Download

1 / 6

60 likes | 254 Views

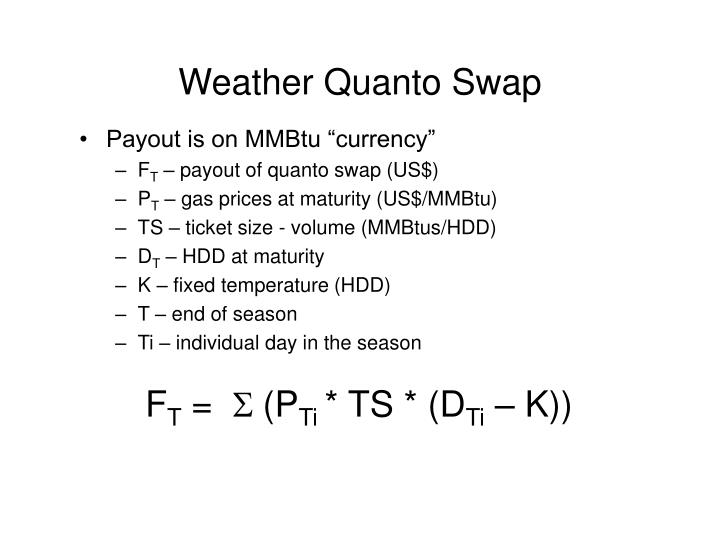

Weather Quanto Swap. Payout is on MMBtu “currency” F T – payout of quanto swap (US$) P T – gas prices at maturity (US$/MMBtu) TS – ticket size - volume (MMBtus/HDD) D T – HDD at maturity K – fixed temperature (HDD) T – end of season Ti – individual day in the season.

E N D

Weather Quanto Swap • Payout is on MMBtu “currency” • FT – payout of quanto swap (US$) • PT – gas prices at maturity (US$/MMBtu) • TS – ticket size - volume (MMBtus/HDD) • DT – HDD at maturity • K – fixed temperature (HDD) • T – end of season • Ti – individual day in the season FT = S (PTi * TS * (DTi – K))

Weather Quanto Swap • Model Assumptions: • Gas prices are lognormally distributed at maturity (Ti) with volatility sp and expected value Pt • HDDs are normally distributed with standard deviationsd and expected value Dt • The Log of Gas prices and HDD expected values are correlated at maturity r = correlation (DT, ln(PT))

Weather Quanto Swap • Pricing the contract: Ft = S Fti Fti = e-r(T – t) * TS * E[PTi (DTi – K)] t T Ti

Weather Quanto Swap • Pricing: • Deltas: • Cross Gamma: Fti = e-r(T– t) TS [ Pti (Dti –K) + Ptispsdr*(Ti-t)] Dpi = e-r(T– t) TS [ Dti + spsdr* (Ti-t)] Ddi = e-r(T– t) TS [ Pti ] Gdpi = Gpdi = e-r(T– t) TS

HDD 1 2 1HDD 2HDD T1 T2 t Gas 1gas 2gas T1 T2 t Weather Quanto Swap • Blended Correlation LN(Pgas vs HDD) : 1 * 1gas * 1HDD * (T1 – t) + 2 * 2gas * 2HDD * (T2 – t) = gas * HDD * (T2 – t)

Weather Quanto Swap • Relevant points: • Bending the LN(gas)-HDD correlation • Blending the gas volatilities • Delta hedging the gas position close to daily maturity (Ti)