Download

1 / 115

1.15k likes | 1.17k Views

Explore the concept of market equilibrium and the interaction between consumer demand and firm supply. Learn about the price of goods, the role of governments in economics, and the effects of supply and demand changes on market equilibrium. Also, discover the principles and characteristics of Islamic economics, as well as the free market system.

E N D

Chapter 2 Demand Supply &2015 Market Equilibrium Prof. Dr. Mohamed I. Migdad Professor of Economics

Chapter 2 content: • 2.1 Introduction • 2.2 What Is the Market? • 2.3 Consumer Demand • 2.4 Firms Supply • 2.5 Equilibrium between Supply and Demand • 2.6 Price of Goods and Price Theory • 2.7 Role of Governments in Economics • 2.8 Effects of Supply and Demand Change on Market Equilibrium

What is the cynic? • A man who knows the price of everything and the value of nothing Oscar Wilde

Market • Market is the word we use daily, and simply is the place we go to purchase different goods and services. • It contains system, institutions, procedures, social relation, infrastructure, where parties engage in exchange. • It could be said that market is the process in which the prices of goods and services are established.

Notes 1. It is not necessary for a market to be connected with a fiscal place. It economically could mean purchasing or selling over tel. or online. 2. There is no specific market for all goods and services, each product is demanded and supplied in its special market.

Market definition • A market is the institution through which buyers and sellers interact and engage in exchange. • A market economy has at its heart the actions of buyers and sellers who exchange goods and services with one another.

Definition • A market at its economic terms is a group of sellers and buyers desiring exchange of goods or services.

How markets work • Buyers and sellers receive signals from one another in the form of prices. • If buyers want to buy more of a good, prices rise and sellers respond by supplying more to the marketplace.

Markets • If buyers want to buy less of a good, prices fall and sellers respond by supplying less to the marketplace.

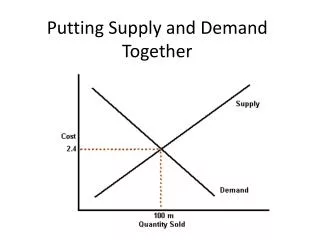

Markets • Market equilibrium occurs when the price is such that the quantity that buyers are interested in purchasing is equal to the quantity that sellers are interested in supplying to the market.

Markets • The market mechanism allows an economy to simultaneously solve the three economic problems of what, how, and for whom.

Who control the market? • There is no higher authority that directs the behavior of these economic agents; rather, it is the invisible handof the marketplace that allocates final goods and services, as well as factors of production.

Economic problem • The economic problem: Given scarce resources, how, exactly, do large, complex societies go about answering the three basic economic questions? • To answer the three basic questions we need to study the economic systems.

Economic Systems • Economic systems are the basic arrangements made by societies to solve the economic problem. • They includes four systems:

Systems • Islamic economy • Laissez-faire economies • Command economies • Mixed systems

Islamic Economy • Some people think that Islam has no economic system of its own • Islamic Economics is as Old as Islam Itself

Islamic Economy • Islamiceconomicsis accordance withIslamic law. • Islamic economics can refer to the application of Islamic law to economic activity either where Islamic rule is in force or where it is not;

I.E • i.e. it can refer to the creation of an Islamic economic system, or to simply following Islamic law in regards to spending, saving, investing, giving, etc. where the state does not follow Islamic law.

Definition of Islamic economics • The Islamic economics is both a science and an art which deals with the daily routine of a Muslim's economic life. • i.e. how he earns his income and how he spends it. It is a science in the sense that it involves many scientific methods in the production of material goods, their distribution and consumption.

Principles • The Islamic economic system is directly guided by Allah Almighty Himself. • all important aspects of the Islamic economic system and the applicable norms are thoroughly discussed in the Holy Quran

Cont. • Allah created all needed provisions so that they may consume them and may satisfy their wants

Other principles • All wealth belongs to Allah (SWT( • The Muslims are the custodians and trustees of the wealth. • Hoarding the wealth is forbidden. • Circulating the wealth is obligatory

المبادئ بالعربية • كل الثروة مملوكة وترجع إلى الله تعالى • المسلمون هم الحراس والأمناء على الثروة والمال • اكتناز الثروات ممنوع • تعميم وتدوير هذه الثروة واجب

The free market system • In a laissez-faire economy,individuals and firms pursue their own self-interests without any central direction or regulation. • The central institution of a laissez-faire economy is the free-market system. • A market is the institution through which buyers and sellers interact and engage in exchange.

Consumer sovereignty • Consumer sovereignty is the idea that consumers ultimately dictate what will be produced (or not produced) by choosing what to purchase (and what not to purchase).

Free enterprise • Free enterprise: under a free market system, individual producers must figure out how to plan, organize, and coordinate the production of products and services.

distribution of output • In a laissez-faire economy, the distribution of output is also determined in a decentralized way. The amount that any one household gets depends on its income and wealth.

Free System • The basic coordinating mechanism in a free market system is price. Price is the amount that a product sells for per unit. It reflects what society is willing to pay.

Command economies • In a command economy, a central government either directly or indirectly sets output targets, incomes, and prices. • And the government determine what to produce and how much and How and for Whom to produce.

Mixed Systems, Markets, and Governments Since markets are not perfect, governments intervene and often play a major role in the economy. Some of the goals of government are to:

goals of government in mixed economy • Minimize market inefficiencies • Provide public goods • Redistribute income • Stabilize the macro economy: • Promote low levels of unemployment • Promote low levels of inflation

The Market System Relies on Supply and Demand to Solve the Trio of Economic Problems

Demand in Product or Output Markets • A household’s decision about the quantity of a particular output to demand depends on:

What is demand: • Demand is the desire to own any thing with an ability and willingness to pay. • It includes the ability and willingness to bay a commodity at a given period and price. • The effective demand is the demand which combines with the ability and willingness to bay in a particular period of time.

The demand curve • The demand curve is a graph illustrating how much of a given product a household would be willing to buy at different prices.

Demand depends on: • The price of the product in question. • The income available to the household. • The household’s amount of accumulated wealth. • The prices of other products (substitutes and complements) available to the household.

Demand depends on: • The household’s tastes and preferences. • The household’s expectations about future income, wealth, and prices.

Quantity demanded • Quantity demanded is the amount (number of units) of a product that a household would buy in a given time period if it could buy all it wanted at the current market price.

Changes in Quantity Demanded Versus Changes in Demand • The most important relationship in individual markets is that between market price and quantity demanded.

continue • We use the ceteris paribus or “all else equal” device, to examine the relationship between the quantity demanded of a good per period of time and the price of that good, while holding income, wealth, other prices, tastes, and expectations constant.

continue • Changes in price affect the quantity demanded per period. • Changes in income, wealth, other prices, tastes, or expectations affect demand.

The demand curve • The demand curve is a graph illustrating how much of a given product a household would be willing to buy at different prices.

law of demand • The law of demand states that there is a negative, or inverse, relationship between price and the quantity of a good demanded and its price.