Download

1 / 2

20 likes | 155 Views

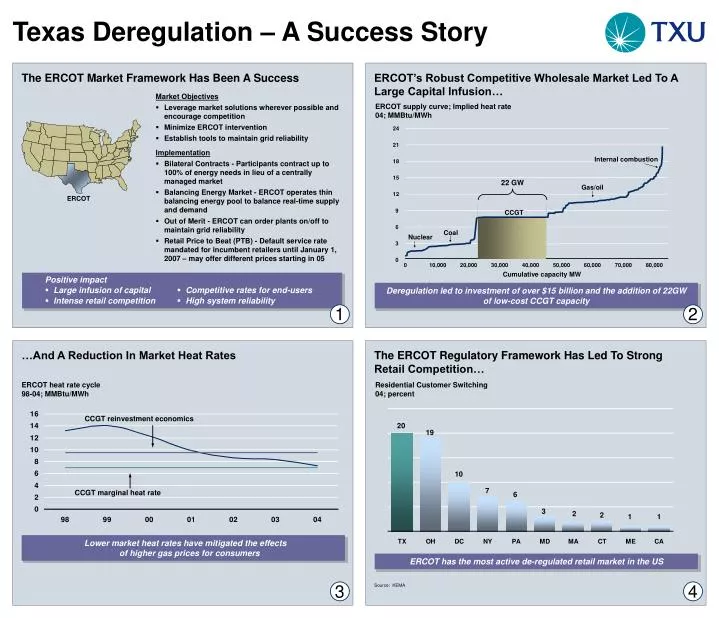

24. 21. Internal combustion. 18. The ERCOT Market Framework Has Been A Success. ERCOT’s Robust Competitive Wholesale Market Led To A Large Capital Infusion…. 22 GW. 15. Gas/oil. 12. Market Objectives Leverage market solutions wherever possible and encourage competition

E N D

24 21 • Internal combustion 18 The ERCOT Market Framework Has Been A Success ERCOT’s Robust Competitive Wholesale Market Led To A Large Capital Infusion… 22 GW 15 • Gas/oil 12 Market Objectives • Leverage market solutions wherever possible and encourage competition • Minimize ERCOT intervention • Establish tools to maintain grid reliability ERCOT supply curve; Implied heat rate 04; MMBtu/MWh 9 • CCGT 6 • Coal • Nuclear 3 0 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 Implementation • Bilateral Contracts - Participants contract up to 100% of energy needs in lieu of a centrallymanaged market • Balancing Energy Market - ERCOT operates thin balancing energy pool to balance real-time supply and demand • Out of Merit - ERCOT can order plants on/off to maintain grid reliability • Retail Price to Beat (PTB) - Default service rate mandated for incumbent retailers until January 1, 2007 – may offer different prices starting in 05 ERCOT Cumulative capacity MW Positive impact • Large infusion of capital • Intense retail competition • Competitive rates for end-users • High system reliability • Deregulation led to investment of over $15 billion and the addition of 22GWof low-cost CCGT capacity 1 2 …And A Reduction In Market Heat Rates The ERCOT Regulatory Framework Has Led To StrongRetail Competition… ERCOT heat rate cycle 98-04; MMBtu/MWh • Residential Customer Switching • 04; percent CCGT reinvestment economics CCGT marginal heat rate Lower market heat rates have mitigated the effectsof higher gas prices for consumers • ERCOT has the most active de-regulated retail market in the US 3 4 Source: KEMA Texas Deregulation – A Success Story

…Giving End Use Customers Access To Lower Prices • Competitive residential price1 vs. regulated rate • 02-04; Percent savings • Competitive large business price vs. regulated rate • 02-04; Percent 2 2 • Customers have benefited from access to lower electricity prices than they would have experienced under a regulated rate regime 1 Competitive Residential price based on 15% discount to TXU PTB as currently offered by market competitors, e.g., Utility Choice (14.6%), Cirro (14.6%) and Gexa (16.6%); Regulated world assumes 7.8 GW added capacity in the rate base at a cost of $600/kw, O&M costs approximately 20/kw-yr resulting in an average cost of $93/kw-yr average cost in the rate base 2 Based on 2004 with the following assumptions: Competitive prices assume $4.07/MMBtu Henry Hub gas price, 24X7 heat rate of 7.3 MWh/MMBtu, and incumbent residential gross margins of 30% and LC&I gross margins of 5% 5 6 7 8 Texas Deregulation – A Success Story …With Customer Switching In Line With Other Successful Deregulated Markets… • Incumbent market share1 • Years since deregulation; Percent • Wireline • North Texas residential • South Texas residential • UK residential2 1 Market share estimates based on customer count 2 Estimates for 2003 and 2004 Source: PUC; OFGEM There Is Still Room For Improvement In ERCOT… …As Key Milestones Approach • Sunset Review1 • The Sunset Advisory Commission reviews performance of The Public Utility Commission of Texas (PUC) and the Office of Public Utility Counsel (OPUC) every 12 years • The next review should be completed during the 2005 session • Key recommendations of the Sunset Advisory Commission include: • Changes to ERCOT/PUC governance structure • Extension of the PUC for 6 years • Market inefficiencies drive significant costs to market participantsacross the ERCOT system • The competitive market in Texas is functioning well andTXU does not anticipate any major structural changes in the marketplace 1 Estimated cost of bad debt for key ERCOT retailers in 2003; TXU retail bad debt in 2003 was $120 MM 2 OOME down cost to the system 3 Reduction of “ask” price to energy retailers of 0.2 cents / KWh on 300 TWh 4 Unaccounted for energy costs at 1% of load at $40 / MWh on 300 TWh (Line loss can represent an additional 5% of load cost) 5 Based on 6 month RMR costs for delay at La Palma of $15 million and 12 month RMR costs on delay at Davis of $30 MM 6 ERCOT requires approximately 2 GW of new capacity per year; better siting reduces transmission cost by $10,000 per MW 1 The Sunset process is guided by a 12-member body of legislators and public members appointed by the Lieutenant Governor and the Speaker of the House of Representatives.