Download

1 / 53

530 likes | 636 Views

ACCOUNT SIDE RULES. ACCOUNTS INCREASE ON THE SIDE IN WHICH THEY APPEAR IN THE ACCOUNTING EQUATION ASSETS = LIABILITIES + CAPITAL LEFT = RIGHT ASSETS INCREASE LEFT SIDE OF THE ACCOUNT LIABILITIES/CAPITAL INCREASE RIGHT SIDE OF THE ACCOUNT. ACCOUNT SIDE RULES. +. ASSETS. =.

E N D

ACCOUNT SIDE RULES • ACCOUNTS INCREASE ON THE SIDE IN WHICH THEY APPEAR IN THE ACCOUNTING EQUATION • ASSETS = LIABILITIES + CAPITAL • LEFT = RIGHT • ASSETS INCREASE LEFT SIDE OF THE ACCOUNT • LIABILITIES/CAPITAL INCREASE RIGHT SIDE OF THE ACCOUNT

ACCOUNT SIDE RULES + ASSETS = LIABILITIES CAPITAL LEFT RIGHT = + - + - - + INC DEC DEC INC DEC INC

A BASIC T ACCOUNT HAS TITLE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT

ASSETS INCREASE ON THE LEFT SIDE OF THE ACCOUNT DECREASE ON THE RIGHT SIDE SIDE OF THE ACCOUNT

LIABILITES DECREASE ON THE LEFT SIDE OF THE ACCOUNT INCREASE ON THE RIGHT SIDE SIDE OF THE ACCOUNT

CAPITAL DECREASE ON THE LEFT SIDE OF THE ACCOUNT INCREASE ON THE RIGHT SIDE SIDE OF THE ACCOUNT

RECORDING TRANSACTIONS DIRECTLY INTO THE ACCOUNTS • The following reflects how we would record the same transactions we have been working with directly into the accounts • I have broken the major classifications (assets, liabilities, and capital) down into the specific accounts we must create as a result of these transactions

Transaction 1 CASH LEFT SIDE ACCOUNT 100,000 RIGHT SIDE ACCOUNT

Transaction 1 CAPITAL LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 100,000

Transaction 2 CASH LEFT SIDE ACCOUNT 100,000 200,000 RIGHT SIDE ACCOUNT

Transaction 2 NOTES PAYABLE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 200,000

Transaction 3 LAND LEFT SIDE ACCOUNT 25,000 RIGHT SIDE ACCOUNT

Transaction 3 CASH LEFT SIDE ACCOUNT 100,000 200,000 RIGHT SIDE ACCOUNT 5,000

Transaction 3 NOTES PAYABLE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 200,000 20,000

Transaction 4 EXPENSE LEFT SIDE ACCOUNT 500 RIGHT SIDE ACCOUNT

Transaction 4 CASH LEFT SIDE ACCOUNT 100,000 200,000 RIGHT SIDE ACCOUNT 5,000 500

Transaction 5 CASH LEFT SIDE ACCOUNT 100,000 200,000 700 RIGHT SIDE ACCOUNT 5,000 500

Transaction 5 REVENUE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 700

Transaction 6 DRAWING LEFT SIDE ACCOUNT 100 RIGHT SIDE ACCOUNT

Transaction 6 CASH LEFT SIDE ACCOUNT 100,000 200,000 700 RIGHT SIDE ACCOUNT 5,000 500 100

