Download

1 / 38

380 likes | 494 Views

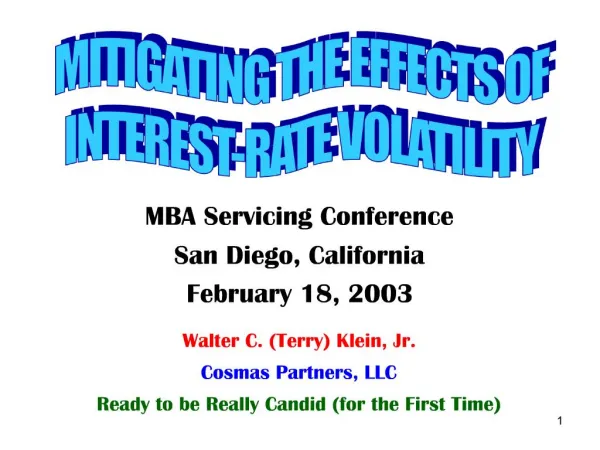

MITIGATING THE EFFECTS OF INTEREST-RATE VOLATILITY. MBA Servicing Conference San Diego, California February 18, 2003. Walter C. (Terry) Klein, Jr. Cosmas Partners, LLC Ready to be Really Candid (for the First Time). Monthly Average Interest Rates 30 Year FNMA Conventional MBS. 17.96%

E N D

MITIGATING THE EFFECTS OF INTEREST-RATE VOLATILITY MBA Servicing Conference San Diego, California February 18, 2003 Walter C. (Terry) Klein, Jr. Cosmas Partners, LLC Ready to be Really Candid (for the First Time)

Monthly Average Interest Rates30 Year FNMA Conventional MBS 17.96% 09/81 14.34% 06/84 10.91% 03/89 12.87% 12/83 9.17% 12/94 8.32% 03/00 8.21% 06/96 9.41% 12/86 6.50% 10/93 1957 12/31 5.60% 6.29% 10/98 6.83% 03/01 1968 4.63% 06/03

ARM Monthly Interest Rates30 Year Fixed-Rate Mortgages The Last Decade Plus In Additional Detail: Patterns of Mortgage Borrowing by Type ARMtoFRM End of Refi BOOM Three ? FRM to FRM Endof Refi BOOM One End of Refi BOOM Two 12/31 5.60%

Mortgage Interest Rates and OriginationsInverted FNMA Rate and$ Billions Sources: FNMA / Inside Mortgage Finance

Inverted FNMA 30 Year Mortgage Rate versus MBA Mortgage Refinance Index 2000 2001 2002 2003 MBA Index Record High 9,978 06/04 MBA Index Previous Record High 6,927 10/09 12/31 5.60% 11/14High 5,535 12/31 1,644 12/22 High 794 12/31 Low 1,644 7 Weeks below 1,500 29 Weeks above 2,500 22 Weeks above 4,000 15 Weeks below 2,500 38 Weeks above 2,500 32 Weeks above 4,000 05/26 Low 288 12 Weeks above 2,500 8 Weeks above 4,000

Industry Volume TrendsMBA Data Dollars in Billions 1 2 3 1Q 410B 4 5 7 6 1 8 11 9 12 10 2 3 13 6 10 4 8 8 11 9 5 7 13 12 2 1 3 7 6 12 9 4 5 10 13 8 11 Forecast

Production versus Runoff DollarsTotal Boarded Portfolio 2001 / 2002 2001 Actual 2002 Actual / Forecast Current Month Estimate in Billions Budget Actual Net Production Payoffs Amortization Foreclosure Actual

What Happened?How Did We Get Here? M. Domingo @ WaMu • Borrowers receive a free prepayment option; • Lenders are required to finance closing costs; • There is no viable market for this “premium”; • Scale / technology have driven unit costs lower; • Result: Lenders hold more servicing rights / risks to fund “premium” – although accounting rules require recognition of income, the lender is really cash poor and is holding Interest-Only (I/O) risk that should be left to sophisticated investors.

