Download

1 / 36

360 likes | 372 Views

Explore the basic concepts of production function and how to optimize inputs to maximize output. Learn about isoquants, economic areas, and the elasticity of substitution.

E N D

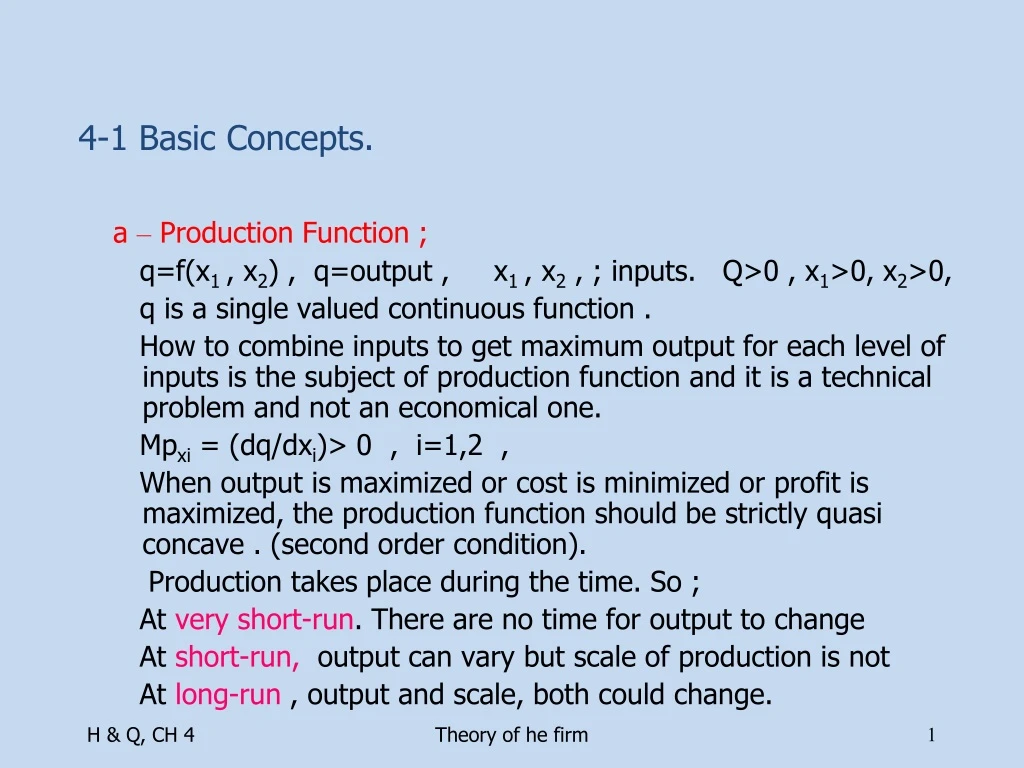

4-1 Basic Concepts. a – Production Function ; q=f(x1 , x2) , q=output , x1 , x2 , ; inputs. Q>0 , x1>0, x2>0, q is a single valued continuous function . How to combine inputs to get maximum output for each level of inputs is the subject of production function and it is a technical problem and not an economical one. Mpxi = (dq/dxi)> 0 , i=1,2 , When output is maximized or cost is minimized or profit is maximized, the production function should be strictly quasi concave . (second order condition). Production takes place during the time. So ; At very short-run. There are no time for output to change At short-run, output can vary but scale of production is not At long-run , output and scale, both could change. Theory of he firm

Q=F(x1,x2) x2 Iso-quant Economic area x1 Theory of he firm

Q2>Q1 Q2 Q1 Economic area q=f(x1,x2) q=f(x1,x2) x2 x1 o Theory of he firm

4-1 Basic Concepts TPx1 q=f( x1) ECONOMIC AREA ECONOMIC AREA B- Production curves; q=f( x1, x02) ωx1=d(lnq)/d(lnx1) ωx1=[dq/dx1][x1/q] ωx1=MPx1/APx1 I ; MP>0,AP>0 ,ωx1>0 MP>AP, ωx1>1 Not economical to Stop production. Scale Of the production is big compare To the volume of production. Either The volume of production should Increase or scale should decrease. (x20/x1) is larger than optimal II; MP>0,AP>, ωx1>0 MP<AP, ωx1<1 (x20/x1) is in optimal size, it is Economical to stop when Profit is maximized. x1 I I II III APx1 MPx1 Max MPx1 Max APx1= MPx1 MPx1 APx1 x1 Theory of he firm

