Download

1 / 28

280 likes | 540 Views

International Bond Market Conference 2009 Strategies for Prospering Primary and Secondary Bond Markets 債券發行市場與交易市場相輔相成之發展策略. November 2009. Impact to Credit Markets. Outline. What Is the Current Status of Crisis? What Is the Global Bond Market Status? What Is the Taiwan Bond Market Status?

E N D

International Bond Market Conference 2009Strategies for Prospering Primary and Secondary Bond Markets債券發行市場與交易市場相輔相成之發展策略 November 2009

Outline What Is the Current Status of Crisis? What Is the Global Bond Market Status? What Is the Taiwan Bond Market Status? Discussion and Q/A

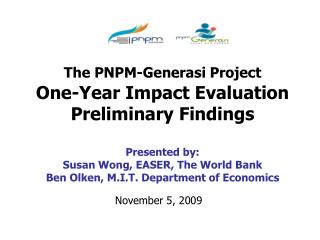

Writedowns & Credit Losses vs. Capital Raised (as of August 25 2009) Billion USD Source: Bloomberg

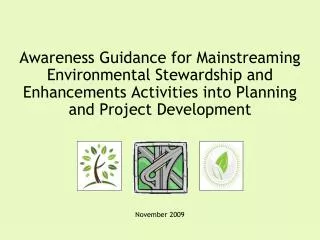

Major US Bank CDS Source: Bloomberg

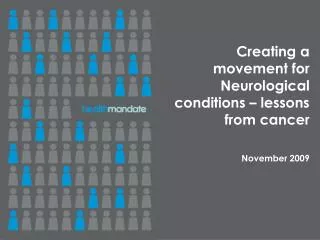

Global Bond Market Status • The corporate bond market has seen a strong rebound this year, with both investment-grade and speculative-grade spreads falling to their lowest levels since July 2008. • Corporate bond spreads have declined substantially from their peaks. • Corporate bond issuance has been robust in 2009. • Most of the fixed-rate bonds that speculative-grade companies have issued in 2009 are four to eight years in length and have a yield to maturity at issue in the 10%-14% range. • Not surprisingly, the average yield tends to be inversely correlated with ratings, meaning that lower-rated issues tend to have higher yields. • Looking forward, refinancing risk will remain an issue, with speculative grade in particular witnessing a ramp-up in the maturity schedule over the next few years. • The recent uptick in bond issues to refinance loans is partly the result of two underlying trends: • First, the high-yield bond market has been more welcoming to new issuers than the leveraged loan market. In the first nine months of the year, 86% of speculative-grade debt has been in bonds versus 45% during the same period in 2008, according to Standard & Poor's Leveraged Commentary & Data. • Second, some issuers likely have chosen to issue bonds not because they couldn't place loans, but rather because they want less restrictive covenants and, in some cases, longer maturities.

Corporate Bond Issuance Amount (Data as of Sept. 28 2009) Source: Thomson Reuters and Standard & Poor’s Global Fixed Income Research

Global Bond Market Status • The corporate bond market has seen a strong rebound this year, with both investment-grade and speculative-grade spreads falling to their lowest levels since July 2008. • Corporate bond spreads have declined substantially from their peaks. • Corporate bond issuance has been robust in 2009. • Most of the fixed-rate bonds that speculative-grade companies have issued in 2009 are four to eight years in length and have a yield to maturity at issue in the 10%-14% range. • Not surprisingly, the average yield tends to be inversely correlated with ratings, meaning that lower-rated issues tend to have higher yields. • Looking forward, refinancing risk will remain an issue, with speculative grade in particular witnessing a ramp-up in the maturity schedule over the next few years. • The recent uptick in bond issues to refinance loans is partly the result of two underlying trends: • First, the high-yield bond market has been more welcoming to new issuers than the leveraged loan market. In the first nine months of the year, 86% of speculative-grade debt has been in bonds versus 45% during the same period in 2008, according to Standard & Poor's Leveraged Commentary & Data. • Second, some issuers likely have chosen to issue bonds not because they couldn't place loans, but rather because they want less restrictive covenants and, in some cases, longer maturities.