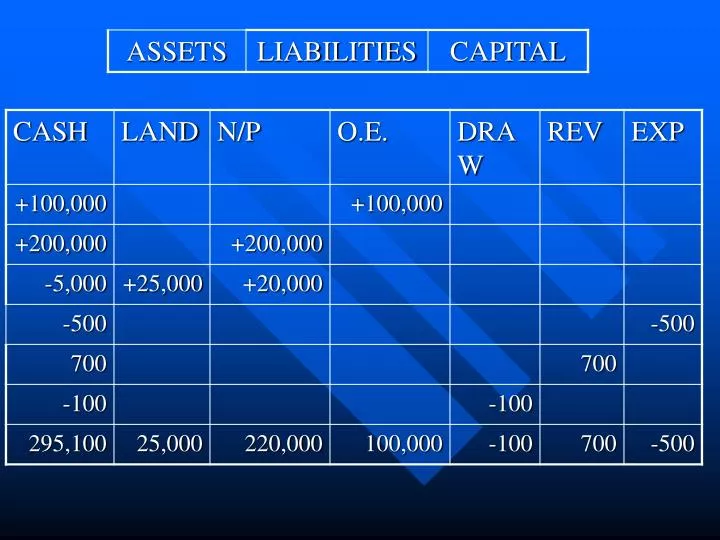

T ACCOUNT FORMAT • Ok, cool, we have recorded those same transactions directly into the accounts using the account side rules given in the second slide. • Now, we need to do the math to determine the “amount” or “resulting balance” that we report for each of the accounts. • We “foot” the account (which means we add up all the amounts on the left and right side of the accounts). • We then determine the “balance of the account” (since one side represents increases and the other decreases, we subtract opposite sides and report the balance on the side that was the largest.

CASH LEFT SIDE ACCOUNT 100,000 200,000 700 RIGHT SIDE ACCOUNT 5,000 500 100 5,600 300,700 This is a footing This is the balance of the account 295,100

LAND LEFT SIDE ACCOUNT 25,000 RIGHT SIDE ACCOUNT 25,000 25,000

NOTES PAYABLE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 200,000 20,000 220,000 220,000

CAPITAL LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 100,000 100,000 100,000

DRAWING LEFT SIDE ACCOUNT 100 RIGHT SIDE ACCOUNT 100 100

REVENUE LEFT SIDE ACCOUNT RIGHT SIDE ACCOUNT 700 700 700

EXPENSE LEFT SIDE ACCOUNT 500 RIGHT SIDE ACCOUNT 500 500

BEFORE WE GO ANY FURTHER • THE LEFT HAND SIDE OF THE ACCOUNT IS CALLED THE DEBITSIDE OF THE ACCOUNT • THE RIGHT HAND SIDE OF THE ACCOUNT IS CALLED THE CREDITSIDE OF THE ACCOUNT • WHY? • WHY NOT?

MEANINGS? • DOES DEBIT MEAN GOOD/BAD? • NO • DOES CREDIT MEAN INCREASE/DECREASE? • NO • DEBIT MEANS LEFT SIDE AND CREDIT MEANS RIGHT SIDE AND NOTHING ELSE

IF YOU REALLY WANT A LITTLE MORE INFO • Debit is short for debtor (DR) – loosely translated from Latin “to have” • Credit is short for creditor (CR) – loosely translated from Latin “to owe” • When this method was created in the 1400’s, the inventors personified the accounts and viewed them as people, and since the assets and equities have opposing positions, they use the opposite sides of the accounts to record the transactions • The cool thing about this approach is that it has a built-in mechanism to “double-check” our mechanics (ie, debits must equal credits)

IS THIS THE PERFECT FORMAT? (RECORDING DIRECTLY INTO THE ACCOUNTS) • WHAT WAS THE $5,000 CASH PAID OUT FOR? • YOU KNOW BECAUSE THIS IS A SHORT PROBLEM WE HAVE WORKED REPEATEDLY • WHAT IF WE HAD 100,000 CASH TRANSACTIONS AND I ASKED YOU ON 12/31 WHY DID WE PAY OUT $14,000 ON MARCH 25 – HOW WOULD YOU ANSWER THE QUESTION? • THE ONLY WAY IS TO SEARCH FOR A CORRESPONDING DEBIT OF $14,000 ON THAT DATE (AND YOU MAY NOT FIND ONE BECAUSE MAYBE WE BOUGHT AN ASSET FOR 30,000 PAYING DOWN 14, 000 AND PUTTING 16,000 ON A NOTE)

ADJUST FORMAT • ONE MORE THING TO ADD – AND WE WILL BE THERE • PRIOR TO RECORDING TRANSACTIONS INTO ACCOUNT – WE FIRST RECORD IT IN THE JOURNAL • JOURNAL – BOOK (MEDIUM) IN WHICH ALL TRANSACTIONS ARE FIRST RECORDED

JOURNALMECHANICS OF RECORDING ENTRY ORIGINALLY IN THE JOURNAL AS OPPOSED TO THE LEDGER OK, what is this and what does it mean? Its just a different format (the paper looks differenct – no T account), the rules are the same. 1. We record the date. 2. We want to debit cash (remember debit means left side so, we write the account title next to the left side of the column); and we want to credit owners equity (we indent the account title to the right side (credit) of the column). We write the amounts under the appropriate Columns (debit or credit).

