Download

1 / 15

160 likes | 339 Views

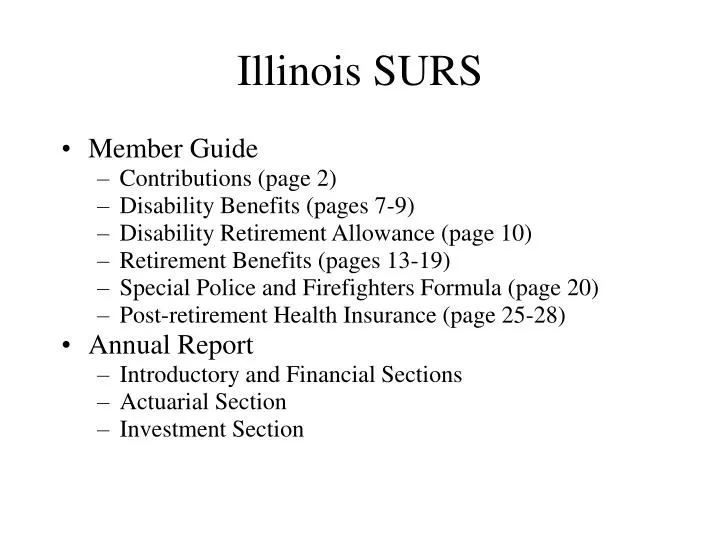

Illinois SURS. Member Guide Contributions (page 2) Disability Benefits (pages 7-9) Disability Retirement Allowance (page 10) Retirement Benefits (pages 13-19) Special Police and Firefighters Formula (page 20) Post-retirement Health Insurance (page 25-28) Annual Report

E N D

Illinois SURS • Member Guide • Contributions (page 2) • Disability Benefits (pages 7-9) • Disability Retirement Allowance (page 10) • Retirement Benefits (pages 13-19) • Special Police and Firefighters Formula (page 20) • Post-retirement Health Insurance (page 25-28) • Annual Report • Introductory and Financial Sections • Actuarial Section • Investment Section

Member GuideContributions • Employee Contributions 6.5% Normal Retirement Benefit 0.5% Automatic Annual Increases 1.0% Survivors’ Insurance 8.0% Total Employee Contribution • Employer Contributions 9.1% Average (1.4 x 6.5%)

Member GuideDisability Benefits • Definition - unable to perform your job • 60 day waiting period (or accumulated sick leave if longer) • Benefit is greater of: • 50% of basic compensation on day you were disabled • 50% of average earnings for 24 months prior • Benefits stop on the earliest of: • Disability benefit payments equal 50% of your total earnings • Sept. 1 of year following your 70th birthday (or 5 years if disabled after 65) • No longer disabled, retirement, or death

Example – Disability Benefits • 28 year old employee • Began work on 1/1/99 • Disabled from an accident on 12/31/00 • Earnings : 1999 $25,000 2000 $30,000 ($2500/month) • Disability benefit of $1250/month starting after 60 days • Payable for 22 months ((1/2)(25,000+30,000)/1250)

Member GuideDisability Retirement Allowance • Definition - totally disabled and unable to perform any substantially gainful employment • Amount - 35% of basic compensation

Retirement Benefits • General Formula (based on average monthly earnings) • 2.2% per year of service • Maximum benefit is 75-80%, depending on starting date and age at retirement

Retirement BenefitsEarly Retirement • General formula benefit is reduced 0.5% for each full month under age 60 at retirement • Avoiding the Early Retirement Reduction • Employee contribution 7% per year under 60 • Employer contribution 20% per year under 60 • No Early Retirement Reduction if you have 32 or more years of service (in 2000)

Example – Retirement Benefit • Employee retires at age 58 with 27 years of service • Final average earnings of $50,000 • Highest annual salary in FAE = $52,000 • Retirement benefit $26,135 (.5227x50,000) • Employee payment for Early Retirement Option $7,280 (.14x52,000) • Retirement benefit without discount $29,700 (.594x50,000) • One time payment of $7,280 provides annual benefit of $2,565

Retirement BenefitsMoney Purchase Formula • Start with contributions and interest in your account • Multiply by 6.5 and divide by 8.0 (to get retirement component) • Multiply by 2.4 (to include employer contribution) to get the money purchase value • Money purchase value is divided by actuarial factor (based on age at retirement – see page 18) to get the monthly retirement benefit

Example – Money Purchase Formula • Same employee as before, but amount of contributions and interest in account is $150,000 • Money purchase value is (150,000x6.5/8.0)x2.4=292,500 • Monthly benefit is 292,500/119.761=2,442.36 • Annual benefit is $29,308.32

Retirement BenefitsPolice and Fire Fighters • Employee contributions 9.5% • Retirement benefits paid in full • at 50 with 25 years of service • at 55 with 20 years of service • Formula • 2.25% per year for first 10 years of service • 2.50% per year of next 10 years of service • 2.75% per year of next 10 years of service • Maximum = 80%

Post-retirement Health Insurance • Any retiree with 5 or more years of service is eligible to participate • State of Illinois pays entire cost of coverage for anyone with 20 or more years of qualified service • For those with fewer than 20 years of service, State pays 5% of cost per year of qualified service

SURS Comprehensive Annual Financial ReportIntroductory and Financial Sections • Public Act 88-0593 (effective 7/1/95) • Funding appropriation for SURS • Public Act 90-448 (effective 1/1/98) • Alternative benefit programs • Funding Status • 1996 68.5% • 1998 85.8% • 1999 85.3%

Actuarial Section • Letter of certification • Valuation results • Unfunded liability of $1.9 billion (6/30/99) • Actuarial assumptions • Mortality Retirement age • Interest Assets • Termination Expenses • Salary increases Spouse’s age

Investment Section • Investment summary • Policy • Objectives • Strategies • Investment results