4-1 Basic concepts I ; MP>0,AP>0 , ωx1>0 MP>AP, ωx1>1 Not economical to Stop production.Scale of the production is big compare To the volume of production. Either the volume of production should Increase or scale should decrease. (x20/x1) is larger than optimal II; MP>0,AP>, ωx1>0 MP<AP, ωx1<1 It is economical to stop production when profit is maximized. Scale of production (x20/x1) is optimal. . III; MP<0, AP>0, ωx1<0 Is is economical to decrease production . The scale of production (x20/x1) is small compare to the volume of production . Either the scale of production should increase or the volume of production should decrease Theory of he firm

4-1 Basic concepts x2 MPx2=0 C - Isoquant q=f(x1,, x2) dq=(df/dx1)x1 + (df/dx2)x2 dq= f1x1 + f2x2 RTS= - dx2/dx1 = f1/f2 If; q=q0 , x1=h(x2, q0) is the isoquant function . Economic Area x1 MPx1=0 Theory of he firm

4-1 Basic concepts As it is seen from the figures , production functions are strictly quasi-concave, when production is in the economic area. q=f(x1,x2,……xn) , if n=even the condition for concavity ; f11 f12…..f1n f11 f12 f13 f11 f12 f21 f22…. f2n ,….. f21 f22 f23 f21 f22 f11<0 …………….. f31 f32 f33 fn1 fn2… fnn If q=f(x1, x2) , then the condition is; f11<0 , f11 f12 , (f11f22– f122) > 0 , f22<0 ,, f21 f22 <0 >0 <0 >0 Theory of he firm

4-1 Basic concepts d- Elasticity of substitution ; σ = dln(x2/x1)/dln(f1/f2)=[(f1/f2)(x2/x1)][d(x2/x1)/d(f1/f2)] q=f(x1,x2) , d(x2/x1)=(x1dx2– x2dx1)/x12 , d(f1/f2) = [∂(f1/f2) /∂x1]dx1+[∂(f1/f2) /∂x2]dx2, (f1/f2)=-(dx2/dx1) σ =f1f2(f1x1+f2x2)/x1x22 D D= 2f12f1f2 – f12f22 - f22f11 If q is strictly concave, then; dRTS/dx1 = d (f1/f2) /dx1 <0 , we will prove that D>0 and so σ >0 C.E.S. P.F. σ =constant C.D. P.F. σ =1 x2 f1/f2 B A tan a =x2/x1 x1 Theory of he firm

4-1 Basic concepts d(RTS)/dx1 = d(f1/f2)/dx1 = d(-dx2/dx1)/dx1 <0 d(f1/f2)/dx1 = [f2(f11dx1 + f12dx2) – f1(f21dx1 + f22dx2)]/f22 <0 d(f1/f2)/dx1 = {f2[f11+f12(dx2/dx1)] – f1[f21 + f22(dx2/dx1)]}/f22<0 d(f1/f2)/dx1 = {f2[f11+f12(-f1/f2)] – f1[f21 + f22(-f1/f2)]}/f22<0 d(f1/f2)/dx1 = {f22f11 -2 f1f2f12 + f22f12}/f22<0 (f22f11 -2 f1f2f12 + f22f12)<0 or D=- f22f11 +2 f1f2f12 - f22f12)>0 , σ >0 Theory of he firm