EXERCISE • RECORD ALL THE TRANSACTIONS IN THIS JOURNEY ENTRY FORMAT Cash 100,000 Owners Equity 100,000

OK, LETS REVIEW STEPS IN THE ACCOUNTING CYCLE • TRANSACTION • RECORD IN THE JOURNAL BY MEANS OF A JOURNAL ENTRY • POST FROM THE JOURNAL TO THE LEDGER • THE FOLLOWING SHOWS THE DETAILS OF STEPS 2 AND 3.

1 1 Recording and Posting an Entry General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 100,000 Capital 100,000 General Ledger Account: CashAccount No. 11 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 Enterthe transaction date in the ledger account.

2 2 Recording and Posting an Entry General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 100,000 Capital 100,000 GeneralLedger Account: CashAccount No. 11 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 100,000 Enter the debit amount in the ledger debit column.

3 3 Recording and Posting an Entry General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 100,000 Capital 100,000 GeneralLedger Account: CashAccount No. 11 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 100,000 100,000 Update the ledger account balance.

4 Recording and Posting an Entry General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 100,000 Capital 100,000 4 GeneralLedger Account: CashAccount No. 11 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 1 100,000 100,000 Enter the journal page in the ledger account.

5 5 Recording and Posting an Entry General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 11 100,000 Capital 100,000 GeneralLedger Account: CashAccount No. 11 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 1 100,000 100,000 Enter the ledger account number in the journal.

General Journal Page 1 Post. Date Description Ref. Debit Credit 1/1 Cash 100,000 Capital 31 100,000 2 1 5 4 GeneralLedger Account: CapitalAccount No. 31 Post. Balance Date Item Ref. Debit Credit Debit Credit 1/1 1 100,000 100,000 3 Recording and Posting an Entry All five parts of the credit posting are shown.

FUNCTION OF JOUNAL • CRONOLOGICAL ORDER • TO SEE THE ENTIRE TRANSACTION ALL AT ONE TIME • TO IDENTIFY CAUSE/EFFECT • EX. Q. WHY DID WE CREDIT CASH $1MM ON JUNE 29? • EX. A. LOOK IN THE JOURNAL – DOWN PYMT ON TRACTOR.

POST FROM THE JOURNAL TO THE LEDGER • POST • COPY VERBATIM • LEDGER • BOOK (MEDIUM) THAT CONTAINS ALL THE ACCOUNTS OF THE BUSINESS

FUNCTION OF THE LEDGER • SUMMARIZATION • DEPICTS THE FINAL ENDING BALANCE OFALL THE FINANCIAL ITEMS (ACCOUNTS) WE ARE KEEPING TRACK OF • ACCOUNT TOTALS

NEXT STEP - PREPARE A TRIAL BALANCE • LIST OF ALL THE ACCOUNTS IN THE LEDGER AND THEIR BALANCE • PROVES THE EQUALITY OF DEBIT AND CREDITS • PREPARE A TRAIL BALANCE ON A SHEET OF PAPER BASED UPON THE JOURNAL ENTRIES AND LEDGER YOU HAVE PREPARED. DON’T PEEK AT THE NEXT PAGE UNTIL YOU’RE FINISHED – IT HAS THE ANSWER.

ADJUSTMENT PROCESS • REVIEW ALL THE ACCOUNTS IN THE LEDGER • DO THESE ACCOUNTS AND ONLY THESE ACCOUNTS PROPERLY REPORT ALL THE FINANCIAL ITEMS WE WANT? • DO THEY REPORT THE PROPER BALANCE? • IF NO – WE NEED TO CHANGE THEM SO THEY DO – UPDATE THE ACCOUNTS – MAKE ADUSTMENTS

ADJUSTMENTS NECESSARY? • RARE – NO, BUT IN THIS CASE, NO ADJUSTMENTS ARE MADE