Download

1 / 20

370 likes | 1.23k Views

Calculating the profit or loss of a business. * Profit (what it is and why it matters) * Purpose and main elements of profit/ loss account. All students…. Explain the concept of profit. Understand the main elements of a profit/loss account statement. Higher level thinking….

E N D

* Profit (what it is and why it matters)* Purpose and main elements of profit/ loss account All students…. Explain the concept of profit. Understand the main elements of a profit/loss account statement. Higher level thinking…. Show understanding of why profit matters to a private sector business. Show awareness of the distinction between retained and distributed profit Distinguish between cash and profit. Show awareness of why cash and profit differ.

Types of financial analysis • Many types of financial reports are concerned with planning ahead. • These include cashflow forecasting, break-even analysis and budget setting. • Others are concerned with reporting results at the end of the year. • These include the profit and loss account and the balance sheet.

The purpose of a profit and loss account • It summarises all the sales revenue for the financial year. • It summarises all the payments or expenses for the same year. • The difference between the two totals is theprofit or loss made in that year.

Two Types of Profit • Gross Profit • Net Profit • Formula: • Sales revenue – Cost of Sales = Gross Profit • Gross Profit – Expenses = Net Profit

Stages: Sales Revenue • Sales are the amount of Money received by selling goods • If you sold 500 pairs of shoes at $100 each then the value of your sales revenue would be…. • $50,000

Stages; Cost of Sales • Expenditure which is made specifically to produce or sell the item. • Purchases (raw material and Stock) • Assume each shoe cost $50 to buy from the manufacturer • 500 x $50 = • $25,000

Stage: Gross Profit • Profit from the sales • Sales revenue – Cost of Sales • $50,000 - $25,000 = • $25,000

Stage: Expenses • Cost of running the business • You operating costs/ Fixed costs/ Overheads • Rent/ wages/ utilities • = $8,000

Stage: Net Profit • Deducating your expenses from your gross Profit • $25,000 - $8,000 = • $17,000 (then you pay inland revenue!)

Lets try…. AGAIN!

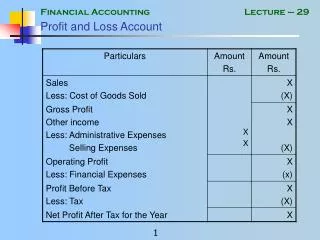

The structure of a profit and loss account 1 Top part is concerned with gross profit, e.g. $ Sales 300,000 Cost of sales 100,000 Gross profit 200,000 Note: cost of sales is the same as ‘cost of purchases’. It is deducted from sales.

The structure of a profit and loss accounts 2 Second part is concerned with net profit, i.e. gross profit minus expenses. $ Gross profit200,000 Expenses Salaries 55,000 Rent 10,000 Other 5,000 Total expenses70,000 Net profit 130,000

Your turn! 160,000 90,000 70,000

Cost of sales • Pg 194 Cost of sales 7842 • Opening Stock 189 • Purchases 4968 5157 • Less closing stock 53 5104 Gross Profit 2738

The importance of Profit • They provide a measure of the success of a business • They provide funds for investment in further fixed assets • They act as a magnet to attract further funds from shareholders enticed by the possibility of high returns on their investment • Profit is a source of more than 60% of all finance used to help companies grow; without profit, firms would stand still.

Why produce a profit and loss account? • It is a legal requirement. Tax is paid on the profit. • It summarises all the year’s transactions – as recorded in documents such as invoices. • It shows the financial ‘health’ of the business. • It is studied by managers, shareholders, banks, financiers and other relevant groups of people.

The Appropriation account Figure 35.4 pg 196