4-2 Optimization behavior Out put maximization Max Q=f(x1,x2) S.T. C0=r1x1+r2x2 +b (b=fixed cost , ri=input price, C=total cost) L=f(x1,x2)+λ(C0– r1x1– r2x2– b) F.O.C. ; (∂L/∂x1)= f1 - λ r1=0 (∂L/∂x2)= f2 - λ r2=0 (∂L/∂λ)= C0– r1x1– r2x2– b=0 (f1/f2)=(r1/r2)=RTS=locus of expansion path λ =marginal productivity one unit of money=(f1/r1)=(f2/r2) S.O.C. ; f11 f12 -r1 f21 f22 -r2 >0 -r1 -r2 0 (f11r22– 2f12r1r2 + f22r12)<0 , f1= λr1 , f2= λr2 , f11(f22/ λ2)-2f12(f1/ λ)(f2/ λ)+f22(f12/ λ2)<0 (f22f11 -2 f1f2f12 + f22f12)<0 or D=- f22f11 +2 f1f2f12 - f22f12)>0, convex Isoquant E.P. x2 q1 q0 E x10 x1 c0 c1 Theory of he firm x20

4-2 Optimization behavior Cost minimization Min C=r1x1 + r2x2 + b S.t. f(x1,x2)=Q0 L=r1x1+r2x2 +b+μ[Q0– f(x1,x2)] F.O.C. ; (∂L/∂x1)= r1 - μf1=0 (∂L/∂x1)= r1 - μf1=0 (∂L/∂ μ)= Q0 - f(x1,x2)=0 (f1/f2)=(r1/r2)=RTS=locus of expansion path μ=marginal cost of producing one unit of output=r1/f1=(r2/f2 )=1/λ S.O.C. ; - μ f11 - μ f12 -f1 -μf21 - μf22 -f2 >0 -f1 -f2 0 D=- f22f11 +2 f1f2f12 - f22f12)>0, convex Isoquant . Theory of he firm

4-2 Optimization behavior All the points on the expansion path belongs to a concave production function and is the solution for both constraint cost minimization and constraint output maximization. (f1/f2)=(r1/r2) , x1 = g(x2, r1, r2) expansion path Profit maximization; Π=pf(x1,x2) – r1x1– r2x2– b (∂Π/ ∂x1)=pf1– r1 = 0 r1=pf1 = VMPx1 (∂Π/ ∂x2)=pf2– r2 = 0 r2=pf2 = VMPx2 (∂2Π/ ∂x12) (∂2Π/ ∂x1 ∂x2) pf11 pf12 (∂2Π/ ∂x2 ∂x1) (∂2Π/ ∂x22) pf21 pf22 Pf11 Pf12 Pf21 Pf22 >0 P2(f11f22– f122) >0 (f11f22– f122) >0 convex isoquant (r1/r2)=(f1/f2) expansion path >0 >0 Theory of he firm

4-3 Demand for inputs Π=pf(x1,x2) – r1x1– r2x2– b (∂Π/ ∂x1)=pf1– r1 = 0 x1=g(r1 , r2 , p) (∂Π/ ∂x2)=pf2– r2 = 0 x2=g(r1 , r2 , p) demand for inputs are homogeneous of degree zero with respect to prices of input and output. pf11dx1 + pf12dx2 = - f1dp + dr1 pf21dx1 + pf22dx2 = - f2dp + dr2 `dx1=[1/(PD)][f22dr1– f12dr2 + (f12f2– f22f1)dp] dx2=[1/(PD)][-f21dr1 + f11dr2 + (f21f1– f11f2)dp] D= (f11f22– f122) > 0 concavity condition if dr2=dp=0 then (dx1/dr1)= (∂x1/ ∂r1)=(f22/PD)<0 [f22<0,D>0] slope of the demand curve (∂x1/ ∂r1) is always negative. Theory of he firm

4-3 Demand for inputs If dp=dr1=o,and f12>0, then, (dx1/dr2)=(∂x1/∂r2)=(-f12/PD)<0 if [f12 >0 ,D >0] (dx1/dp)=(f12f2– f22f1)/(PD)>0 in a competitive situation, when there is increase in price of output, increase in the level of production will increase demand for inputs. Le Chatelier Π=pf(x1, x2, x3,….xn) – Σ rixi (∂xi*/∂ri)0≤ (∂xi*/∂ri)1 ≤ (∂xi*/∂ri)2 ≤………… ≤ (∂xi*/∂ri)n-1 (∂xi*/∂ri)n-1 = optimum level of xi with n-1 constraint, when profit is maximized. when the number of constraints increases, the variation in input level xi should be larger in order to compensate the inflexibility of change in those inputs who are binding by the constraints. Theory of he firm

