Download

1 / 37

370 likes | 495 Views

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Regis Coccia, Managing Editor Business Insurance Ed Wrobel, Tillinghast-Towers Perrin Julie E. Robertson, Honigman Miller Schwartz and Cohn LLP Paul Longman, Employers Re Seamus Tivnan, Marsh Cayman Islands. ART AND SCIENCE

E N D

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Regis Coccia, Managing Editor Business Insurance Ed Wrobel, Tillinghast-Towers Perrin Julie E. Robertson, Honigman Miller Schwartz and Cohn LLP Paul Longman, Employers Re Seamus Tivnan, Marsh Cayman Islands

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Ed Wrobel Tillinghast-Towers Perrin phone: (860) 843 7022 fax: (860) 843 7001 email: ed.wrobel@tillinghast.com

Why ART?The Buyers’ Perspective • $1B+ in premium needs to find a home • (St Paul, PHICO, MIIX, Reliance, Reciprocal of America….) • Substantial increases in rate and retention • Limitations in coverage • Non-renewals => Significantly greater risk retention required of smaller entities => Formalization of risk retention vehicle

The Buyers’ Perspective “Our loss experience is better than average - we’re being painted with a broad brush”

The Actuarial Perspective “Our loss experience is better than average - we’re being painted with a broad brush” – – Really?

The Actuarial Perspective • The captive feasibility study • Actuarial / financial analysis • Legal / regulatory / tax issues • Coverage / structure • Reinsurance

The Actuarial Perspective • Key Issues in the Current Environment • Critical Mass • Economically feasible to absorb frictional costs • Stability / predictability of loss costs • Capital/surplus • Adequacy for smaller entities

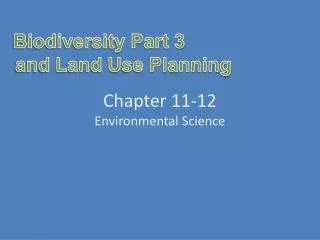

Margin/Surplus Levels Mean Value Probability 90% Confidence Level Margin $ $5M $8M

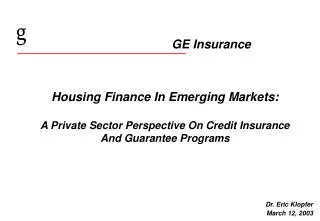

Margin/Surplus Levels Mean Value Probability 90% Confidence Level Margin $ $300K $1M

The Actuarial Perspective • Key Issues in the Current Environment • Credibility of data • Consistency: changing carriers • Case reserve adequacy / strengthening • Reliance on industry information • Impact of trends, legislative changes • Source / mechanism for funding in the event of adverse experience • Affordability

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Julie E. Robertson Honigman Miller Schwartz and Cohn LLP (313) 465-7520 jrobertson@honigman.com

Characteristics of physician practices: • No retained earnings/no available capital • No “institutional mindset • No long term view of insurance • No experience with risk retention • Poor access to loss history/data • Tail coverage issues • Premium deductibility issues Historically, few physician captives because:

Different practice models: • National provider groups • Bigger local groups • Employing business/financial professionals • Retained earnings and investments • More opportunity for premium deductibility • Insurance market, insurance market, insurance market! “Oh, the times they are a changing”

June 2001 Rev Proc./Dec 2002 Rulings • Abandonment of “economic family doctrine” • 2002-89: Single parent captive/90% risk parent/10% risk 3rd parties = No Insurance • But 50% risk parent/50% risk 3rd parties = Insurance • 2002-90: Single parent captive/12 subsidiaries = Insurance • 2002-91: group captive; no one insured more than 15% stock/15% risk = Insurance Premium Deductibility

Rev Proc 2002-75: IRS will now begin issuing private letter rulings regarding tax treatment of captive insurance arrangements • Highly factual; likely expensive and time consuming process • If you have to ask . . . Premium Deductibility

4% direct premium/1% reinsurance premium • Not applicable if captive makes a 953(d) election Federal Excise Tax and Reinsurance Transactions

Must have “risk” to have insurance • Security requirements equal to aggregate limits can undermine deductibility Premium Deductibility and Security Requirements

State may require purchase of insurance from approved carriers or for fund participation • Example: Pennsylvania/medical malpractice insurance • State regulatory environment or attitude may affect decision • State Department of Insurance may view direct issue captive as transacting insurance within state and attempt to regulate it Why Do Physicians Choose a Fronted Program?

