Download

1 / 13

130 likes | 251 Views

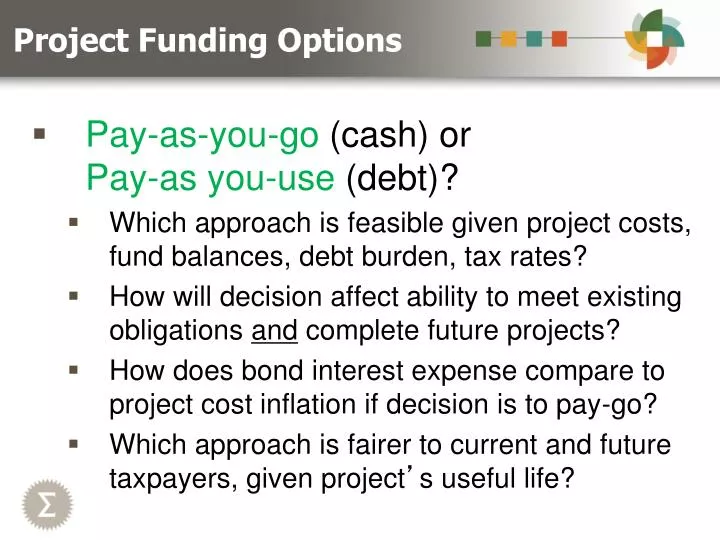

Project Funding Options. Pay-as-you-go (cash) or Pay-as you-use (debt)? Which approach is feasible given project costs, fund balances, debt burden, tax rates? How will decision affect ability to meet existing obligations and complete future projects?

E N D

Project Funding Options • Pay-as-you-go (cash) orPay-as you-use (debt)? • Which approach is feasible given project costs, fund balances, debt burden, tax rates? • How will decision affect ability to meet existing obligations and complete future projects? • How does bond interest expense compare to project cost inflation if decision is to pay-go? • Which approach is fairer to current and future taxpayers, given project’s useful life?

Parameters: Internal • Project costs and timing • Plus: Other future financing needs? • Available funds and future revenues • Estimated bond interest rates • Also: Investment rates on fund balances • Council / community positions

Parameters: External • Authorization in State Law • Types of municipal debt • Process for approval and issuance • Federal Regulations • IRS: Tax-Exempt Uses; Arbitrage Rebate • MSRB / SEC: Post-Issuance Compliance • Market Forces • Rating Agencies: Credit Quality • Investors: Rates, Terms and Conditions

Project Funding Plans • Given parameters, what are options? • Which will deliver funding when needed? • Which is affordable: now and in future? • Which is good policy and precedent? • Which is politically viable? • Result = Project Funding Plan

Fix the Fork Funding Plan 1 • Estimated Cost: $7.5 Million • POST Cash: $2.0 million • General Fund Cash: $650,000 • G.O. Bond Proceeds: $4.85 million • Two Bond Issues: Tax-Exempt and Taxable • $2.0M POST Cash Uses • River restoration / flood mitigation • Relocation necessary for River project • Park improvements • Other POST-eligible uses TBD

Fix the Fork Funding Plan 2 • $650,000 General Fund Cash Uses • 100% of relocation necessary for Pan & Fork Site (RFCDC-owned parcel) redevelopment • Other private or public uses TBD • $4.85M G.O. Bond Proceed Uses • Tax-Exempt: River restoration and other public costs not paid with POST / GF cash • Taxable: Pan & Fork site and RMI site improvements, all other private development costs not paid with GF cash

Fix the Fork Funding Plan 3 • G.O. Bond Ballot Question • Authority to issue bonds, pledge full faith and credit and unlimited property tax ability • But Town intends to “cancel” all of authorized debt levy debt with other revenues, not raise property taxes above existing level • Tax-Exempt / Taxable Bond split is TBD • Not part of ballot question, other than estimated cost • Town will err toward taxable to fund “gray area” costs as higher interest cost < cost of IRS audit / penalty

Fix the Fork Funding Plan 4 • Repayment of Tax-Exempt Bonds • Pay mostly from future POST revenues • General taxes for bond portion funding non-POST costs (i.e. streets / utilities) • Plan: offset / reimburse general taxes with Basalt Sanitation District, future special assessments • Repayment of Taxable Bonds • Pay near-term from existing general taxes • Use future assessments and development charges / agreements to reimburse Town and pay off bonds early (if possible)

GO Bond Example • Estimated GO Bond amount: $5.0 Million • 10 year repayment term (2014 – 2023) • “Worst Case” blended interest rate: 5.00% • Current estimated blended rate is 3.00% • “Worst Case” annual debt service: $650,000 • Repayment sources: • 1% POST sales tax ($1.2 million annually) • Existing General taxes (property and 2% sales) • External: Basalt Sanitation District, assessments

Bond Issuance Participants • Issuer: Town of Basalt • Independent Bond Advisor: Ehlers • Bond Counsel: Kutak Rock • Rating Agency: Standard & Poor’s • Paying Agent: TBD • Bond Underwriter: TBD • Bondholders: TBD

Bond Issuance Process 1 • Key Pre-Election Steps • August 13: Council reviews funding plan and ballot question, authorizes staff to proceed • August 27: Council calls for November 6 election on ballot question • September 20: TABOR pro/con statements submitted to counties for distribution to voters • September – October: Town mailer, website, other outreach as permitted by state law • October 15: Counties mail ballots to voters

Bond Issuance Process 2 • November 5: Election Day • If Voters Approve Question • November 12: Council authorizes bond sales • November 18: S&P rating call / visit • November 26: Competitive bond sales and Council award to winning bidders • Mid-December: Town receives and invests bond proceeds (in sync with project timeline) • Ongoing: Post-issuance compliance

Discussion • Town Policy: Cash vs. Debt • Fix the Fork Funding Plan • G.O. Bonds: Uses, Debt Service, Participants, Issuance Process • Proposed Ballot Question andKey Steps / Dates