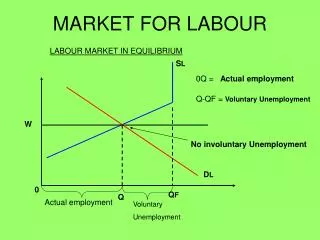

Download

1 / 14

140 likes | 253 Views

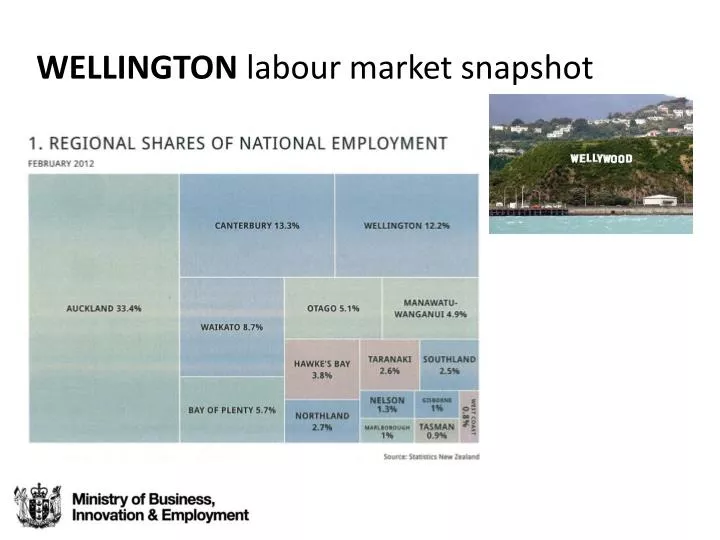

WELLINGTON labour market snapshot. Employment. 269,000 people employed end Dec 2012 (rate 65.6%) Wellington tanked post recession. Slow since March 2010. Canterbury and Auckland tanked earlier, but recovered more rapidly, until February 2011.

E N D

Employment • 269,000 people employed end Dec 2012 (rate 65.6%) • Wellington tanked post recession. Slow since March 2010. • Canterbury and Auckland tanked earlier, but recovered more rapidly, until February 2011. • Now Auckland has weakened but still growing, and Canterbury is stepping up.

Incomes • Wellington has high average annual household incomes • But employment growth in filled jobs has been below average (and below other urban regions)

Vacancies • Canterbury vacancies have been higher, esp. since the Feb 11 quake • Auckland and Wellington vacancy levels are similar (flat)

Participation • High participation – 70.3% vs 68.2% nationally (only Southland higher) • Larger proportion of population in the working ages (15-64)

Unemployment • Wellington now matches the national rate (6.9%) • Has generally been more resilient during recessions

Industry 2012 • Strongest in professional, scientific and technical services, and in public administration and safety • Weaker in manufacturing, and agriculture, forestry and fishing.

Skills • Wellington and Auckland both highly skilled, with less emphasis on skilled and elementary occupations, but also with a higher than average share of semi-skilled • Highly skilled: managers and professional occupations • Skilled: technicians and trades workers • Semi-skilled: clerks, services and sales workers, agriculture and forestry workers • Elementary: machinery operators and assemblers, general labourers

Forecasts Source: MBIE Short-term Employment Prospects: December 2012 (March years) • Forecasts vary continuously, but can be usefully examined to see the basic trends and how the various components relate • 2013 employment growth to March is now forecast to be -0.7%, GDP 2.3%* • Labour productivity has been growing, as GDP does quite well, while employment growth has been slow

Employment growth by industry forecast Source: MBIE Short-term Employment Prospects: December 2012 (March years) * incl. Communication Services; Finance and Insurance; Property and Business Services; Professional , Scientific and Technical Services;

Employment growth by skills forecast Source: MBIE Short-term Employment Prospects: December 2012 (March years) • Strongest growth in skilled, highly skilled, and elementary level occupations, reflecting the Canterbury rebuild and the strong growth in construction • Both skilled and elementary play a smaller than national average role in Wellington’s labour market

Employment growth by industry forecast - WN Source: MBIE Short-term Employment Prospects: December 2012 (March years) * incl. Communication Services; Finance and Insurance; Property and Business Services; Professional , Scientific and Technical Services;

Challenges/Opportunities • Diversifying Wellington’s industry mix • Internationalising Wellington’s professional business service firms (which are currently focussed on government) • Continuing to improve tourism takings and better leveraging visitor attractions to attract talent and investment • Commercialising science and research development