4-3 Demand for inputs (∂x1*/∂r1)0 = f22/pD two inputs no constraint . if x2 is constrained by x2=x2* , Π=pf(x1 , x*2) – r1x1– r2x*2– b (∂Π/ ∂x1)=pf1– r1 = 0 pf11dx1– dr1 = 0 (dx1/dr1) =[1/(pf11)] (∂ x1*/∂r1)1=[1/(pf11)] we have to prove that ; (∂x1*/∂r1)0 = f22/(PD) ≤ [1/(pf11)]= (∂x1*/∂r1)1 [f11f22/D] ≥ 1 D= f11f22– f122 >0 concavity condition. f11<0 , f22<0 Theory of he firm

x2 4-4 Cost – Function q3 Expansion path q2 g(x1 , x2 ) =0 Short run ; q=f(x1 , x2) c = r1x1 + r2x2+ b g(x1 , x2 ) =0 c=φ(q , r1 , r2) + b Cost functions characteristics; 1- non-decreasing 2- homogenous of degree one in input prices 3-concave with respect to input prices q1 x23 p3 x22 p2 p1 x21 c1 x1 c2 c3 x11 x12 x13 q1=f(x11, x21) c1=r1x11 + r2x21 q2=f(x12,x22) c2=r1x12 + r2x22 q3=f(x13,x23) c3=r1x13 + r2x23 c=φ(q , r1 , r2) + b Theory of he firm

4-4 Cost - function x2 r11x11+r21x21= c1=φ(q*,r11,r12) q* φ(q*,r21,r22) r12x12+r22 x22 =c 2 = r11x12 +r21x22 r12=λ r10 +(1-λ) r11 x21 r10x12 + r20x22 r22=λ r20 +(1-λ) r21 x22 r 1 0x10+r2 0x20=c0 = c0φ(q*,r01,r02) x20 r10x12+r20x22 ≥ φ(q*,r01,r02) x1 r11x12 +r21x22 λ ≥ φ(q*,r11,r12) X11 x12 x10 [r10x12+ r20x22] ≥λ φ(q*,r01,r02) (1-λ) [r11x12 +r21x22] ≥ (1-λ) φ(q*,r11,r12) (r11/ r21) (r12/ r22) (r10/r20) [λr10 +(1-λ) r11]x12+[λ r20 +(1-λ) r21] x22≥ λφ(q*,r01,r02)+(1-λ) φ(q*,r11,r12) (r12 x12 + r22x22)= φ(q*,r21,r22) ≥ λ φ(q*,r01,r02)+ (1-λ) φ(q*,r11,r12) Theory of he firm

C=φ(q*,r1,r2) c2= φ(q*,r21,r22) c0=φ(q*,r01,r02) λφ(q*,r01,r02) + (1-λ)φ(q*,r11,r12) r1 c1=φ(q*,r11,r12) x0 r01 r12 x1 r11 r02 r12 r2 r22 Theory of he firm

4-4 Cost function . suppose that q=Ax1ax2b (f1/f2)=(r1/r2) (aAx1a-1x2b)/(bAx1ax2b-1)=(r1/r2) (ax2/bx1)=(r1/r2) q=Ax1ax2b C=r1x1+r2x2 TC= Ba q [1/(a+b)] , B=(a+b)[(r1a r2b)/(Aaabb)](1/a+b) AC = Ba q(1-a-b)/(a+b) MC = [Ba/(a+b)] q(1-a-b)/(a+b) = AC/(a+b) If (a+b) =1 , cost functions are linear,constant return to scale ; AC , MC C TC=Baq AC=MC=Ba q q Theory of he firm