Global Bond Market Status • The corporate bond market has seen a strong rebound this year, with both investment-grade and speculative-grade spreads falling to their lowest levels since July 2008. • Corporate bond spreads have declined substantially from their peaks. • Corporate bond issuance has been robust in 2009. • Most of the fixed-rate bonds that speculative-grade companies have issued in 2009 are four to eight years in length and have a yield to maturity at issue in the 10%-14% range. • Not surprisingly, the average yield tends to be inversely correlated with ratings, meaning that lower-rated issues tend to have higher yields. • Looking forward, refinancing risk will remain an issue, with speculative grade in particular witnessing a ramp-up in the maturity schedule over the next few years. • The recent uptick in bond issues to refinance loans is partly the result of two underlying trends: • First, the high-yield bond market has been more welcoming to new issuers than the leveraged loan market. In the first nine months of the year, 86% of speculative-grade debt has been in bonds versus 45% during the same period in 2008, according to Standard & Poor's Leveraged Commentary & Data. • Second, some issuers likely have chosen to issue bonds not because they couldn't place loans, but rather because they want less restrictive covenants and, in some cases, longer maturities.

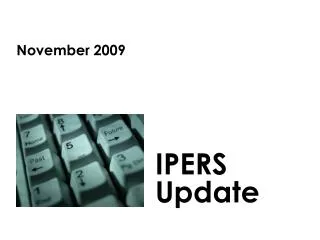

New Nonfinancial Corporate Bond Issuance (Maturities >= 3 years)

Global Bond Market Status • The corporate bond market has seen a strong rebound this year, with both investment-grade and speculative-grade spreads falling to their lowest levels since July 2008. • Corporate bond spreads have declined substantially from their peaks. • Corporate bond issuance has been robust in 2009. • Most of the fixed-rate bonds that speculative-grade companies have issued in 2009 are four to eight years in length and have a yield to maturity at issue in the 10%-14% range. • Not surprisingly, the average yield tends to be inversely correlated with ratings, meaning that lower-rated issues tend to have higher yields. • Looking forward, refinancing risk will remain an issue, with speculative grade in particular witnessing a ramp-up in the maturity schedule over the next few years. • The recent uptick in bond issues to refinance loans is partly the result of two underlying trends: • First, the high-yield bond market has been more welcoming to new issuers than the leveraged loan market. In the first nine months of the year, 86% of speculative-grade debt has been in bonds versus 45% during the same period in 2008, according to Standard & Poor's Leveraged Commentary & Data. • Second, some issuers likely have chosen to issue bonds not because they couldn't place loans, but rather because they want less restrictive covenants and, in some cases, longer maturities.

Global Bond Market Status • The corporate bond market has seen a strong rebound this year, with both investment-grade and speculative-grade spreads falling to their lowest levels since July 2008. • Corporate bond spreads have declined substantially from their peaks. • Corporate bond issuance has been robust in 2009. • Most of the fixed-rate bonds that speculative-grade companies have issued in 2009 are four to eight years in length and have a yield to maturity at issue in the 10%-14% range. • Not surprisingly, the average yield tends to be inversely correlated with ratings, meaning that lower-rated issues tend to have higher yields. • Looking forward, refinancing risk will remain an issue, with speculative grade in particular witnessing a ramp-up in the maturity schedule over the next few years. • The recent uptick in bond issues to refinance loans is partly the result of two underlying trends: • First, the high-yield bond market has been more welcoming to new issuers than the leveraged loan market. In the first nine months of the year, 86% of speculative-grade debt has been in bonds versus 45% during the same period in 2008, according to Standard & Poor's Leveraged Commentary & Data. • Second, some issuers likely have chosen to issue bonds not because they couldn't place loans, but rather because they want less restrictive covenants and, in some cases, longer maturities.

Taiwan Bond Market • Taiwan's straight bond (corporate and financial debenture issues) and convertible / exchangeable bond markets could see a resurgence in activity over the next two quarters. • a prevailing low interest rate environment and trends of raising up the interest rate, • modest signs of economic recovery in Taiwan, • the recent rebound of the domestic stock market, and • local banks' increased need to strengthen their regulatory capital ratios. • Though higher ( twAA-) rating hurdle for domestic bond issuance still exists, some issuers could sell domestic bond which is lower than "twAA-" recently, e.g. Asia Cement Corp. (tw A+)(1.95% + 5 billion NTD + 5 years on Sept. 22 2009) issued bonds in domestic market. • Credit spreads (five-year bond yields over government bonds yields with the same tenor) slightly narrowed in the second quarter of 2009, as overall issuance rates gradually adapted to a succession of interest rate cuts and a decline in investor fears. • A growing tendency for investors to factor credit risk awareness into their required yield was observed. Market participants continue to favor more creditworthy institutions, with 'twBBB' rated debentures and bonds traded at increasing spreads than higher-rated issues--'twA', 'twAA', and 'twAAA' • Structured products like securitization could be recovered back to market after the financial crisis.

