Download

1 / 33

330 likes | 445 Views

Chapter 6: Processing: Pre-Qualification & Loan Application. Part III PROCESSING. By Dr. D. Grogan M.C. “Buzz” Chambers. PREVIEW.

E N D

Chapter 6: Processing: Pre-Qualification & Loan Application Part III PROCESSING By Dr. D. Grogan M.C. “Buzz” Chambers

PREVIEW The purpose of this chapter is to show the learner how the mortgage loan broker bridges the gap between the borrower’s infrequent borrowing of real estate loan funds and the lender’s frequent daily business transaction practices. The mortgage loan broker aids in the paperwork and forms required to close a real estate loan. The purpose of this chapter is also to familiarize the learner with the Uniform Residential Loan Application (URLA, FNMA 1003). Different types of loans have differing, specific qualifications for each particular loan.

STUDENT LEARNING OUTCOME 1. Complete buyer qualification data to determine qualifying ratios. 2. Differentiate between acceptable ratios for Federal Housing Administration (FHA), Department of Veterans Administration (DVA), and conventional financing. 3. Outline basic DVA eligibility criteria for veterans. 4. Explain the sections of the URLA 1003, loan application.

Mortgage Loan Broker Role: Your title: Loan agent, loan representative Your job: A liaison between lender & borrower Your role: Accept & process the loan application Provide required disclosure Verify information Obtain additional information from borrower Reject application Provide borrower with written credit disclosure and reporting agency Reject or Accept the loan based on the information

6.1 Lender/Purchase Statement • The lender should obtain a copy of the accepted purchase agreement after the mortgage loan broker has received a completed loan application and has a credit report. • The loan broker should provide a letter showing: • Borrower loan qualification • Purchase price maximum for borrower • Creditworthiness of the borrower

Property Profile • When a purchase agreement is finalized, the loan broker needs to obtain a property profile to determine: • Current title holders • Legal description • Status on property tax payments • Liens • Trust deeds • Comparables • Assessor parcel number (APN)

6.2 Disclosure of Home Ownership Counseling Purpose: The more the borrower knows about home ownership, the better the borrow can make realistic and wise purchase & loan decisions. Required by some loan programs before purchaser approved for a specific loan. How much money will be needed to consummate the transaction, including the down payment, closing costs, and the reserves? What does the credit history indicate about the future ability to make the loan payments? What questions should the borrower ask when shopping for a loan to obtain attractive terms? Can the borrower budget for the cost of home ownership to obtain the tax advantages of home ownership?

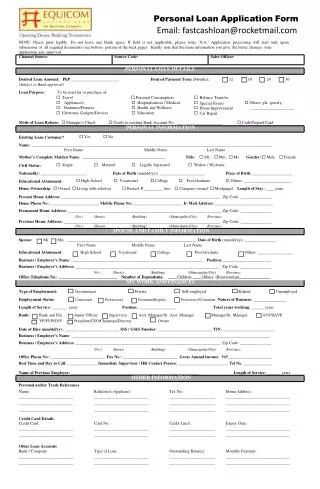

6.3 Residential Loan Application • FNMA form 1003 • Pronounced: 10 – 0 – 3 • New version Jan 2010 • Appendix A shows the English/Spanish form • An explanation for each circled number corresponds with the form and directions. • The circled numbers on the form require detailed and accurate information for each item.

Uniform Residential Loan Application1003 – Page 1 Part 1 – Type of loan applied for. Loan terms Part 2 – Property information. Loan purpose: purchase, refinance, construction) Part 3 – Borrower info (socialsecurity number) Part 4 – Employment info (number of years) Note: Want to see at least 2 years employment history & 2 years residential history.

