Download

1 / 11

130 likes | 169 Views

Learn about arbitrage opportunities, zero-investment portfolios, APT, diversification, and comparing APT with CAPM. Discover how multifactor models work and their relevance in risk management and portfolio optimization.

E N D

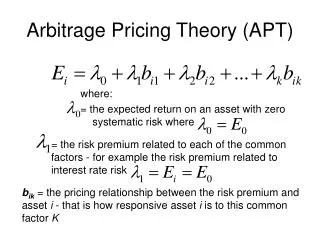

Arbitrage Pricing Theoryand Multifactor Models Arbitrage Opportunity and Profit Diversification and APT APT and CAPM Comparison Multifactor Models

Arbitrage Opportunity and Profit • Arbitrage • The opportunity of making riskless profit by exploiting relative mispricing of securities • E.g., IBM: $96 on NYSE and $96.15 on NASDAQ creates an arbitrage opportunity • Zero-Investment Portfolio • A portfolio of zero value by long and short the same amount of securities • E.g., Buy $10,000 of stock A and short $10,000 of stock B creates a zero-investment portfolio

Arbitrage Opportunity and Profit • Example: Two stocks A, B and a bond C. • If it rains tomorrow, A pays $1.3 and B pays $0.2 • if it does not rain, A pays $0.3 and B pays $1.5 • C pays $2 regardless. • Price today: PA = PB = $1, PC= $2 • Find the arbitrage opportunity and profit from it • Solution • Short 1 share of A and B each to get $2 • Use the proceeds to buy bond C • Total initial investment = $0 • P/L = $0.5 if it rains, and P/L = $0.2 if it does not.

Diversification and APT • Well-diversified Portfolio • A portfolio sufficiently diversified such that non-systematic risk is negligible • Arbitrage Pricing Theory (APT) • A theory of risk-return relationships derived from no-arbitrage conditions in large capital market • Individual stock: • Well-diversified portfolio: RF is the factor return • No-arbitrage means: αP = 0

Diversification and APT • How does it work? • Factor portfolio: • If portfolio C has αP = 2%, βP = 0.5 • Show me the money • Short $100 of the factor portfolio • Long $200 of portfolio C • Net payoff • Risk-free four bucks? I’ll take it anytime!

APT and CAPM Comparison • APT applies to well-diversified portfolios and not necessarily to individual stocks • It is possible for some individual stocks not to lie on the SML • APT is more general in that its factor does not have to be the market portfolio • Both models can be extended to multifactor setup

Multifactor Models • Possible to consider more than one benchmark factor! • Consider a two-factor model: • Ri: excess return = ri – rf • RMi: factor portfolios excess return = rMi – rf • : return sensitivity to systematic factors - also called as “factor loadings” “factor betas”

Multifactor Models • Where do the factors come from? • Variables that reflect macroeconomic picture • E.g. industrial production, inflation, bond spreads • Variables that serve as proxies for exposure to systematic risk • E.g. Fama-French (1993) model approach

Fama-French (1993) Model • Three-factor model: • Ri: stock excess return = ri – rf • RM: market excess return = rM – rf • SMB: “Small Minus Big” factor return SMB =1/3 (Small Value + Small Neutral + Small Growth)- 1/3 (Big Value + Big Neutral + Big Growth) • HML: “High Minus Low” factor return HML =1/2 (Small Value + Big Value)- 1/2 (Small Growth + Big Growth) • : return sensitivity to factors

Wrap-up • What is arbitrage and how to do it? • What are the major differences between APT and CAPM? • Multifactor models – the way to go!