Third party insureds may feel more comfortable with commercial policy • Insureds may be required to maintain insurance from rated carrier or approved carrier under • Bond/debt/credit facility covenants • Medical staff bylaws • Managed care contracts • Other contracts Why Do Physicians Choose a Fronted Program?

Health Care Providers must ensure the privacy of protected health information shared with their business associates • Impact on fronted captive programs • Policy endorsements and required elements • Passing the information “down the chain” • Can information be redacted? HIPAA Privacy Rules

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Paul Longman Email : Paul.Longman@ercgroup.com

By definition, ART Customer is: • Seeking options to conventional insurance and/or 100% risk transfer • Wishes to retain a “predictable” level of risk • Seeks to transfer “unpredictable” level of risk: per occurrence or aggregate • Reinsurer usually provides excess coverage Art & Science - A Reinsurer’s Perspective

What we look for……. “Size Matters!” • Single entity or strong affiliation/relationship between members • Commitment to long term risk financing solution • Desire and ability to retain an appropriate level of loss • Strong financials Art & Science - A Reinsurer’s Perspective

What we look for……. “Size Matters!” • Commitment and resources to Risk Management/Loss Prevention Program • Creditable historical loss data • Competent claims handling via in-house staff or TPA. • Clear/unambiguous coverage forms - “clear understanding of what is covered” Art & Science - A Reinsurer’s Perspective

What we look for……. “Size Matters!” • Actuarial Projection of expected losses • Acceptable funding mechanism for expected losses Art & Science - A Reinsurer’s Perspective

Captive documentation • Business Plan • Articles of Incorporation/Articles of Assoc.. • Bylaws • Verification of Capitalization • Certificate of Incorporation • Certified copy of Certificate of Authority (USA) or Certificate of Registration (offshore) Art & Science - A Reinsurer’s Perspective

Comments on fronting: • Rating and viability of front is crucial • Universe of willing fronting companies has shrunk • Front fees vary significantly - policy issuance and required servicing are major factors. Servicing can be done by customer, broker, fronting co. or others Art & Science - A Reinsurer’s Perspective

Comments on fronting: • Risk ceded back to customer from fronting co. or reinsurer usually must be fully collateralized *some companies require collateralization = to the full aggregate exposure *others will require collateralization = to expected losses + a provision for adverse development *acceptable collateralization: ever-green LOC or trust agreement Art & Science - A Reinsurer’s Perspective

ART AND SCIENCE Plus Medical PL Symposium March 11-12, 2003 Seamus Tivnan Marsh Management Services Cayman Ltd. Tel 345 949 7988 Fax 345 949 7849 Email Seamus.Tivnan@marsh.com

Risk Retention Group • Reciprocal • Captive Insurer • Pure • Group / Association • Segregated Cell • Domiciles • United States • Offshore Art & Science Captive Options

Largest Domicile in the World for Healthcare • 199 healthcare captives with $1B in premium and $4.3B in assets • First Class Infrastructure • Proven Reputation • Accessibility • Doing Business in Cayman Art & Science Why Cayman?

Why? • Affordability • Availability • Accessibility • Or • Attract ability Art & Science So you think you want a captive?

Minimum Size • Premium, capital • Costs • To consider, establish and operate • Administration • Home office, plus Director and Officer obligations • Long term commitment Art & Science So you think you want a captive?

The Regulator – that’s the easy part • Fronting • Do you need it? Can you find it or even afford it? • Reinsurance • Do you need it? Can you find it or even afford it? • Funding • It may be more expensive • Pay more premium or more capital? • Taxation • ‘Exists’ in all domiciles Art & Science So you still want a captive?

Tax Deductibility & Structure • Strength in numbers • Segregated Cell Approach • Funding – be it premium or capital • Funding – retro element, good or bad? • Fronting • Commitment – to begin and continue • Old programs struggle as members leave Art & Science Physician Groups – Why they do not start and why they fail?

Timing • Select domicile • Select partners – actuary, attorney, auditor, banker, manager, tpa • Select Board of Directors • File Application – with fee • Capitalize Company and hold first meeting Art & Science Captive Go Ahead