4-4 Cost function . If (a+b)>1 ,, cost function is concave,( increasing return to scale); If (a+b)<1 ,, cost function is convex,( decreasing return to scale); AC C TC MC C q q C TC MC C AC q q Theory of he firm

4-4 Cost function . We showed that when cost is minimized ( to reach to an specified level of output) the production function should be concave, or the cost function should be convex to the origin, or the producer should be on the rising part of marginal cost curve. This is the second order condition for profit maximization. Min C=r1x1 + r2x2 + b S.t. f(x1,x2)=Q0 L=r1x1+r2x2 +b+μ[Q0– f(x1,x2)] F.O.C. ; (∂L/∂x1)= r1 - μf1=0 (∂L/∂x1)= r2– μf2 =0 (∂L/∂ μ)= Q0 - f(x1,x2)=0 Taking total differential we get; Theory of he firm

4-4 Cost function . μf11dx1 + μf12dx2 + f1dμ = dr1 μf21dx1 + μf22dx2 + f2dμ = dr2 f1dx1 + f2 dx2 =dq dμ = (1/D)[(f21f2– f12f1)dr1 + (f21f1- f11f2)dr2+ μΠdq] D=2f12f1f2 – f11f22 – f22f12 Π = f11f22– f122 dμ/dq = (μΠ)/D if dr1= dr2=0 strict concavity of production function ; D>0 , Π = f11f22– f122 >0 (dμ/dq )>0 , μ>0 , dc=r1dx1+r2dx2=μ (f1dx1+f2dx2) dq=f1dx1+f2dx2 dc/dq = MC = μ (dMC/dq) >0 P , MC MC p Π is maximized Π is minimized q q1 q2 Theory of he firm

4-4 Cost function . Long run cost function; In the long run there is no fixed cost. So b is variable in the short run cost function (C=r1x1 + r2x2 + b) . suppose that the parameter “b” shows the cost of buying and installing the machinery for establishing an specified size of plant. So , if k denotes the size of plant(the number of machinery by assumption) we should have b=g(k) . The production function , cost function , and expansion path in the long run is as follows; q=f(x1, x2 , k) C=r1x1 + r2x2 +g(k) h(x1, x2 , k) =0 from the above relations we could get long run cost as a function of output(q) and k(size of the plant). C=θ(q , k ) + g(k) Theory of he firm

4-4 Cost function . Assigning different k, we will get different cost schedules in the short run. If any size of plant is feasible, there will be a unique size of plant for each level of output which minimizes the cost of producing that level of output. The relation between output level and the optimum size of the plant which minimizes the cost could be obtained from the following relation; ∂C/ ∂k =0 ∂[θ(q , k ) + g(k)]/ ∂k =0 , k = Φ(q) substituting for k in terms of q in the family of cost schedules {C=θ(q , k ) + g(k)}, we will get the long run cost function ; LTC= F(q) . The graphical relation between the family of cost function in the short run and long run cost function is shown in the following figure; Theory of he firm

cost LTC Cost function STC3 STC2 STC1 q q1 q2 q3 SAC1 SMC3 SMC1 LAC LMC SAC2 SAC3 SMC2 q1 Theory of he firm q2 q3

Cost function and profit maximization in long run and short run SMC3 P,C LMC SMC1 p2 SAC1 LAC SAC3 SMC2 SAC2 P1 Q Q1 Q2 Q3 Theory of he firm

Joint product. x=h(q1 , q2) , or H(q1, q2,x)=0 , production relation x= single input , q1,q2 two outputs . when revenue is maximized(TR=p1q1+p2q2) subject to cost constraint(x=x0), or cost is minimized subject to a specific revenue, or profit is maximized, the above production relation should be strictly quasi-convex , which means a concave production possibility frontier. This means producing in the economic area, or producing efficiently on the production possibility frontier. If x=x0 , then q2 = f(q1 , x0) is the production possibility frontier dx= (∂h/∂q1)dq1 + (∂h/∂q2)dq2 = 0. slope of P.P.F.= RPTq1,q2 = - (dq2/dq1) = (∂h/∂q1)/(∂h/∂q2) = (h1/h2)=(∂x/∂q1)/(∂x/∂q2)= (MCq1/MCq2)=(MPq2/MPq1) Theory of he firm