Uniform Residential Loan Application1003 – Page 2 Part 5: Monthly Income & Expense data Income, commissions, dividends, rental income Monthly housing expense for Loans, taxes, insurance, association dues Part 6: Assets and liabilities data Liquid assets (cash, checking accounts) Other assets (real estate, retirement, vehicles) Liabilities includes unpaid loan balances Total assets - Total liabilities = Net Worth

Uniform Residential Loan Application1003 – Page 3 Part 6 (continued): Real Estate owned Rental income and creditor name Part 7: Transaction details Purchase price + costs + discount points List of subordinate financing and credits Mortgage insurance and funding fee financed Add loan amount + insurance + funding fee Subtract cash from borrower

Uniform Residential Loan Application1003 – Page 3 Part 8: Borrower & Co-borrower Declarations Any judgments, bankruptcy, foreclosure or lawsuit Any SBA or student loans or government agency Any alimony, child support or maintenance pay No part of down payment is borrower If borrower is a co-maker or endorser on a note Resident status (citizen or permanent resident alien) Ownership interest in property in past few years

Uniform Residential Loan Application1003 – Page 3 Part 9: Acknowledgements and Agreements Acknowledge purpose of the loan & intent The loan is senior No illegal uses Agreement to amend items during loan period Transfer or assignment No representations nor warranties by lender Certification Information provided is true and correct Civil liability & criminal prosecution for misrepresentation Signed and dated by each borrower

Uniform Residential Loan Application1003 – Page 3 Part 10: Government monitoring Borrower states they will not furnish data, or Borrower completes the requested information: Race National origin Sex Interviewer required to complete data How application taken Interviewer information • Part 10: Government monitoring • Borrower gives any additional useful information • All parties sign and date this page

SECTION 2: Pre-Qualifications Income: Establish income Verify pay stub, tax returns, W-2’s. Document bonuses, rental & interestincome

6.4 Qualifying Ratios: Front End Ratio = Total Housing expense/Gross Income Conventional – 95% LTV Max. Ratio is 26% Conventional – 90% LTV Max. Ratio is 28% Conventional – 80% LTV Max. Ratio is 32%FHA – Max Ratio is 29% Back End Ratio = Proposed Housing exp + All debt / Gross Income Conventional loans – maximum 33% 36% 38% FHA and DVA maximum ratio is 41% Community Home Buyers Program may be as high as 45%

Ratio Calculation BACK END RATIO = PITI + HOA + MI + DEBTS GROSS INCOME (GI) MONTHLY PITI + HOA + MI FRONT END RATIO = GROSS INCOME (GI) MONTHLY

ARM Income-Expense Ratios Housing Total monthly Expense Debt service FNMA (LTV 90% or more) 26% 33% FNMA (LTV 90% or less) 28% 36% FHLMC (exceeds cap and 25% 33% discount guidelines)

6.5 Dept of Veterans Administration (DVA) Qualification • DD form 214, Report of Release or Discharge From Active Duty • Original Certificate of Eligibility • Eligibility requirements for various conflict periods • Beginning and ending dates of the conflict • Specific number of active days of service • Minimum 24 full months for post-Vietnam

Service Period Criteria E RA DATES LENGTH OF SERVICE World War II 09/16/40-07/25/47 90 days active duty Peacetime 07/26/47-06/26/50 181 days continuous active duty Korean Conflict 06/27/50-01/31/55 90 days active duty Post-Korean 02/01/55-08/04/64 181 days continuous active duty Vietnam 08/05/64-05/07/75 90 days active duty

Service Period Criteria (cont) Post-Vietnam 05/08/75-09/07/80 181 days continuous active duty Enlisted 09/08/80-08/01/90 2 years (24 months) active duty Officers 10/17/81-08/01/90 2 years (24 months) active duty Persian Gulf 08/02/90-undetermined 24 months or period called to active duty, not less than 90 days Veteran is still on 181 days of Continuous Service active duty

Maximum DVA loans: Calculating the sales price/loan amount gross income Gross Income Multiply by X 41% Total debt service, including housing expense Subtract monthly installment/revolving debts Total debt allowed for PITI Subtract figure for monthly taxes and insurance/Homeowners association dues (HOA) Total debt for principal and interest Divide by P & I factor for current allowable interest rate Maximum loan amount borrower may receive

