Download

1 / 12

130 likes | 616 Views

Pro Forma Analysis. Used for valuing firms granting credit acquiring companies planning strategy budgeting More art than science. Sales Forecast. Typically, start with sales forecast fundamental factor determining firm’s future drives other variables in firm

E N D

Pro Forma Analysis • Used for • valuing firms • granting credit • acquiring companies • planning strategy • budgeting • More art than science

Sales Forecast • Typically, start with sales forecast • fundamental factor determining firm’s future • drives other variables in firm • Generally start with historic growth rates • Break down by industry/geographic segment • Adjust for know economic changes (e.g., Asia) • Asymptote to steady-state economy growth • E.g., Coke sales will grow 5% in 2003, and then grow 4.5% through 2004 and 4% thereafter

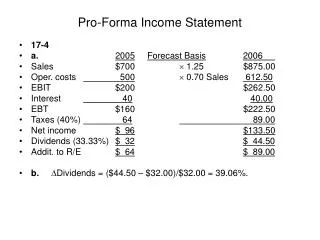

Income Statement Forecasts • Cost of goods sold and S,G&A • typically percentage of sales • based on adjusted historic % • Coke CGS will be 30% going forward • Coke SGA will be 40% going forward • Interest is based on expected debt • assumed constant $199 for Coke case • Income tax expense is based on tax rates applied to pretax income • Coke’s will be 27% going forward

Working Capital • Accounts Receivable tie to sales and terms • use accounts receivable turnover (or percent of sales) • Inventories tie to cost of goods sold • use inventory turnover (or percent of sales) • Accounts payable tie to purchases and terms (or percent of sales) • Other working capital typically ties to sales • For convenience, we will assume • Cash remains at constant percentage of sales • Noncash WC of $750 in 2002, $850 in 2003 and growth with sales thereafter

PP&E • capital expenditures tie lead sales growth • $950 in 2002, $1,100 in ‘03, with sales growth thereafter • depreciation is based on capital expenditures • 80% of capital expenditures • Stock issuance/repurchase and long-term debt tie to capital needs • Coke repurchases with excess cash

Dividends are a percent of earnings • 45% going forward • Retained earnings ties to dividends and net income • We will assume all excess cash is used to repurchase shares

Statement of cash flows follows from: • income statement • balance sheet • Warning!!! Check frequently to ensure your numbers make sense