q2 X=h(q1 , q2) q2 P.P.F. q1 RPT=h1/h2 P.P.F. q1 If x=h(q1 ,q2) is regularly strictly convex- d2q2/dq12 =(1/h23)(h11h22–2h12h1h2 +h22h12) >0 Theory of he firm

expansion path Constrained revenue maximization. q2 TR=p1q1 + p2q2 Iso-revenue Max TR=p1q1 + p2q2 S.T. x0=h(q1,q2) L=p1q1+p2q2 + μ(x0– h(q1,q2)) (∂L/ ∂q1)=p1- μh1=0, (∂L/ ∂q2)=p2- μh2 =0 (∂L/∂μ)= x0– h(q1,q2) μ=(p1/h1)=p1(∂q1/∂x)=VMPxq1 μ=(p2/h2)=p2(∂q2/∂x)= VMPxq2 VMPxq1=VMPxq2 (p1/p2)=(h1/h2)= (∂q2/∂x)/ (∂q1/∂x)=RPTq1,q2 -μh11 b -μh12 -h1 -μh21 -μh22 -h2 >0 ,=(1/h23)(h11h22–2h12h1h2 +h22h12)= - d2q2/dq12 >0 -h1 -h2 0 concave PPF, convex production relation, concave production function. H(q1,q2,x0)=0 p q2* -p1/p2 q1* Theory of he firm

q2 TR0=p1q1 + p2q2 Iso-revenue Constrained cost minimization. expansion path Minimize x=h(q1,q2) S.T. p1q1 + p2q2=R0 L = h(q1,q2) + μ(R0 – p1q1– p2q2) h1 – μp1=0 h2 – μp2=0 (R0 – p1q1– p2q2)=o (p1/p2)=(h1/h2)= (∂q2/∂x)/ (∂q1/∂x)=RPTq1,q2 μ=(p1/h1)=p1(∂q1/∂x)=VMPxq1 μ=(p2/h2)=p2(∂q2/∂x)= VMPxq2 VMPxq1=VMPxq2 each point on the expansion path (like point p) is the solution for both the constraint cost minimization and constraint revenue maximization if the PPF is concave. p q2* H(q1,q2,x)=0 q1 q1* Theory of he firm

Constraint profit maximization Max Π=p1q1 + p2q2– rx S.T. x=h(q1,q2) Π*= p1q1+p2q2– rh(q1,q2) ∂Π*/∂q1=p1– rh1 =0 ∂Π*/∂q2=p2– rh2 =0 (p1/p2)=(h1/h2)= (∂q2/∂x)/ (∂q1/∂x)=RPTq1,q2 r=(p1/h1)=p1(∂q1/∂x)=VMPxq1 r=(p2/h2)=p2(∂q2/∂x)= VMPxq2 VMPxq1=VMPxq2 = r -rh11 -rh12 -rh21 -rh22 >0 , -rh11<0 , r2(h11h22– h122)>0 , h22>0 Marginal cost of producing q1 and q2 should be rising, or marginal product of x in producing q1 and q2 should be falling . Concave PPF. Again production should occur in the economic area . The same familiar condition which should be held for optimum production in optimum behavior of the firm . Theory of he firm

Exercises Q4-1 ; construct the average and marginal production functions for x1 which correspond to the production function q=x1x2– 0.2x12– o.8x22. Let x2=10. At what respective values of x1 will the AP and MP of x1 equal zero. APx1=q/x1 = x2– 0.2x1– 0.8x22/x1 MPx1=∂q/∂x1 = x2– 0.4x1 X2=10, APx1=10 – 0.2x1 – 80/x1=0 , x1=10 , x1=40 x2=10, MPx1=10 – 0.4x1=0 , x1=25 Q4-2 ; determine the domain over which the production function q=100(x1+x2)+20x1x2-12.5(x12+x22) is increasing and strictly concave. f1=100+20x2-25x1>0, x2>(25x1-100)/20, x2>1.25x1 - 5 f2=100+20x1-25x2>0, x2<(100+20x1)/25, x2<4+ 0.8 x1 f11=f22= -25 , f12=f21=20 , f11f22– f122=(-25)(-25)-(-20)2=225>0 Theory of he firm

