 1--add to asset values to write up to FMV

2--establish asset values

5-6 measurment errors--what do you suggest, if the amounts could be determined? If the amounts cannot be determined?

37. Core Goodwill CON 6 states that assets are probable future economic benefits obtained or controlled by a particular entity as a result of past transaction or events. Assets have 3 essential characteristics:

38. Assets embody a probable future benefit that involves a capacity, singly or in combination with other assets, to contribute directly or indirectly to future net cash inflows

39. A particular entity can obtain the benefit and control others� access to it, and

40. The transaction or other event giving rise to the entity�s right to or control of the benefit has already occurred.

41. Core goodwill cannot be exchanged for something else of value nor can it be used to settle the entity�s liabilities. However, it can be used to produce net future cash inflows.

42. Core goodwill has the capacity in combination with other assets to contribute indirectly to future cash flows. The future benefit associated with core goodwill may be less certain than the benefit associated with other most other assets

43. CON 6 notes that the �most obvious evidence of future economic benefit is market price�.

44. Because core goodwill does not have the capacity singly to contribute directly to future net cash inflows, it is not priced separately in the marketplace, but rather is priced in combination with other assets with which it contributes to future cash flows

45. While core goodwill is not priced separately, that does not preclude it from having future economic benefit. CON 6 notes that anything commonly bought and sold has future economic benefit, including the items in a �basket purchase� obtained in a business combination (para. 173)

46. Control exists, because the acquirer owns a controlling financial interest in the acquired entity�s equity.

And the past transaction is the acquisition.

47. So it would seem that core goodwill meets the criteria to be recognized as an asset.

48. Separately Identifiable Schuetze would exclude goodwill from his definition of assets because he would require that all assets that are not cash or contractual claims to cash or services must be capable of being sold separately for cash. AS a result, exchangeability is an essential characteristic of those assets.

49. UK�s Accounting Standards Board in 1997 also took the stand that Goodwill is not an asset. While their definition of an asset is similar to that of the FASB, they interpret �control� in a different context. The ASB states �items that cannot be separately identified from the business as a whole cannot be individually controlled by the entity and hence are not assets.�

50. The ASB states that �goodwill is neither an asset like other assets nor an immediate loss in value. Rather, it forms the bridge between the cost of the investment as shown in the acquirer�s own financial statements and the values attributed to the acquired assets and liabilities in the consolidated financial statements.

51. Although purchased goodwill is not in itself an asset, its inclusion amongst the assets of the reporting entity, rather than as a deduction from shareholders� equity, recognized that goodwill is part of a larger asset, the investment, for which management remains accountable.�

52. Meeting the definition of an asset is a necessary but not sufficient condition for goodwill to be recognized as an asset in the financial statements. Measurabilty, relevance, and reliability must also be met.

53. One question is the extent to which we can measure the different components of the excess of purchase price over the book value of the assets.

54. IT seems that different portions of the components should be accounted for differently.

55. The net gains on the appreciation of the assets above book value should be included in the asset value and depreciated.

56. Core goodwill should be capitalized. Should it be depreciated? Subject to impairment tests? Maintained indefinitely?

57. The new standard on business combinations indicates that core goodwill should be capitalized and subject to an impairment test. What do you think of this?

58. Intangibles Component 2 was:

Fair values of other net assets not recognized by acquiree - primarily identifiable intangibles that may not have been recognized, possibly because they did not meet recognition criteria (IPR&D)

59. Research on Intangibles The Financial Accounting Standards Committee of the American Accounting Association is charged with responding to requests by standard setters on issues related to financial reporting.

60. They find that extant research supports the following conclusions:

Expenditures on R&D and to a lesser extent advertising, not currently recognized as assets, contribute to firm value That is, capital market research ascribes asset-like status to such expenditures.

61. That means that market prices reflect a time component to these expenditures.

62. This, in spite of the fact that the assets are not reflected on the balance sheet�how do we determine that the market treats these expenditures as assets?

63. The stock market reacts positively to firm�s announcements relating to R&D activities. Higher than expected R&D expenditures are positively correlated with higher stock prices. Similarly, the stock market values advertising expenditures. The effects of advertising were largely confined to firms producing durable goods.

64. That would indicate that the market perceives a higher present value of future cash flows because of these current expenditures.

65. By evaluating the length of time the stock sells at a �premium� related to the announcement of the expenditure, we can infer the life that the market attributes to the expenditure.

66. Inferred lives of advertising expenditures were generally short, in the range of 1-5 years.

The inferred lives of the R&D investments ranged from 5 to 10 years,

67. In special cases, such as in the wireless communication industry, nonrecognition of internally generated intangibles can potentially obviate the relevance of conventional financial statements.

68. What does this imply for the fair value of acquired intangibles?

Can the values be measures reliably?

69. One might believe that management made estimates of the values of identifiable intangibles in arriving at a purchase price for the acquisition...

70. So the assets could be valued �through the eyes of management�.

Is this a fair market value? OR does it contain measurement error?

71. IF it contains measurement error, is this a problem?

72. Is your answer different if you are considering the use of financial information to evaluate the stewardship of management vs. the forward looking estimate of the nature, timing, and uncertainty of future cash flows?

73. Is it better to attempt to measure these different components of goodwill and treat them separately or to lump them all together in a single intangible asset account, goodwill?

74. IPR&D Interpretation 4 of FAS 2 states that IPR&D must be measured and separated out from core goodwill in a purchase combination.

What is IPR&D?

75. The research and development acquired singly, as a part of a group of assets, or in a business combination accounted for using the purchase method.

76. Example Three grad students in Ames, Iowa, started a biotech research company. They rented office space in the ISU Research Park. They bought 3 state-of-the-art computers and programs worth $15,000, and 3 used desks and chairs. The grad students spent three years developing computer models of DNA molecules in an attempt to develop a

77. model of an insect-resistant corn seed. After 3 years, they had a design for genetically-engineered corn that they believed would be worth testing.

They did not have the resources to actually make the seed nor to test it in fields.

78. Because they did not have the resources to carry the development work any farther, they decided to look for a buyer for their company.

79. Does their work and their company have value? To what extent? What is the value of their net identifiable tangible assets?

Do they have any goodwill? (Remember our definition(s) of goodwill)

What will the purchase price represent?

80. The entire value of the company is IPR&D.

According to current accounting standards, the entire amount of IPR&D must be expensed when acquired.

81. This requirement is to maintain consistency with FAS 2, which requires all R&D to be expensed as incurred.

Does this make sense?

If IPR&D were not expensed, what would be the issues with capitalization?

Costs to complete, similar research projects that were internally generated...

82. The SEC has taken issue with IPR&D charges, claiming that they have been abused.

What about the potential for abuse?

Are large charges likely?

What are the measurement issues?

83. Who makes the determination of the value of IPR&D?

84. One of the problems has been who has the expertise to value the different components of IPR&D. On occasion, the audit firm has evaluated the deal and assigned values to the components of the excess of the purchase price over the book value of the assets.

85. What are the issues with this?

86. What is the potential impact on reported earnings? (See IPR&D paper�)

87. Does this raise questions about the relevance and reliability of financial reporting?

89. FASB Paper...