Taiwan Bond Market Outstanding & Issuance Amount Source: 公司債:中央銀行網站 金融債券: 中央銀行網站 可轉債: 證券櫃檯買賣中心 證券化證券:銀行局網站

Taiwan New Issuance Amount Rated by TRC (up to Oct 2009) • Total outstanding amount of issuance bonds rated by TRC: • 1,370 billion NTD + 300 (高鐵) million USD • Amount applied to TRC and issued in 2009: • applied amount (2009 only): 199.8 billion NTD • issued in 2009 (applied in 2009 and 2008): 159.2 billion NTD • Corporate Bond : 63.5 billion NTD • Bank Debentures : 95.7 billion NTD • issued in 2009(applied in 2009 only): 117.1 billion NTD • The rest of applied amount to be issued in 2009: 82.7 billion NTD

Taiwan Bond Market • Taiwan's straight bond (corporate and financial debenture issues) and convertible / exchangeable bond markets could see a resurgence in activity over the next two quarters. • a prevailing low interest rate environment and trends of raising up the interest rate, • modest signs of economic recovery in Taiwan, • the recent rebound of the domestic stock market, and • local banks' increased need to strengthen their regulatory capital ratios. • Though higher ( twAA-) rating hurdle for domestic bond issuance still exists, some issuers could sell domestic bond which is lower than "twAA-" recently, e.g. Asia Cement Corp. (tw A+)(1.95% + 5 billion NTD + 5 years on Sept. 22 2009) issued bonds in domestic market. • Credit spreads (five-year bond yields over government bonds yields with the same tenor) slightly narrowed in the second quarter of 2009, as overall issuance rates gradually adapted to a succession of interest rate cuts and a decline in investor fears. • A growing tendency for investors to factor credit risk awareness into their required yield was observed. Market participants continue to favor more creditworthy institutions, with 'twBBB' rated debentures and bonds traded at increasing spreads than higher-rated issues--'twA', 'twAA', and 'twAAA' • Structured products like securitization could be recovered back to market after the financial crisis.

Taiwan Bond Market • Taiwan's straight bond (corporate and financial debenture issues) and convertible / exchangeable bond markets could see a resurgence in activity over the next two quarters. • a prevailing low interest rate environment and trends of raising up the interest rate, • modest signs of economic recovery in Taiwan, • the recent rebound of the domestic stock market, and • local banks' increased need to strengthen their regulatory capital ratios. • Though higher ( twAA-) rating hurdle for domestic bond issuance still exists, some issuers could sell domestic bond which is lower than "twAA-" recently, e.g. Asia Cement Corp. (tw A+)(1.95% + 5 billion NTD + 5 years on Sept. 22 2009) issued bonds in domestic market. • Credit spreads (five-year bond yields over government bonds yields with the same tenor) slightly narrowed in the second quarter of 2009, as overall issuance rates gradually adapted to a succession of interest rate cuts and a decline in investor fears. • A growing tendency for investors to factor credit risk awareness into their required yield was observed. Market participants continue to favor more creditworthy institutions, with 'twBBB' rated debentures and bonds traded at increasing spreads than higher-rated issues--'twA', 'twAA', and 'twAAA‘. • Structured products like securitization could be recovered back to market after the financial crisis.

Taiwan Bond Market • Taiwan's straight bond (corporate and financial debenture issues) and convertible / exchangeable bond markets could see a resurgence in activity over the next two quarters. • a prevailing low interest rate environment and trends of raising up the interest rate, • modest signs of economic recovery in Taiwan, • the recent rebound of the domestic stock market, and • local banks' increased need to strengthen their regulatory capital ratios. • Though higher ( twAA-) rating hurdle for domestic bond issuance still exists, some issuers could sell domestic bond which is lower than "twAA-" recently, e.g. Asia Cement Corp. (tw A+)(1.95% + 5 billion NTD + 5 years on Sept. 22 2009) issued bonds in domestic market. • Credit spreads (five-year bond yields over government bonds yields with the same tenor) slightly narrowed in the second quarter of 2009, as overall issuance rates gradually adapted to a succession of interest rate cuts and a decline in investor fears. • A growing tendency for investors to factor credit risk awareness into their required yield was observed. Market participants continue to favor more creditworthy institutions, with 'twBBB' rated debentures and bonds traded at increasing spreads than higher-rated issues--'twA', 'twAA', and 'twAAA‘. • Structured products like securitization could be recovered back to market after the financial crisis.