Exercises Q4-3 ; Derive an input expansion path over which the production function q=A(x1+1) a(x2+1) b , where a, b >0. max q=A(x1+1)a(x2+1)b s.t. C=r1x1 + r2x2 (MPx1/MPx2)=(r1/r2) , MPx1=aA(x1+1)a-1(x2+1)b MPx2=bA(x1+1)a(x2+1)b-1 , x2=(b/a) r(1+x1) – 1 , r=(r1/r2) Q4-4 ; Assume that an entrepreneur’s short-run total cost function is C=q3-10q2+17q+66. Determine the output level at which he maximizes profit if p=5.Compute the output elasticity of cost at this output. MC=3q2– 20q +17=5=p , q=6 , q=3/2 , (∂MC/∂q) =6q – 20 , if q=6 , (∂MC/∂q) =16>0 П= Max, if q=1.5, (∂MC/∂q) =-16<0 ε= (∂q/ ∂c)(c/q)=[1/(∂c/∂q)](c/q)=[1/(MC)](c/q)= [1/(3q2– 20q +17)][(q3-10q2+17q+66)/q] , if q=16 ε=0.8 Theory of he firm

Exercises Q4-5 ; A family of short run total cost curves is generated by C=0.04q3 – 0.9q2 +(10-lnk)q +8k2 , where k>1 denotes the plant size. Determine the firm’s long run total cost curve. (∂c/∂k)=-q/k + 16k =0 , k=[(q)1/2]/4 c=0.04q3–0.9q2 +[10-ln{(q)1/2/4}]q +16(q)1/2/4 Q4-6 ; An entrepreneur uses one input to produce two outputs subject to production relation x=A(q1a+q2b), where a,b>1. He buys the inputs and sells the output at fixed prices.Express his profit maximizing outputs as functions of the prices. Prove that his production relation is strictly convex for q1, q2 >0. Π=TR – TC =p1q1 +p2q2– rx=p1q1 +p2q2– rA(q1a+q2b) (∂Π/∂q1)= p1 - raq1a-1 = 0, q1=(p1/rAa)1/(a-1) q2= (p2/rAb)1/(b-1) (∂x/∂q1)=Aaq1a-1 , (∂x/∂q2)=A bq1b-1 , (∂2x/∂q12)=a(a-1)Aq1a-2 (∂2x/∂q22)=b(b-1)Aq2b-2 , (∂2x/∂q1∂q2)=0 (∂2x/∂q12) (∂2x/∂q22) - (∂2x/∂q1∂q2) =[A2ab(a-1)(b-1)q1a-2q2b-2]>0 Theory of he firm

Exercises Q4-7 An entrepreneur produces one outputs with two inputs using the production function q=Ax1ax21-a . He buys inputs and sells the output at fixed prices. He is subject to a quota which allows him to purchase no more than x10 units of x1 . He would have purchased more in the absence of quota. Determine the entrepreneur’s conditions for profit maximization. What is the optimal relation between the value of the marginal product of each input and it’s price? What is the optimal relation between the RTS and the input price ratio? Π = pq – r1x1– r2x2 +λ(x10– x1) Π = pAx1ax21-a – r1x1– r2x2 +λ(x10– x1) ∂Π/∂x1 = pAax1a-1x21-a–r1 - λ= pMPx1–r1 – λ=0 ∂Π/∂x2 = pA(1-a)x1ax2-a–r2=0=pMPx2–r2=0 RTSx1x2 =(MPx1/MPx2) =(r1 + λ)/r2 >r1/r2 Theory of he firm

x2 q1 q2 x20 x2 RTS = (r1+λ)/r2 r1x1+r2x2 x1 RTS= r1/r2 x10 x1 END OF CHAPTER 4 Theory of he firm