Download

1 / 39

390 likes | 414 Views

Understand legal and regulatory frameworks, treasury management codes, and investment strategies for effective financial control and risk management. Learn about debt management, cash flows, and optimizing performance while complying with CIPFA TM Code and Prudential Code. Presented by David Chefneux, dive into key principles, practices, and strategies for treasury risk management, decision-making, and reporting requirements. Enhance your knowledge of financial markets, investments, and money market transactions to achieve value for money and maintain public funds. Stay updated with annual reports, strategies, and prudential indicators in this comprehensive introduction to treasury management.

E N D

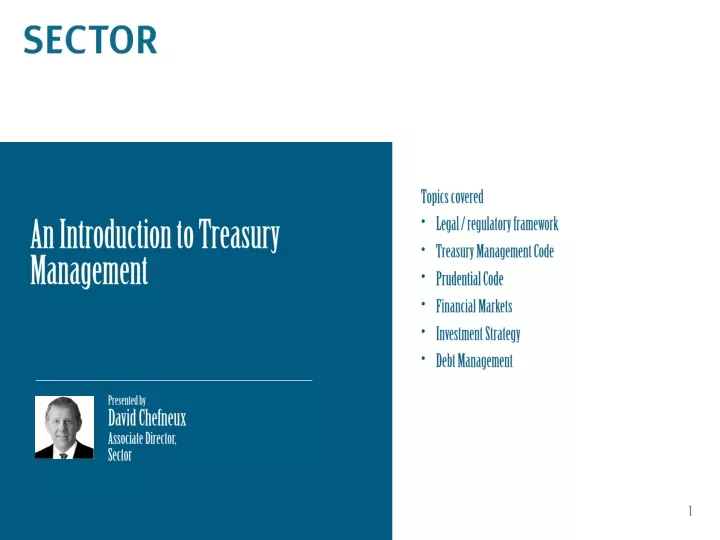

Topics covered • Legal / regulatory framework • Treasury Management Code • Prudential Code • Financial Markets • Investment Strategy • Debt Management An Introduction to Treasury Management Presented by David ChefneuxAssociate Director, Sector

Treasury Management – as per CIPFA TM Code of Practice • The management of the organisation’s:- • Investments • Cash flows • Banking • Money market and capital market transactions • Effective control of risks associated with those activities • Pursuit of optimum performance consistent with those risk 2

Local Government Acts • Local Government Investments (Scotland) Regulations 2010 • Authorities may only invest with the consent of Scottish ministers • Must have regard to TM Code & Prudential Code 3

Finance Circular 5/2010 (1) • Consent of Scottish Ministers for local authorities to invest money • Must comply with conditions set out in this circular • Investment properties included in LA portfolio of investments • Any loan to third party is an investment – except loans to another authority forming part of the Common Good under s.40 2003 Act • Have regard to TM Code of Practice and Prudential Code • Only make investments defined as permitted investments • Identify which investments permitted in the coming financial year • Limits for amount that may be invested in each type of permitted investment • State objective of each type of investment 4

Finance Circular 5/2010 (2) • Identify risks for each type of investment • Annual Investment Strategy for each year –approved by full board or Council before the start of each financial year • Recommend Investment strategy part of wider TM strategy • Max value and period for investments • Must not borrow more in advance of needs to make a profit • Policy for borrowing in advance of need and justification for any taken • Annual Investment Report within 6 months of end of year 5

CIPFA Treasury Management Code • Why? • High profile losses of investments with banks that defaulted in 1990s • Breakdown of confidence between City financial institutions and local authorities • Inappropriate increase in risk exposure • Maintain high and consistent standards in looking after public funds and debt • Large cash balances held by local authorities and new investment instruments 6

CIPFA Treasury Management Code – three key principles • Formal and comprehensive objectives, policies, practices, strategies, & reporting arrangements for effective management and control of TM activities • Control of risk: security, liquidity, yield • Value for money within context of effective risk management 7

CIPFA Treasury Management Code – Clause 1Treasury Management Practices • Working documents for officers • How policies and objectives in the Treasury Management Policy Statement will be achieved • How it will manage and control those activities • Do not have to be formally approved by Council but subject to scrutiny 8

CIPFA Treasury Management Code – Treasury Management Practices TMP1 - Treasury risk management TMP2 - Performance measurement TMP3 - Decision making and analysis TMP4 – Approved instruments, methods and techniques TMP5 – Organisation, clarity and segregation of responsibilities and dealing arrangements 9