The Borrower’s “Free Call Option” M. Domingo @ WaMu • A huge proliferation of “no-cost” mortgage loans • GSE reluctance to support prepayment penalties due to consumer and predatory lending concerns • The clear result is that many Mortgage Brokers and Loan Officers help borrowers to exploit our mortgage finance system with repeated refinances

Servicing is an Operating Business – Not a Derivative Investment M. Domingo @ WaMu • The current base servicing fee may be too high! • Revenue has increased exponentially due to: • The dramatic rise in mortgage loan size; and • Unit Costs are lower due to scale / technology: • Servicing costs and expenses are unit based. • Result: The margin between revenue / expense has created larger absolute MSR values, which, in turn, has greatly expanded the role of servicers in, and the importance of, managing this real I/O risk.

Rethink Prepayment Penalties and Advancing Closing Costs M. Domingo @ WaMu • Structure the “fairest deal” that is not punitive: • Strike a balance by charging an appropriate prepayment fee commensurate with risks of advancing origination costs while offering consumers meaningfully lower rates; or • Advance closing costs as part of principal without triggering marginal LTV thresholds • DO NOT enforce penalty for foreclosure / sale • Educate US borrowers, regulators and investors

Consider Reducingthe Base Servicing Fee M. Domingo @ WaMu • Align servicing fees with the actual cost of the operational infrastructure needed to support it • Strike a balance between risk / reward and market requirements - the lender’s “skin in the game” • Recent Secondary Market changes in this area: • GNMA II Servicing Fee Limit reduced from 44.0 bps to 19.0 bps and MANY are using it • Fannie Hybrid Servicing Fee Limit = 12.5 bps • Freddie Hybrid Servicing Fee Limit = 10.0 bps

Trading MBS in 1/8’s(or at least 1/4’s) M. Domingo @ WaMu • Mortgage originators tend to generally price their mortgage loans to consumers in 1/8 increments • An MBS market that traded in 1/4’s or 1/8’s would allow originators to sell their “excess” servicing enabling them to book reasonable cash gains • Ultimately move the market toward decimalization • Issue: the perceived (significant) liquidity risk • Industry can / should work to create this reality

Mortgage Servicing Fees and MSR’sIssues with Which We Must Deal - I • Marito is correct: our industry must change several key elements of the mortgage banking industry’s core concepts / philosophies if we desire more consistent / predictable earnings • In turn, most of the problems that he mentioned were created by all of us

Mortgage Servicing Fees and MSR’sIssues with Which We Must Deal - II • Increasing volatility in interest rates since the late 1960’s and the growth in mortgage volume since the advent of securitization in 1970 (Ginnie Mae) and its further enhancement in the early 1980’s (FannieMae and Freddie Mac) are more to blame for the true magnitude of these issues / problems • We and the FASB have some responsibility for worsening matters by moving revenue recognition from the servicing annuity to the closing table

Mortgage Servicing Fees and MSR’sIssues with Which We Must Deal - III • The increased volatility of interest rates since the advent of Ginnie Mae securities in 1970 suggests the need for smaller coupon increments and/or wider coupon bands for the Ginnie Mae I MBS’s • After chairing the Ginnie Mae Choice and New Markets Task Forces (2000-2002), it will take a great deal of work to reach agreement since Wall Street Dealers are focused on homogeneity and we are unwilling to forsake our “best” execution

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - I • We sacrificed prepayment penalties for Federal preemption of state usury ceilings in the 1980s • We fought hard in the early 1990’s, particularly at the end of the 1992-1993 Refinance Boom, to find a way to capitalize the costs to originate and, in 1995, we received the mixed blessing of FAS 122 • We created and actively sold “No Fee, No Cost” Bought-Up Refinances for more than a decade

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - II • While we often curse mortgage brokers when they can’t hear us, we don’t want to lose their volume since they control over 60% of the total market • This is true even though we suspect fraud, know that they aren’t fiduciaries for our borrowers and will churn the mortgage loans that they sell to us (although they may have to wait several months until the SRP no longer must be repaid or swap the borrower(s) with another mortgage broker)

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - III • Few lenders have made any effort whatsoever to offer prepayment affected mortgage loans: Bank of America, First Nationwide and Countrywide • Loan Officers and Mortgage Brokers don’t like the effective restriction on their market-given right to churn / refinance “their” borrowers • We need to become a far more accountable and proactive industry – since our low capitalized origins, we have only been in the reactive mode

