Download

1 / 19

190 likes | 213 Views

Learn about the major risks in retirement, including longevity risk, sequence of returns risk, LTC risk, market risk, and more. Discover strategies to protect your retirement savings and maximize your Social Security benefits.

E N D

Taking Control of Your Retirement 246 Bustleton Pike Feasterville-Trevose, PA 19053 Phone: 215-613-4999 Info@insshops.cpm www.InsShops.com

Retirement risks What are some of the major risks we face in retirement? • Longevity Risk • Sequence of returns risk • LTC risk • Market risk • Inflation risk • Loss of spouse risk • Public policy risk LIFE EXPECTANCY TABLES TODAY People are living longer today. For all of us this means our planning needs to take a longer view and prepare us for the next 25-35 years. What is today’s average life expectancy? Woman:81 Man: 76

What is sequence of returns risk The risk of receiving lower or negative returns early in a period when withdrawals are made from the underlying investments. The order or the sequence of investment returns is a primary concern for those individuals who are retired and living off the income and capital of their investments. It is not just long-term average returns that impact your financial wealth, but the timing of those returns. When retirees begin withdrawing money from their investments, the returns during the first few years can have a major impact on their wealth. Two retirees with identical wealth can have entirely different financial outcomes, depending on when they start retirement.

1. Understanding your money ( ) The market 3 Types of Stock Market Performance DOWN UP FLAT What the Experts Say! • Over time the Market outperforms everything • Safety through Diversification • Everyone loses Money sometimes

2. Retirement plan rules IRA In-service Distributions Important Ages 59 ½ Rule 70 ½ Rule

3. Qualified retirement plan issues Hidden Fees Extreme Volatility Variable Annuities Examples of Commonly used Retirement Investment Problems Please understand before you buy

4. A possible solution What if you could purchase an Insurance Product that credits interest based on a Stock market-linked index and when the stock market – linked index goes up, you have the opportunity to be credited more interest; but when the stock market-linked index goes down, you don’t lose any of your principal? Why do you have insurance for your HOME, CAR, HEALTH and even your LIFE If this type of insurance product was available, wouldn’t you want to know about it? PROTECTION Fixed Index Annuities are not a direct investment in the stock market. They are long-term insurance products with guarantees backed by the issuing company. They provide the potential for interest to be credited based in part on the performance of specific indices, without the risk of loss of premium due to market downturns or fluctuation.

5. Fixed index annuities Who offers them? Each Fixed Index Annuity is different There are Two Catches: • Time 10% • CAP NO FEES Be Careful – Some may be better for you than others. WHAT’S A FIDUCIARY ROLE?

6. Retirement income strategies Create an Income Floor with Guaranteed Income You cannot outlive* The Probability based approach (systematic withdrawal method) Safe withdrawal rate: was 4% now 2.8% Annuity (noun) “a payment of a fixed sum of money at regular intervals of time, especially yearly.” Social Security (Annuity) Pensions (Annuity) Paychecks for life ( Guaranteed income annuity) *Guaranteed income is only possible through the use of an annuity with guaranteed income rider. All annuity guarantees are backed soley by the financial strength and claims-paying ability of the issuance company.

7.SOCIAL SECURITY MAXIMIZATION Social Security Benefit Increase & Decrease based on Claiming Age 8% 70% 1 year For every year you delay claiming Social Security, how much larger is the benefit? How much larger will your Social Security benefit be if you claim at 70 instead of 62? If you change your mind after claiming, how long do you have to revert it? Taxation of Your Social Security 85% How much of your Social Security benefit could be subject to taxation? Social Security Claiming & Taxation Strategies These case studies are hypothetical. You should make your own decisions in light of your financial situation. CASE STUDY #1 For one Client, a proper asset positioning and withdrawal strategy provided an additional $140,000 due to reduced taxation of Social Security Benefits. CASE STUDY #2 For one married couple, with a life expectancy to age 90, by optimizing their Social Security claiming decision they will see an additional $300,000 in benefits during their lifetimes.

8.Inflation risk Inflation is the rate at which the general level of prices for goods and services is rising and, consequently, the purchasing power of your dollars is diminishing. Let’s look at some common household expenses and purchases: How many times in the last 7 years has there been No Cost of Living increase in our Social Security Benefits? 3 years

9. Long-term care risk After age 65, what percent of us will need some form of long-term care? 72% Average amount of time we’ll need care: Man:2.9 years Woman:3.9 Average cost of long-term care: Home Health care: $50,000 a year Assisted Living: $60,000 a year Nursing Home: $120,000 a year

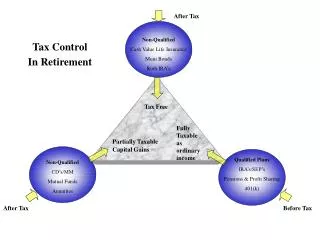

10.Public policy risk Eliminating & Reducing Taxation of Retirement Benefits Your assets and income fall in 3 general buckets: Taxable Tax Deferred Tax Exempt

Do you want what we do? Every client is unique. We are happy to help you or for those who want a holistic approach, we would help you create a Retirement Prosperity Roadmap to optimize all aspects of your retirement. • Protection of Principal from Market Declines • Retirement Income Planning • Income for Life • Long- Term Care solutions • Social Security Maximization • Tax Efficiency Strategies • Life Insurance Review • Estate Planning/Estate Tax Minimization • Active Money management THAT’S WHAT WE DO!

Medicare Myths Myth 1: As soon as you turn 65, you must apply for Medicare Myth 2: If you have a job, you don’t have to apply for Medicare Myth 3: If you are on COBRA, you don’t have to apply for Medicare you turn 65, just as long as you can stay on COBRA. Myth 4: All Medicare supplements come with a drug plan. Myth 5: Only people who are 65 are allowed to be on Medicare Myth 6: If you’re employed in a group with 20 or more employees, you have to come off the group plan. Myth 7: if you are employed by a company with less than 20 employees, you don’t have to come off the group plan. Myth 8: If I do NOT apply for Medicare when I turn 65. I will have to pay a penalty when I eventually do apply. Myth 9: Once I have enrolled into Medicare, I must always keep Medicare. Myth 10: Everyone is entitled to receive Medicare Part A, at NO cost, Once they turn 65 Myth 11: Everyone pays the same amount for Medicare Part B and Medicare Part D (Rx prescription plan).