Download

1 / 18

180 likes | 310 Views

Notes for Chapter 12. ECON 2390. Taxes to reduce pollution. Basic Tax Structures Income taxes (progressive, regressive, proportional or flat tax) Consumption (Sales and GST) Ad valorem (property, inheritance). Area a. Total costs minimized (area a + b). Area b.

E N D

Notes for Chapter 12 ECON 2390

Taxes to reduce pollution Basic Tax Structures • Income taxes (progressive, regressive, proportional or flat tax) • Consumption (Sales and GST) • Ad valorem (property, inheritance)

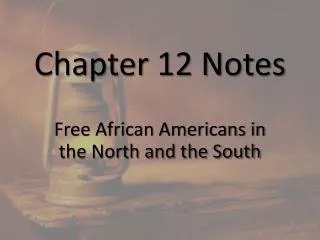

Area a Total costs minimized (area a + b) Area b The concept of cost minimization for abatement is related to the concept of elasticity in demand The basic math rests on geometry and the area defined by the rectangle that shows the marginal abatement cost/tax and emission level 3

Total cost of damages foregone = e + f (total cost of abatement + avoided losses to the pollutee) The net benefit is f Total tax paid by the polluter is a+b+c+d, plus the abatement cost. Taxes are more costly to the firm than standard Cost of a standard (set at E*) is just e. Why tax? What dangers exist in using a tax 4

A tax imposed on industry will cost differentially depending on abatement costs. Total abatement is 80 + 20 Kg/mo The book shows that an emission tax may have a lower social compliance cost than a uniform standard When abatements costs vary a tax may be more cost-effective ($/kg controlled) 5

Cost of tax + abatement creates an incentive to invest in new technology Industry 1: total cost = a+b+c+d+e Industry 3: total cost = b+d+e If the difference is technology the gain is a+ c 6

Taxes to reduce pollution Basic Tax Structures • Income taxes (progressive, regressive, proportional or flat tax) • Consumption (Sales and GST) • Ad valorem (property, inheritance)

Green Taxes • Some advocate replacing existing taxes on employment, incomes and profits (‘goods’) with taxes on energy use (‘bad’) • This is claimed to result in • better overall national economic performance; • higher levels of employment; • and a cleaner environment. • The goal is to shift the balance between human resources and natural resources. • Taxes are well known to shift resources: • Income taxes tend to reduce work effort • Sales taxes reduce consumption (cigarettes) • Carbon taxes are intended to reduce use of fossil fuels

Green Taxes • Problems • green taxes are regressive because they hit poorer people relatively harder than richer. • A tax on natural gas raises the cost of heating, cooking and lighting, it will consume a higher proportion of disposable income and poor people would find it harder to pay. • The effect is greater if we reduce income and taxes to really force the shift for which there are many exemptions.

Rehabilitating the Green Tax • Some studies show that redistributing the surplus as an eco-bonus creates a progressive tax. • Green taxes at the retail level are regressive, but imposed at the upstream are less so it affects all incomes – salaries, rents, profits, dividends, which tend to fall more of richer households. • Green taxes should form part of a broader tax reform. For example a general shift to wealth taxes and a move to value added taxes (GST) and away from income taxes. Caution: Progressivity in taxation is not the only goal. Other goals must be sustainability (resource allocation is not disturbed to erode the tax base), ease of administration, and enforcement.

Incentives and subsidies • The reverse of taxation are rewards for good behaviour • Subsidies are design to lower the costs of adopting new technologies or uses that are more expensive (private costs), but are believed to create social benefits. • Common examples • Incentives to insulate • Cash for hybrid purchase

Oilpatch to benefit from green initiatives, but alternatives left out Mike De Souza reported that Canada's wind energy sector is among the groups losing out in the federal budget which will maintain hundreds of millions of dollars in subsidies for fossil fuel industries in Western Canada. Robert Hornung, president of the Canadian Wind Energy Association, said the budget's failure to continue a federal incentive program for new projects will lead to jobs and investments heading to the United States. Mr. Hornung said he was "shocked and disappointed" that the government failed to renew the program. Steven Guilbeault of Equiterre, said "We're abandoning our commitment for the development of wind energy in Canada as opposed to our other G8 competitors or even countries like China and South Korea. It's not just an environmental catastrophe. It's a series of missed job creation opportunities" (Edmonton Journal, A4, 05 March 2010; Montreal Gazette, A4).

Canada’s Clean Air Agenda • The Government of Canada committed to reducing Canada’s total GHG emissions by 20% from 2006 levels by 2020 and by 60–70% by 2050; • In addition, to several other actions including: • a goal of having 90% of Canada’s electricity provided by non-emitting sources such as hydro, nuclear, clean coal, or wind power, by 2020 • continuing to advance the Clean Energy Dialogue with the US Administration • investing more than $2 billion through our Economic Action Plan to protect the environment, especially through technological transformation, while stimulating the economy • playing an active and constructive role at the UN climate change talks leading up to the Copenhagen conference in December –18, 2009 Environment Canada. Retrieved September 21, 2009, from http://www.ec.gc.ca/cc/default.asp?lang=En&n=18BA6889-1

Industry Associations http://www.canwea.ca/index_e.php

ecoEnergy for Renewable Power • NRCan program that offered 1¢ per kWh Other subsidies and “natural growth) Programs NRCan Programs

Ontario Feed-in Tariff http://fit.powerauthority.on.ca/

![[Notes 12]](https://cdn0.slideserve.com/443045/notes-12-dt.jpg)