Table of residual income by region For loan amounts below $79,999: Family Size Northeast Midwest South West 1 $390 $382 $382 $425 2 $654 $641 $641 $713 3 $788 $772 $772 $859 4 $888 $868 $868 $967 5 $921 $902 $902 $1,004 Over 5 Add $75 for each additional member up to a family of 7 For loan amounts above $80,000: Family Size Northeast Midwest South West 1 $450 $441 $441 $491 2 $755 $738 $738 $823 3 $909 $889 $889 $990 4 $1,025 $1,003 $1,003 $1,117 5 $1,062 $1,039 $1,039 $1,158 Over 5 Add $80 for each additional member up to a family of 7

6.6 Federal Housing Administration (FHA) Qualifications Calculate the maximum loan amount from the gross income. Proof of total verifiable income from all sources. Total monthly expenses that continue for six months or longer. Determine ratios: 31% front end; 43% back end. Calculate maximum loan amount. Estimate closing costs and down payment for total cash required to close escrow.

Maximum FHA loan amount $ _________ Gross income Multiply by × 43% Back-end ratio Total debt service including housing expense Subtract monthly installment/revolving debts Total income allowed for PITI Subtract figure for monthly taxes and insurance/HOA Total income for principal and interest Divide by P & I factor for interest rate (varies with point structure—buydown) Maximum loan amount borrower may obtain ADD CASH DOWN PAYMENT Total Price Total Sales Price

MONTHLY GROSS INCOME Borrower’s Base Income $ Other $_____________ Co-borrower’s Income $ Other $_____________ TOTAL MONTHLY INCOME (Gross) $_____________(A)

DEBTS AND OBLIGATIONS Installment Debt $ ______ (10 mo. or longer-Car, Student Loans, Etc.) Revolving Debt (Credit Cards) $______ TOTAL MONTHLY OBLIGATIONS $ _________(B)

MONTHLY PAYMENTS Prin. and Int. $___________ Loan Amount $_________ + MIP_________ = $ __________ Homeowners Assoc. (Monthly Dues) $ __________ Not Covered______________ (i.e., fire, flood, etc.) Hazard Insurance (Fire Only) $ __________ Property Taxes @ __________% of the purchase price $ ________ TOTAL HOUSING EXPENSES $ ________________ (C)

FHA Qualifying worksheet TOTAL HOUSING EXPENSE (C) $______ ÷ Total Gross Income (A) $______ = ______% TOTAL FIXED PAYMENTS (B) + (C) $______ ÷ Total Gross Income (A) $______ = ______% Ratio Guidelines are 31%/43%. These ratios may be exceeded by up to 2% if the property is "Energy Efficient" (built after 1976). Cash-Out Refinance: No compensating factors allowed, ratios as stated, 31%/43%, CANNOT BE EXCEEDED.

6.7 Conventional Qualifications • Reserve requirements: • $417,000 > 2-3 months PITI held as cash • $417-$729,750 6 months reserves • > $1 million 12 months reserves • Obtain borrower’s total gross income from all sources. • Determine housing expense (A PITI). • Obtain borrower’s assets & liabilities. • Calculate ratios: front end & back end.

Calculating the Sales Price/Loan from Gross Income Gross Income Multiply by × 36% (33, 36, 38% back-end ratios based on the LTV) Total debt service including housing expense Subtract monthly installment/revolving debts Total allowed for PITI Subtract figure for monthly taxes and insurance/HOA Total allowed for PI Divide by P & I factor for interest rate (varies with points charged) Maximum loan amount borrower may obtain Divide by loan to value percentage (0.95, 0.90, 0.80) Sales price borrower may purchase

6.8 Other Qualifications • When a borrower or property falls into the following categories, additional qualifications are often required: • the structure does not conform to the zoning of the land (for example, a single family residence is located on land that is zoned C-1, commercial, I-1, or industrial). • the borrower’s mortgage payment record is slow and there have been three to four late payments in the last twelve months. • the property is been placed into foreclosure. • the borrower’s length of time on the job does not meet FNMA/FHLMC guidelines.

Match Borrower to Loan Program I. LOAN-TO-VALUE RATIO (LTV) DVA – up to 100% FHA – down payment of 3% Conventional – up to 95% (103%) as of 2/1/02 some lenders Commercial loans – usually only up to 60% Community Home Buyer – up to 97% II. Each loan program has unique features III. Each mortgage loan broker may represent numerous lenders with various program & loans