Download

1 / 20

200 likes | 363 Views

Money in the Competitive Equilibrium Model Part 1. Ad-Hoc Money Demand in CE Model Hyperinflation Dynamics. How can we incorporate money demand into the competitive equilibrium model? How will the quantity of money affect real variables, prices, and inflation?

E N D

Money in the Competitive Equilibrium ModelPart 1 Ad-Hoc Money Demand in CE Model Hyperinflation Dynamics

How can we incorporate money demand into the competitive equilibrium model? • How will the quantity of money affect real variables, prices, and inflation? • What are the implications for monetary policy?

Two Approaches for adding money in CE model: (i) Ad-Hoc (exogenous) money demand. (ii) Explicit Money Demand as a choice variable for households. (Search Model / Shortcuts)

Ad-Hoc Money Demand • Money Demand Function: where Ly > 0, LR < 0 and R = r + pe • Money Market Equilibrium: y = y* and r = r* from CE model or

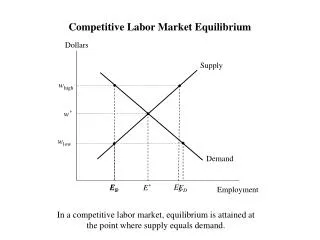

The ad-hoc money demand function can be “added” onto the CE model. Money market only determines prices: CE Model y*, r*, c*, N*, w* Money Market P* (arrows flow one way only!)

A competitive equilibrium in a two-period model with production is and for t = 1,2 solving: (1 eq) (2 eq) (2 eq) (4 eq) (1 eq)

Equilibrium Prices: dP/dy* < 0 and dP/dr* > 0 • Productivity Shocks (z) Temp: dy*/dz > 0, dr*/dz < 0 dP/dz < 0 Perm: dy*/dz > 0, dr*/dz = 0 dP/dz < 0

Neutrality of Money: dP/P = dM/M inflation rate (p) = money growth (m) • Classical Dichotomy: Real variables are independent from nominal variables (P,M) y*, r*, c*, N*, w* Money Market P* (arrows flow one way only!)

Inflation Dynamics • Historically many countries around the world have experienced hyperinflaiton. (1) Hyperinflation in 1980s Israel – 370% Argentina – 1,100% Bolivia – 8000% • German Hyperinflation (1/22 – 12/23, 4000%) Daily Newspaper Price $0.30 (1/21) $1,000,000 (10/23) $7,000,000 (11/23)

Cagan (1956) asks: (i) Is there a systematic process by which inflation expectations are formed? (ii) How did inflation expectations contribute to hyperinflations? • Note from money market clearing: dP/dpe > 0 • Cagan (log) Money Demand Function:

Where g is constant (related to y*, r*) and a > 0 measures the sensitivity (elasticity) of MD to pe. • Money Market-Clearing or (1) • Adaptive Expectation (2) 0 < l < 1 represents the speed of adjustment.

Estimation - Solve for pte from (1), lag it to get pt-1e - Substitute into (2) and then plug (2) into (1) (3) Country pa l Germany 322 5.46 0.20 Russia 57 3.06 0.35

Stability Substitute pt-1 = pt – pt-1 into (3) and re-arrange: If mt – mt-1 =m constant, then

pt is stable (non-explosive) if or al < 1-l < 1. • A sufficient condition for hyperinflation: al > 1 • Germany: al = 1.09 > 1 Russia: al = 1.07 > 1

Intuition: • Expected inflation adapts faster to actual inflation (high l) and the more sensitive MD is to expected inflation (high a) hyperinflation more likely.

Rational Expectations • Cagan Model with rational expectations: • Money Market Equilibrium: • Fed Money Supply Rule: where m are constants and e is a random money demand shock created by the Fed.

Implications (i) Current pt depends upon current and future money supplies mt. (ii) The impact of a shock to the money supply (e) depends upon whether it’s temporary or permanent. * m1small temp small effect on pt * m1 close to 1 perm large effect on pt

Nominal versus Real Quantities: Real = Nominal/P Interest Rates: (exact) or r = R – p (approx) where R = nominal rate r = real rate inflation rate =