Download

1 / 26

260 likes | 395 Views

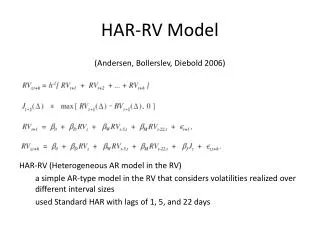

HAR-RV with Sector Variance. Sharon Lee April 1, 2009. HAR-RV Model. HAR-RV makes use of average realized variance over daily, weekly, and monthly periods. h=1 corresponds to daily periods, h=5 corresponds to weekly periods, h=22 corresponds to monthly periods

E N D

HAR-RV with Sector Variance Sharon Lee April 1, 2009

HAR-RV Model • HAR-RV makes use of average realized variance over daily, weekly, and monthly periods. • h=1 corresponds to daily periods, h=5 corresponds to weekly periods, h=22 corresponds to monthly periods • These time horizons correspond to day-ahead, 5-day ahead, and month-ahead predictions of average realized variance.

Sectors • Consumer Goods • Healthcare • Financial • Technology • Basic Materials • Industrials • Utilities • Conglomerates • Services • Stocks with less than 2000 observations were removed

HAR-RV Models • 1) Single stock on stock’s regressors • 2) Single stock on stock’s regressors and its sector’s regressors • 3) Single stock on stock’s regressors, sector’s regressors, and market’s regressors

Consumer Goods Sector Model Fits

Healthcare Model Fits

Financial Model Fits

Technology Model Fits

Basic Materials Model Fits

Conglomerates Model Fits

Industrial Model Fits

Services Model Fits

Utilities Model Fits

Utilities Model Fits

next • Explanations for market variables • R-squared patterns among sectors • Incorporate risk factors • Further analysis