Download

1 / 24

250 likes | 369 Views

You and Your Credit Score. FICO. The Score.

E N D

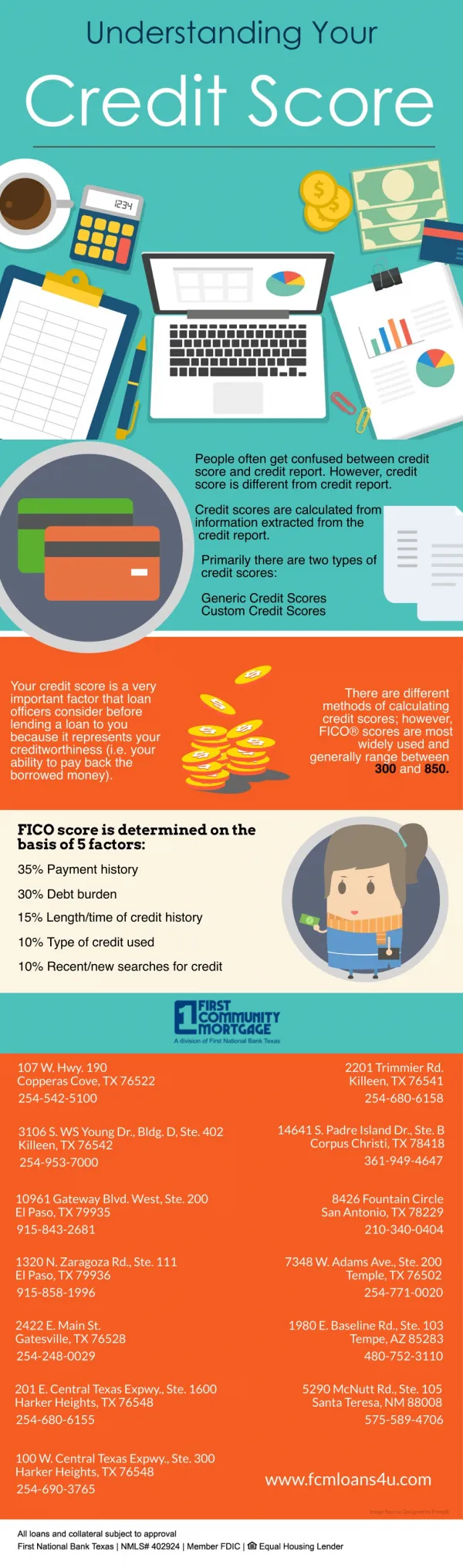

The Score • The most widely used credit score is the FICO Score, the credit score created by Fair Isaac Corporation. Lenders use the FICO Score to help them make billions of credit decisions every year. Fair Isaac calculates the FICO Score based solely on information in consumer credit reports maintained at the credit reporting agencies.

Score Range • FICO credit scores range from 300 to 850. That FICO Score is calculated by a mathematical equation that evaluates many types of information from your credit report, at that agency. By comparing this information to the patterns in hundreds of thousands of past credit reports, the FICO Score estimates your level of future credit risk.

What does Your Credit Report Contain • Identification -Name, address -Social Security Number -Current and Previous employers • Credit Information -Credit accounts with Financial institutions, retailers, credit card issuers, other lenders -Credit limits, account balance, payment pattern over the last two years

What does Your Credit Report Contain • Public record information -Bankruptcies -Judgements -Tax liens • Inquiries -Credit Grantors -Potential employers • Credit Score (if requested)

What is not in your Report • Race or religion • National origin • Sex and marital status • Whether you receive public assistance • Criminal activity

What is your credit score? • A credit score is a number which represents an estimate of an individual’s financial creditworthiness • A pioneer credit score company, FICO was founded in 1956 as Fair, Isaac and Company by engineer Bill Fair and mathematician Earl Isaac.

Five Parts to your FICO credit scores • 35% of Score - Payment history • The score is affected by how many bills have been paid late, how many were sent out for collection and any bankruptcies. When these things happened also comes into play. The more recent, the worse it will be for your overall score. • 30% of Score – How much you owe How much do you owe on car or home loans? How many credit cards do you have that are at their credit limits? The rule of thumb is to keep your card balances at 25 percent or less of their limits.

FICO Score • 15% of Score – Length of Credit History • The longer you've had established credit, the better it is for your overall credit score. • 10% of Score – New Credit Opening new credit accounts will negatively affect your score for a short time. This category also penalizes hard inquiries on your credit in the past year.

FICO Score • 10% of Score –is based on the types of credit you currently have. It will help your score to show that you have had experience with several different kinds of credit accounts, such as revolving credit accounts and installment loans.

FICO Score • FICO credit scores have a 300–850 score range. The higher the score, the lower the risk. But no score says whether a specific individual will be a “good” or “bad” customer.

Not the only thing… • While many lenders use FICO credit scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable for a given credit product. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders use to determine your actual interest rates.

The minimum required to calculate a FICO Score • For your FICO Score to be calculated, your score must contain enough information—and enough recent information—on which to base your credit score. Generally, that means you must have at least one account that has been open for six months or longer, and at least one account that has been reported to the credit reporting agency within the last six months.

How Actions Affect Credit Scores:Examples • Charge 2 credit cards to the credit limit • Score drops from 780 to 700 • Pay off a credit account • Score increases from 600 to 680 • Pay late on a bank loan payment • Score drops from 720 to 645 • Pay all credit accounts on time • Score increases from 707 to 727

Why Credit Scores are important • Helps lenders predict how likely you are to make credit payments on time • Affect whether you can get credit • What you pay for credit cards, auto loans, mortgages, and other types of credit • Higher scores more likely to be approved and pay a lower interest rate

About Credit Scores - • Many types of credit scores • Lenders usually mean FICO score developed by Fair Isaac Corporation • Most commonly used scoring system • Scores range from 300 – 850 • Most people score in the 600s and 700s

Myths about Credit Scores • Close unused credit cards – False • Your credit report merges when you marry – False • FICO Scores are based on income – False • Checking your score hurts your score - False

Why Scores go Down: • Pay late or pay less than required payment • Public Record items appear • Bankruptcy, Judgements • Credit balances go up a lot • Open new accounts

What makes scores go up: • Pay bills on time • Pay down credit card balances • Keep older accounts open • Avoid opening new ones • Apply for new credit only when you need it • Make sure your credit report is accurate

Improving your Score will… • Lower your interest rates • Speed up credit approvals • Get better credit card, auto, mortgage offers

Key Points: • Get a copy of your credit report annually • Every 12 months – free copy of credit report from three major reporting agencies www.annualcreditreport.com or 1-877-322-8228 • Correct any errors or inaccuracies • Establish good credit habits

3 Major Credit Reporting Agencies • Experian • Web: www.experian.com • Phone: 1-800-200-6020 • Equifax • Web: www.equifax.com • Phone: 1-866-685-1111 • Transunion • Web: www.transunion.com • Phone 1-800-888-4213