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - IV • We love to blame others (particularly the GSE’s) for our eternal commitment to be a profit-proof business in the drive to originate more volume • Equitable prepayment penalties that can only be enforced when borrowers choose to refinance are currently supported very effectively by the GSE’s • It’s incomprehensible why this is not better known since prepay penalties really serve their purpose

Rate of Payoff Summary for 2002By Year of Origination (Annualized) Year to date through August 2002 annualized

Implied Remaining Life for 2002By Year of Origination (Annualized) * * * * * * * Estimated Year to date through August 2002 annualized

Rate of Payoff Summary for 2002By Year of Origination (Annualized) Year to date through August 2002 annualized

Five-Year Prepayment Penalty OptionConforming Prepay versusNo Prepay Data as of 09/06/02

Five-Year Prepayment Penalty OptionJumbo Prepay versus No Prepay 08/02 CPR

Prepayment ProductionAugust Bookings *Includes Bond, CalPERS, Correspondent and Government

Prepayment ProductionHistorical Bookings *Includes Bond, CalPERS, Correspondent and Government

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - V • To offset the growing belief that consumers are “entitled” to the one way street of free refinances, prepayment penalties should decline on an annual basis (say, six months of interest @ 100%, 80%, 60%, 40%, 20% on 80% of the remaining balance) • Investors haven’t been asked to participate in the prepayment penalties in a way to encourage their willingness to pay for the true value of the call preemption and we must educate / involve them

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - VI • In turn, why should our investors be willing to pay more for the risks of I/O strips than we mortgage bankers believe that they are really worth. • In the past, we have fought hard to preserve the minimum servicing fee (FannieMae has reduced it twice for Fixed-Rate Mortgages – 50.0 bps to 37.5 bps to 25.0 bps and Ginnie Mae has tried as well) since it was believed that the market would take the difference and we give away the gain anyway.

Mortgage Servicing Fees and MSR’s“The Borrower’s Free Option” - VII • In my view, the risk is the squeeze on mortgage bankers as simple intermediaries due to the fact that regulations and requirements change over time (rarely for the better in terms of costs) and mortgages that tend to remain in the servicing portfolio are more delinquent / costly to service • A reduction in servicing fees, due to continuous growth in average mortgage balances (not lower costs), may be okay while it will be gone forever

Quarterly Average Mortgage DelinquenciesLagged 2.5 Years versus 30-Year FNMA MBS Enhanced sub-prime delinquency tracking appears to explain the dramatic recent (1998) increase although FHA delinquencies have also had a material effect, despite incredibly strong real estate markets across the U.S. What will happens when rates rise creating higher loan default rates? FNMA Conventional MBS National Delinquency Survey

Record Month 3.97% Total Portfolio Delinquency RateMBA Method with Bankruptcies 2000 2002 2001 46bps Higher than Record Month Target 4.61% 4.41% 4.43%

Record Month 2.12% FannieMae Delinquency RateMBA Method with Bankruptcies 2000 2001 2002 10bps Higher than Record Month Target 2.49% 2.22%

Record Month 7.16% Ginnie Mae Delinquency RateMBA Method with Bankruptcies 2000 2001 2002 248bps Higher than Record Month Target 9.94% 9.56% 9.64%

Relative Mortgage Delinquency RatesBenchmarked By Channel • In my view, we are being lulled into a mild state of euphoria by what has been more than a decade and a half of robust property appreciation, great stock market results and the segmentation of weaker credits into the sub-prime industry (that has yet to be tested in a real estate recession) • When mortgage interest rates rise, and I believe that they will, we should be prepared for fairly difficult delinquency / default consequences - let’s all work to plan for this possible eventuality

August Delinquencies by Channel12-Month Rolling Book of Business I Reflects Percentage of McDash Industry Performance Data for 09/01/01 through 08/31/02

Mortgage Servicing Fees and MSR’sIn Summary • As previously stated, in my view, we are a totally reactive industry and I would caution the players to evaluate its most critical needs for change in terms of what the future may bring - not just in light of the most recent past, which has been 12 years of the best of times with several 18 month periods of increasing rates while mortgage rates have dropped from nearly 10.0% to the 5.0% level • Let’s all work to plan, and not react, for a change