CIPFA Treasury Management Code – Treasury Management Practices TMP6 – Reporting requirements and management information arrangements TMP7 – Budgeting, accounting and audit arrangements TMP8 – Cash and cash flow management TMP9 – Money laundering TMP10 – Training & qualifications TMP11 – Use of external service providers TMP12 – Corporate governance 10

Annual report Mid-year review Annual strategy and plan Before the start of the year Mid-year (minimum) After year end CIPFA Treasury Management Code – Clause 2: Reporting requirements To go to full Council – can be scrutinised by committee beforehand Also regular monitoring reports to executive and scrutiny committee 11

Affordable capital expenditure plans External borrowing and liabilities within prudent and sustainable levels TM decisions in accordance with good practice Prudential Code: Objectives • Achieved by: • Strategic planning – service priorities and objectives • Asset management planning – whole of life costs • Option appraisal – individual projects • Practicality – is plan achievable and realistic? 12

Prudential Code: Indicators • To be set before start of year • Reviewed at end of year • Revised as required – following correct process • Set for the coming year and following 2 years • Approved by same process as budget 13

International data / events Key UK data / events Inflation Target (2.0%) Monetary Policy Committee (MPC) Bank Rate (0.5%) What drives the Financial Markets/Interest rates? 16

What affects Money Market Yields? Short Term Rates: Overnight 1 month 2 months 3 months 4 months 6 months 9 months 12 months Supply / Demand High Expectation of the Bank Rate Forecast of the future direction of Bank Rate Low 17

What affects Gilt (Bond) yields? 1 year 2 years 3 years 4 years 5 years 5-10 years 10-20 years 20-30 years 30-40 years 40-50 years Expectation of Bank Rate Combination of Bank Rate expectations and Inflation • Inflation expectations • Government’s policy and future funding requirements • Institutional demand (e.g. Pension Fund liability matching req) Low 18

Bank of England Forecasts February 2012 19

Remember Types of risk • Security • Liquidity • Yield • Counterparty • Market / interest rate • Liquidity 23

Counterparty Risk • Credit ratings – Bank and Sovereign • Credit Default Swaps • Equities • Market Rates • Market analysis and information 24

Credit Ratings • What is a credit rating? • Independent assessment of an organisation • Likelihood of getting money back • Statement of opinion • Risk associated with investments in a counterparty 25

Credit Ratings • Who provides credit ratings? • Fitch • Moody’s • Standard & Poor’s (S&P) • Who uses credit ratings • Local authorities • Other non-financial institutions • Financial institutions • Professional bodies • Central banks 26

Credit Ratings • Credit rating categories • Short term (Fitch, Moody’s, S&P) • Long term (Fitch, Moody’s, S&P) • Viability (Fitch) / Financial Strength (Moody’s) • Support (Fitch) 27

Credit Ratings • Investment Grade (Short term, Long term) • Fitch: F3, BBB • Moody’s: P-3, Baa • S&P: A-3, BBB 28

Rating change indicators Credit Ratings • Rating Outlook • Positive • Stable • Negative • Rating Watch • Positive • Negative 29

Credit Default Swaps (CDS) • Description • Market indicator of risk associated with a counterparty • How can they be used? • Part of Annual Investment Strategy • Day-to-day decision making • Considerations • Speculation • Trends 30

Counterparty Risk Summary • Credit ratings are an opinion, no guarantee • Assess all information available • Ratings • Rating Outlooks / Watches • CDS • Equities • Get a number of quotes • Market rates • Evaluate relative “value” of investment rate 31

Security Liquidity Yield Risk Management Considerations Manage counterparty risk Check your liquidity requirements Set realistic target rates and understand the relative risk associated with each investment If in doubt, ask! 32

Investment Instruments • DMADF (Debt Management Agency Deposit Facility) • Treasury Bills • Money Market Funds • Government Liquidity Funds • Fixed Term Deposits • Call/Notice Accounts 33

Diversification Spread of risk - ‘not having all your eggs in one basket’ Interest rate views Counterparty exposure and limits Asset classes 34

Borrowing from PWLB • PWLB rates are set twice dailyThey lend up to: • 10 years variable rate (Maturity & EIP only) for 1, 3 or 6 month rollovers • 50 years fixed rate • Minimum period of a new loan is 1 year (Maturity debt) and 2 years for Annuity and EIP debt • Fixed rates are based on a margin above Gilt yields (per Section 5 of the National Loans Act 1968) 37

External borrowing – other considerations • Does the Authority have any other debt portfolio objectives? • Are there urgent short term budgetary pressures to find savings? • Is the average rate of interest on the existing debt portfolio viewed as being too high? Is it out of line with peer authorities? • Is the existing maturity profile of the debt skewed in a way that needs remedial action? 38