Download

1 / 12

120 likes | 215 Views

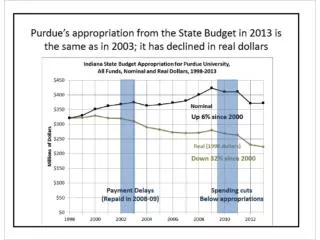

DEBT FUND ANALYSIS. Jun 01, 2008 – Jun 15, 2008. Debt Market Outlook. Short-term rates will head north. In the current situation because of a lack of clarity on the direction of yields, participants prefer the short end of the yield curve

E N D

DEBT FUND ANALYSIS Jun 01, 2008 – Jun 15, 2008

Debt Market Outlook • Short-term rates will head north. In the current situation because of a lack of clarity on the direction of yields, participants prefer the short end of the yield curve • Liquidity in June is expected to tighten further due to advance tax and other outflows, we can expect more money to be raised in short maturities in CD’s and CP’s • It has been observed that bond yields have a high correlation to crude prices. It will be one of the drivers; any fall in crude price can bring some relief rally to bond prices, but other than that, the market is in a negative sentiment after high inflation figure Debt Market Update • Market movements • Liquidity was tight (because of a CRR hike and payout of INR 10,000 crore) pushing O/N money market and short term rates up • RBI raised the FII investment limit in the debt market. Investment in the corporate debt market doubled to USD 3 bn, while limits in government debt were raised from USD 3.2 bn to USD 5 bn • Annual inflation for the week ended May 17 is 8.10%. The last time we saw a number higher than this was on September 11, 2004, when WPI was 8.15% • Strong correlation was seen between crude price and bond yields, where any fall in crude price resulted in easing of bond yields Liquidity/borrowings: • Liquidity was tight, pushing the money market rate to 7% plus levels • Average daily total liquidity was INR 88799 crore, while the weighted average rate was 7.46%, much higher than the previous week’s 5.77% • Tight liquidity pushed non-SLR rates northwards. One month CD yields went up from previous Friday’s 7.60% to 8.65% today • Debt Portfolio Strategy • Liquid Plus Funds are still a safer bet from a short term (3-6 months) horizon 2

Recommended Debt MF Categories • Liquid Plus Funds: • These funds have favorable portfolio composition. These funds are expected to invest close to 40% on higher side and 25% on the lower side in Corporate Bonds with maturity above 1 year • These funds are able to take advantage of rise in Overnight rates and also increase the portfolio yield by taking call in high duration bonds. In the current scenario where overnight rates are expected to remain high and yields on corporate bond to ease slightly from current levels. These funds are better positioned to take advantage of both the scenarios • These funds provide an indirect bet on Short to Medium term bonds. In case of 100% investment in these bonds an investor can be subject to mark to market compulsion and any rise in rates is likely to hurt the return on investment. However, with investment in Liquid Plus Funds an investor can take advantage of spread investment strategy of these funds • These funds are treated as an income fund and are exempt from the current rise in Dividend Distribution Tax. Old rate of Dividend Distribution Tax is applicable to these funds 3

Recommended Schemes in Liquid Plus Funds • Liquid Plus Funds – Retail & Institutional • DWS Money Plus Fund • ICICI Prudential Flexible Income Plan • JM Money Manager Fund – Super Plus Plan • LIC Liquid Plus Fund 7

Disclaimer This document has been prepared by Edelweiss and is strictly confidential and is intended for the use by recipient only and may not be circulated, redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of Edelweiss. Receipt and review of this document constitutes your agreement not to circulate, redistribute, retransmit or disclose to others the contents, opinions, conclusion, or information contained herein. In the preparation of the material contained in this document, Edelweiss has used information that is publicly available, including information developed in‐house Information gathered & material used in this document is believed to be from reliable sources and is given in good faith. Edelweiss however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material no such party will assume any liability for the same. Edelweiss and/or any affiliate of Edelweiss does not in any way through this material solicit any offer for purchase, sale of any financial transaction/commodities/products of any financial instrument dealt in this material. All recipients of this material should before dealing and or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice. The investments discussed in this material may not be suitable for all investors. Any person subscribing to or investigating in any product/financial instruments should do so on the basis of and after verifying the terms attached to such product/financial instrument. Edelweiss (including its affiliates) and any of its officers, directors, personnel and employees, shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, and consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/are liable for any decision taken on the basis of this material. Edelweiss has included statements/opinions/recommendations in this document which contain words or phrases such as “will”, “expect”, “should” and similar expressions or variations of such expressions, that are “forward looking statements”. Financial products and instruments are subject to market risks and yields may fluctuate depending on various factors affecting capital/debt markets. Please note that past performance of financial products and instruments does not necessarily indicate the future prospects and performance thereof. Actual results may differ materially from those suggested by the forward looking statements due to risks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and/or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. Edelweiss (including its affiliates) or its officers, directors, personnel and employees, including persons involved in the preparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation in the financial instruments/products/commodities discussed herein or act as advisor or lender/borrower in respect of such securities/financial instruments/products/commodities or have other potential conflict of interest with respect to any recommendation and related information and opinions. The said persons may have acted upon and/or in a manner contradictory with the information contained here. This document is intended to be used only by resident Indians, non‐resident Indians, persons of Indian origin, subject to the applicable laws and regulations of any Indian or foreign regulatory authority. This document should not be regarded as solicitation of business in any jurisdiction including India. Mutual Fund investments are subject to market risk please read the offer document carefully before investing. 12