Download

1 / 10

• 100 likes • 299 Views

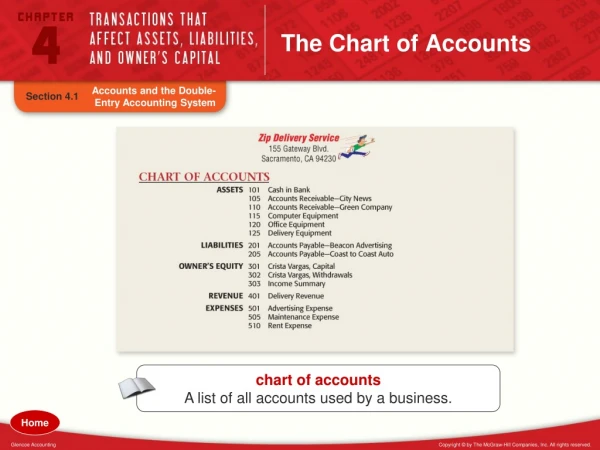

Understanding the chart of accounts. Prepared by: Kelly murray-scott Lambton college finance department November 17, 2009 Revised: September 25 th , 2014. General ledger account structure . Department (1 st 4 digits of the cost centre) 1-701004-44200

E N D

Understanding the chart of accounts Prepared by: Kelly murray-scott Lambton college finance department November 17, 2009 Revised: September 25th, 2014

General ledger account structure Department (1st 4 digits of the cost centre) 1-701004-44200 Fund Cost Centre Object Operating – International/Wuxi – Office Expense

Funds • 1 – Operating • Used for the majority of academic and administrative departments • 2 – Capital • Used for tracking capital spending – equipment, furniture, buildings, etc. • 4 – Foundation • Used for revenue and expenses generated by the Lambton College Foundation and Alumni • 5 – Restricted • Used to track funds that are restricted for specific uses (i.e. scholarships, conferences, etc.) • 6 – Ancillary • Used for the bookstore, parking and residence accounts • 7 – Fireschool • Used for all activity within the fireschool as it pertains to the industrial activity

Revenue The most common revenue accounts include: 40xxx 41xxx 42xxx Revenue received from MTCU 44xxx for programs run by Lambton 44xxx 45xxx 46xxx – Any fees paid by students for services provided by the College 47xxx – Revenue earned from ancillary operations 48xxx – Revenue earned from delivering contracted services 49xxx – Revenue earned from miscellaneous sources (i.e. the Foundation) Revenue accounts should only be used to record funds earned by the College. Revenue accounts typically maintain a credit balance. Expenses should not be posted to revenue accounts except for anomalies like deferred revenue adjustments.

Expenses The most common revenue accounts include: 40xxx – FT Academic Salaries 41xxx – FT Administrative Salaries/PT Academic 42xxx – FT/PT Support Salaries 43xxx – Benefits 44xxx – General and Instructional Expenses 45xxx – Building and Equipment Maintenance 46xxx – Fees and Contracted Services 47xxx – Expenses Related to Premises 48xxx – Expenses Related to Equipment 49xxx – Miscellaneous Expenses Expense accounts should only be used to record amounts payable by the College. Expense accounts typically maintain a debit balance. Revenue should not be posted to expense accounts except for anomalies like recovery/ reimbursement for expenses (i.e. 44090).

Clarification of Contracted Services • These accounts include: • 465xx – Contract Services Instructional Payroll • Used to pay all instructors in non-post secondary courses that will be paid through payroll (the instructors do not invoice the College) • 46570 – Contract Services Instructional Non-Payroll • Used to pay all instructors in non-post secondary courses that will be paid through an invoice issued to the College • 46901 – Contract Services Non-Instructional Payroll • Used to pay all contracted employees who are not teaching (i.e. consultants) and will be paid through payroll • 46970 – Contract Services Non-Instructional Non-Payroll • Used to pay all contracted employees who are not teaching and will be paid through an invoice issued to the College Notes: These four accounts should not be used for any part-time, partial load instructors or part-time support staff. The contracted services paid through payroll are subject to a “benefit” charge announced at budget/forecast time to cover the College’s costs of CPP, EI, EHT, etc.

Things to Remember • The College’s fiscal year runs from April 1st to March 31st (the current year is always referred as the year it ends i.e. for fiscal year 2014-15 it is referred to as 2015) • End users should never post to fulltime salary of benefit accounts (40100, 41500, 42000, 43000, 43400, 43600) – any adjustments to these accounts needs to be authorized/made by Finance • Benefit accounts should never be used on their own (43xxx, 4654x, 46944) – they should only be used in relation to the corresponding payroll • Post expenses to their proper accounts – if the line does not exist, contact Finance to add it to your cost centre • An employee cannot be both on payroll and contract (non-payroll) • If something has been posted to the wrong account, please send a journal entry form with backup to Finance • When in doubt…just ask